Question: BIUX, X APA E Emphasis Heading Normal Subtitle Title No Space Replace Select Create and Share Adobe PDF fon Adobe Acro LLLLLLLLLLLLL LLLLLLLLL il Yerel

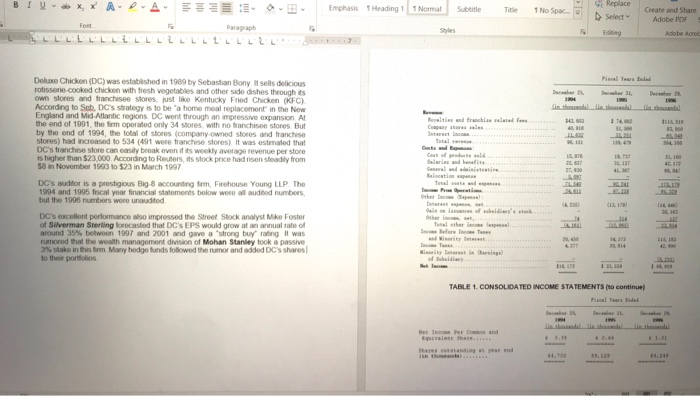

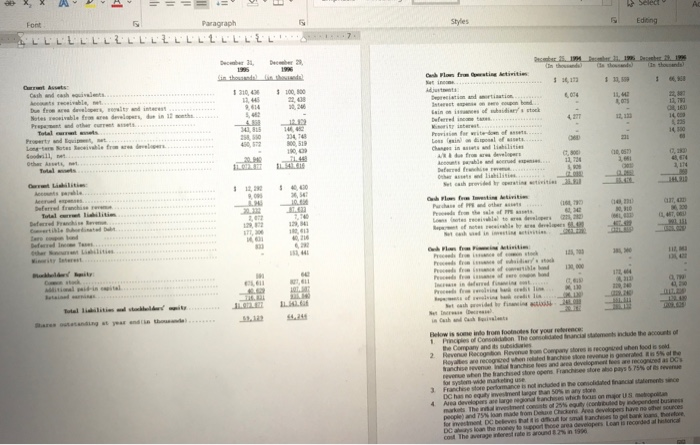

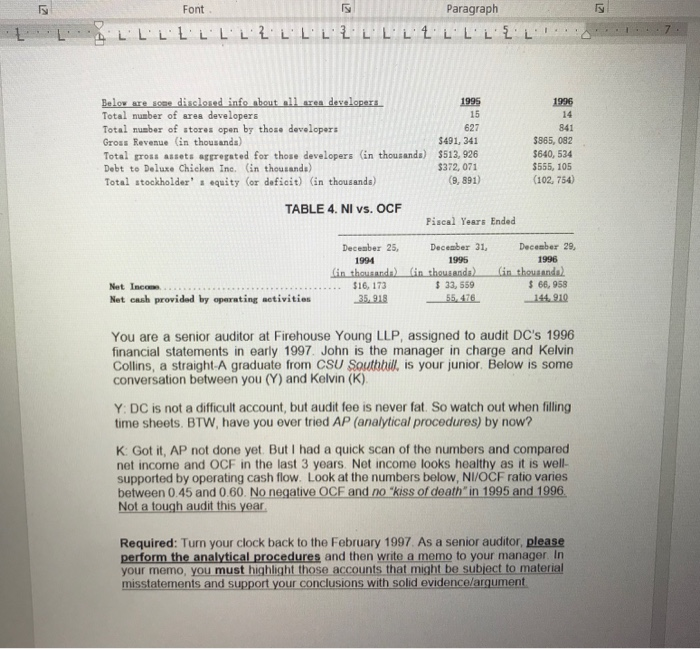

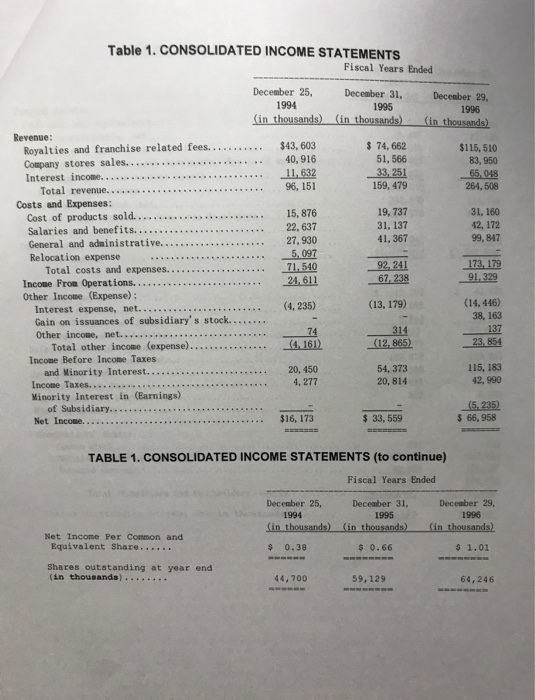

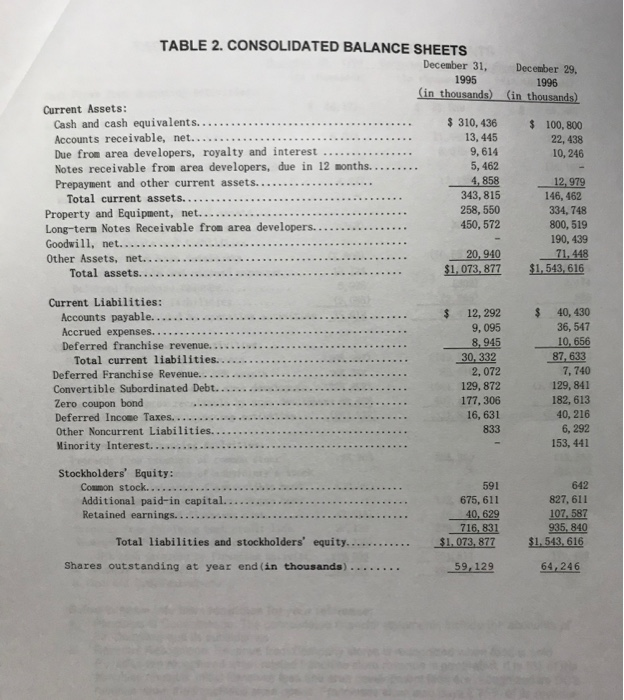

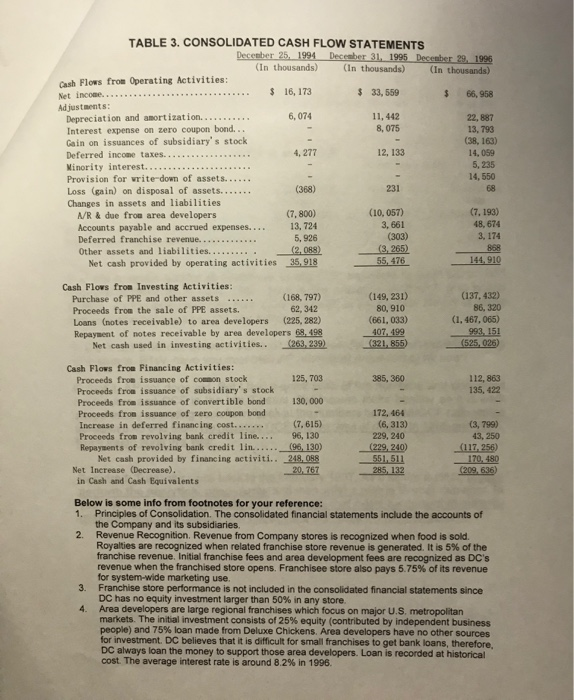

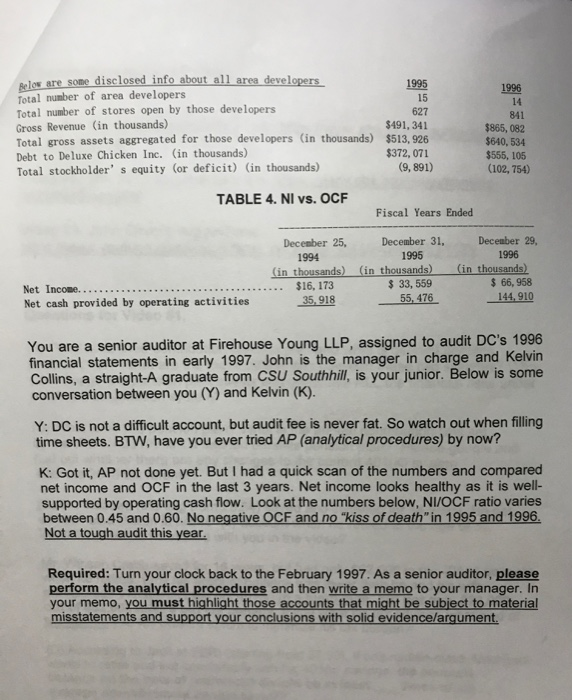

BIUX, X APA E Emphasis Heading Normal Subtitle Title No Space Replace Select Create and Share Adobe PDF fon Adobe Acro LLLLLLLLLLLLL LLLLLLLLL il Yerel December December Deluxe Chicken (DC) was established in 1989 by Sebastian Bony sells delicious rotisserie cooked chicken with fresh vegetables and other side dishes through its own stores and franchise stores just like Kentucky Fried Chicken (KFC) According to Sob DC's strategy is to be a home meal replacement in the New England and Mid Atlantic regions DC went through an motive expansion At the end of 1901, the firm operated only 34 stores with no wranchisee stores But by the end of 1994, the total of stores company owned to and franchise stores) had increased to 534 (491 were franchise stores) it was estimated that DC's franchise store can easily beak events weekly average revenue perstore is higher than $23000. According to Reuters its stock pricehad nison steadily from $8 in November 1993 to $23 in March 1997 DC's auditor is a prestigious Big B accounting , Fehouse Young LLP. The 1994 and 1995 Incal year financial statements below wore audited numbers but the 1906 numbers were unaudited DC's excellent performance who impressed the Street Stock analyst Mke Foster of Silverman Sterling located that DC's EPs would grow an annual rate of around 35% between 1907 and 2001 and gave a strong buy rating It was rumored that the wealth Management division of Mohan Stanley took a passive 3% stake in this form Mary hedge funds followed the rumor and added DC's shares to the portfolios TABLE 1. CONSOLIDATED INCOME STATEMENTS (to continue wat Terende Net Income Per Command are a year and XXV Select Styles Editing Paragraph LLLLLLLLLLLLL LLLLLLLLL Dec 1 1 1.1 De 196 December 31 as ritra atima timitis 1 300 100,00 s Teble, et Due fredere, ritend interes Notes receivable for deve d e in 30,346 ains of widerstock 122132 SO Los in a disposal of t... 1,800 (10,0529 11.463 09 356 (10,10 Deferred franchise Purchase and other COM 2010 1,457,00 Dans leven 123 1003 B lade 401 LITE Pereira 11, Wil pall-incl. LE DO - E dit ut cathodet befinn Below is somente tror footnotes for your reference 1 Principles of Conson The conceded bruncia m e include the account of Company and its subsidies 2 Revenue Recobon evento company stores is recoged when food is sold Heyes we recogned when r ed anche wore is the Banche venge anchisees and we developments are record as even when the franchised store opens Franchisesore pays 575 of severe 3 Franchise to performance is not included in the com ediana mente DC has no galvestment agera 50 any store 4 Ave developers a large egna bandeses e boas on S p ot ma Thement confectby panduan for women DC beves that is a formal and to get back and therefore DC on the money to proceea developers canis recorded at local co The average were is around in 1990 Font Paragraph A LLLLLLLL LLLLL LLLLLLL 1996 14 841 Below are some disclosed info about all area developer Total number of area developers Total number of stores open by those developers Gross Revenue (in thousands) Total gross assets arregated for those developers (in thousands) Debt to Deluxe Chicken Inc. (in thousands) Total stockholder's equity (or deficit) (in thousands) 1995 15 627 $491, 341 $513, 926 $372, 071 (9,891) $865, 082 $640, 534 $555, 105 (102, 754) TABLE 4. NI vs. OCF Piscal Years Ended December 25, 1994 Gin thousanda) $16,173 35,918 December 31, 1995 Gin thousanda) $ 33,559 55.476 December 29, 1996 Gin thousands $ 66,958 144.910 Net Inc . Net cash provided by operating activities You are a senior auditor at Firehouse Young LLP, assigned to audit DC's 1996 financial statements in early 1997 John is the manager in charge and Kelvin Collins, a straight. A graduate from CSU Southhill, is your junior Below is some conversation between you (Y) and Kelvin (K). Y DC is not a difficult account, but audit fee is never fat. So watch out when filling time sheets. BTW, have you ever tried AP (analytical procedures) by now? K Got it, AP not done yet. But I had a quick scan of the numbers and compared net income and OCF in the last 3 years. Net income looks healthy as it is well- supported by operating cash flow. Look at the numbers below, NI/OCF ratio varies between 0.45 and 0.60. No negative OCF and no "kiss of death" in 1995 and 1996. Not a tough audit this year Required: Turn your clock back to the February 1997 As a senior auditor, please perform the analytical procedures and then write a memo to your manager in your memo, you must highlight those accounts that might be subject to material misstatements and support your conclusions with solid evidence/argument Deluxe Chicken (DC) was established in 1989 by Sebastian Bony. It sells delicious rotisserie-cooked chicken with fresh vegetables and other side dishes through its own stores and franchisee stores, just like Kentucky Fried Chicken (KFC). According to Seb, DC's strategy is to be "a home meal replacement" in the New England and Mid-Atlantic regions. DC went through an impressive expansion. At the end of 1991, the firm operated only 34 stores, with no franchisee stores. But by the end of 1994, the total of stores (company-owned stores and franchise stores) had increased to 534 (491 were franchise stores). It was estimated that DC's franchise store can easily break even if its weekly average revenue per store is higher than $23,000. According to Reuters, its stock price had risen steadily from $8 in November 1993 to $23 in March 1997. DC's auditor is a prestigious Big-8 accounting firm, Firehouse Young LLP. The 1994 and 1995 fiscal year financial statements below were all audited numbers, but the 1996 numbers were unaudited. DC's excellent performance also impressed the Street. Stock analyst Mike Foster of Silverman Sterling forecasted that DC's EPS would grow at an annual rate of around 35% between 1997 and 2001 and gave a strong buy" rating. It was rumored that the wealth management division of Mohan Stanley took a passive 3% stake in this firm. Many hedge funds followed the rumor and added DC's shares to their portfolios. Table 1. CONSOLIDATED INCOME STATEMENTS Fiscal Years Ended December 25, 1994 (in thousands) December 31, 1995 (in thousands) December 29, 1996 (in thousands) $43, 603 40,916 $ 74,662 51,566 33, 251 159, 479 11, 632 96, 151 $115,510 83,950 65,048 264, 508 19, 737 31, 137 41,367 31. 160 42, 172 99,847 Revenue: Royalties and franchise related fees........ Company stores sales............. Interest income............. Total revenue.... Costs and Expenses: Cost of products sold.......... Salaries and benefits.... General and administrative..... Relocation expense Total costs and expenses.... Income From Operations... Other Income (Expense): Interest expense, net...... Gain on issuances of subsidiary's stock. Other income, net.... Total other income (expense). Income Before Income Taxes and Minority Interest....... Incope Taxes......... Minority Interest in (Earnings) of Subsidiary......... Net Income........... 15, 876 22, 637 27,930 5.097 71,540 24,611 92,241 67.238 173, 179 91. 329 (4,235) (13, 179) (14.446) 38, 163 137 23,854 74 314 (4.161) (12,865) 20, 450 4,277 54,373 20,814 115, 183 42, 990 $16, 173 (5.235) $ 66,958 $ 33,559 TABLE 1. CONSOLIDATED INCOME STATEMENTS (to continue) Fiscal Years Ended December 25, 1994 (in thousands) December 31. 1995 (in thousands) December 29, 1996 (in thousands) Net Income Per Common and Equivalent Share... $ 0.38 $ 0.66 $ 1.01 Shares outstanding at year end (in thousands) .... 44,700 59,129 64.246 December 29, 1996 (in thousands) $ TABLE 2. CONSOLIDATED BALANCE SHEETS December 31, 1995 (in thousands) Current Assets: Cash and cash equivalents........... $ 310, 436 Accounts receivable, net............ 13,445 Due from area developers, royalty and interest. 9,614 Notes receivable from area developers, due in 12 months.. 5, 462 Prepayment and other current assets..... 4,858 Total current assets..... 343, 815 Property and Equipment, net...... 258, 550 Long-term Notes Receivable from area developers..... 450, 572 Goodwill, net......... Other Assets, net............. 20,940 Total assets................. $1,073, 877 100,800 22, 438 10,246 12,979 146, 462 334, 748 800, 519 190, 439 71, 448 $1,543, 616 $ $ Current Liabilities: Accounts payable............ Accrued expenses............ Deferred franchise revenue....... Total current liabilities...... Deferred Franchise Revenue........... Convertible Subordinated Debt......... Zero coupon bond Deferred Income Taxes...... Other Noncurrent Liabilities..... Minority Interest....... 12, 292 9,095 8.945 30. 332 2,072 129,872 177, 306 16, 631 833 40, 430 36,547 10,656 87.633 7, 740 129, 841 182, 613 40,216 6,292 153, 441 Stockholders' Equity: Common stock........... Additional paid-in capital........ Retained earnings... 591 675, 611 40,629 716, 831 $1.073, 877 642 827, 611 107,587 935, 840 $1.543, 616 Total liabilities and stockholders' equity............ Shares outstanding at year end (in thousands) ........ 59,129 64,246 TABLE 3. CONSOLIDATED CASH FLOW STATEMENTS December 25. 1994 December 31, 1995 December 29, 1996 (In thousands) (In thousands) (In thousands) Cash Flows from Operating Activities: Net income.. ... $ 16, 173 $ 33,559 66,958 Adjustments Depreciation and amortization........... 6,074 11,442 22,887 Interest expense on zero coupon bond. .. 8, 075 13,793 Gain on issuances of subsidiary's stock (38, 163) Deferred income taxes...... 12, 133 14.059 Minority interest............. 5,235 Provision for write-down of assets...... 14,550 Loss (gain) on disposal of assets. (368) 231 Changes in assets and liabilities MR & due from area developers (7, 800) (10,057) (7,193) Accounts payable and accrued expenses.... 13,724 3,661 48, 674 Deferred franchise revenue.. 5.926 (303) 3. 174 Other assets and liabilities.... (2,088) (3 265) Net cash provided by operating activities 35,918 55, 476 144.910 4,277 Cash Flows from Investing Activities: Purchase of PPE and other assets ...... (168, 797) Proceeds from the sale of PPE assets. 62,342 Loans (notes receivable) to area developers (225, 282) Repayment of notes receivable by area developers 68, 498 Net cash used in investing activities.. (263, 239) (149,231) 80,910 (661, 033) 407, 499 (321, 855) (137,432) 86, 320 (1,467,065) 993, 151 (525, 026) 125, 703 385, 360 112,863 135, 422 130,000 Cash Flows from Financing Activities: Proceeds from issuance of common stock Proceeds from issuance of subsidiary's stock Proceeds from issuance of convertible bond Proceeds from issuance of zero coupon bond Increase in deferred financing cost....... Proceeds from revolving bank credit line.... Repayments of revolving bank credit lin...... Net cash provided by financing activiti.. Net Increase (Decrease). in Cash and Cash Equivalents (7.615) 172, 464 (6,313) 229, 240 (229,240) 551, 511 285, 132 (96, 130) 248. ONS 20,767 (3 799) 43, 250 (117.256) 170, 480 (209,636) Below is some info from footnotes for your reference: 1. Principles of Consolidation. The consolidated financial statements include the accounts of the Company and its subsidiaries. 2. Revenue Recognition. Revenue from Company stores is recognized when food is sold Royalties are recognized when related franchise store revenue is generated. It is 5% of the franchise revenue. Initial franchise fees and area development fees are recognized as DC's revenue when the franchised store opens. Franchisee store also pays 5.75% of its revenue for system-wide marketing use. 3. Franchise store performance is not included in the consolidated financial statements since DC has no equity investment larger than 50% in any store. Area developers are large regional franchises which focus on major U.S. metropolitan markets. The initial investment consists of 25% equity (contributed by independent business people) and 75% loan made from Deluxe Chickens Area developers have no other sources for investment. DC believes that it is difficult for small franchises to get bank loans, therefore, DC always loan the money to support those area developers. Loan is recorded at historical cost. The average interest rate is around 8.2% in 1996. 1996 Below are some disclosed info about all area developers 1995 Total number of area developers 15 Total number of stores open by those developers 627 Gross Revenue (in thousands) $491, 341 Total gross assets aggregated for those developers (in thousands) $513, 926 Debt to Deluxe Chicken Inc. (in thousands) $372,071 Total stockholder's equity (or deficit) (in thousands) (9,891) 841 $865, 082 $640, 534 $555, 105 (102, 754) TABLE 4. NI vs. OCF Fiscal Years Ended December 25, 1994 (in thousands) $16, 173 35,918 December 31, 1995 (in thousands) $ 33, 559 55, 476 December 29, 1996 (in thousands) $ 66,958 144, 910 Net Income..... Net cash provided by operating activities You are a senior auditor at Firehouse Young LLP, assigned to audit DC's 1996 financial statements in early 1997. John is the manager in charge and Kelvin Collins, a straight-A graduate from CSU Southhill, is your junior. Below is some conversation between you (Y) and Kelvin (K). Y: DC is not a difficult account, but audit fee is never fat. So watch out when filling time sheets. BTW, have you ever tried AP (analytical procedures) by now? K: Got it, AP not done yet. But I had a quick scan of the numbers and compared net income and OCF in the last 3 years. Net income looks healthy as it is well- supported by operating cash flow. Look at the numbers below, NI/OCF ratio varies between 0.45 and 0.60. No negative OCF and no "kiss of death in 1995 and 1996. Not a tough audit this year. Required: Turn your clock back to the February 1997. As a senior auditor, please perform the analytical procedures and then write a memo to your manager. In your memo, you must highlight those accounts that might be subject to material misstatements and support your conclusions with solid evidence/argument. BIUX, X APA E Emphasis Heading Normal Subtitle Title No Space Replace Select Create and Share Adobe PDF fon Adobe Acro LLLLLLLLLLLLL LLLLLLLLL il Yerel December December Deluxe Chicken (DC) was established in 1989 by Sebastian Bony sells delicious rotisserie cooked chicken with fresh vegetables and other side dishes through its own stores and franchise stores just like Kentucky Fried Chicken (KFC) According to Sob DC's strategy is to be a home meal replacement in the New England and Mid Atlantic regions DC went through an motive expansion At the end of 1901, the firm operated only 34 stores with no wranchisee stores But by the end of 1994, the total of stores company owned to and franchise stores) had increased to 534 (491 were franchise stores) it was estimated that DC's franchise store can easily beak events weekly average revenue perstore is higher than $23000. According to Reuters its stock pricehad nison steadily from $8 in November 1993 to $23 in March 1997 DC's auditor is a prestigious Big B accounting , Fehouse Young LLP. The 1994 and 1995 Incal year financial statements below wore audited numbers but the 1906 numbers were unaudited DC's excellent performance who impressed the Street Stock analyst Mke Foster of Silverman Sterling located that DC's EPs would grow an annual rate of around 35% between 1907 and 2001 and gave a strong buy rating It was rumored that the wealth Management division of Mohan Stanley took a passive 3% stake in this form Mary hedge funds followed the rumor and added DC's shares to the portfolios TABLE 1. CONSOLIDATED INCOME STATEMENTS (to continue wat Terende Net Income Per Command are a year and XXV Select Styles Editing Paragraph LLLLLLLLLLLLL LLLLLLLLL Dec 1 1 1.1 De 196 December 31 as ritra atima timitis 1 300 100,00 s Teble, et Due fredere, ritend interes Notes receivable for deve d e in 30,346 ains of widerstock 122132 SO Los in a disposal of t... 1,800 (10,0529 11.463 09 356 (10,10 Deferred franchise Purchase and other COM 2010 1,457,00 Dans leven 123 1003 B lade 401 LITE Pereira 11, Wil pall-incl. LE DO - E dit ut cathodet befinn Below is somente tror footnotes for your reference 1 Principles of Conson The conceded bruncia m e include the account of Company and its subsidies 2 Revenue Recobon evento company stores is recoged when food is sold Heyes we recogned when r ed anche wore is the Banche venge anchisees and we developments are record as even when the franchised store opens Franchisesore pays 575 of severe 3 Franchise to performance is not included in the com ediana mente DC has no galvestment agera 50 any store 4 Ave developers a large egna bandeses e boas on S p ot ma Thement confectby panduan for women DC beves that is a formal and to get back and therefore DC on the money to proceea developers canis recorded at local co The average were is around in 1990 Font Paragraph A LLLLLLLL LLLLL LLLLLLL 1996 14 841 Below are some disclosed info about all area developer Total number of area developers Total number of stores open by those developers Gross Revenue (in thousands) Total gross assets arregated for those developers (in thousands) Debt to Deluxe Chicken Inc. (in thousands) Total stockholder's equity (or deficit) (in thousands) 1995 15 627 $491, 341 $513, 926 $372, 071 (9,891) $865, 082 $640, 534 $555, 105 (102, 754) TABLE 4. NI vs. OCF Piscal Years Ended December 25, 1994 Gin thousanda) $16,173 35,918 December 31, 1995 Gin thousanda) $ 33,559 55.476 December 29, 1996 Gin thousands $ 66,958 144.910 Net Inc . Net cash provided by operating activities You are a senior auditor at Firehouse Young LLP, assigned to audit DC's 1996 financial statements in early 1997 John is the manager in charge and Kelvin Collins, a straight. A graduate from CSU Southhill, is your junior Below is some conversation between you (Y) and Kelvin (K). Y DC is not a difficult account, but audit fee is never fat. So watch out when filling time sheets. BTW, have you ever tried AP (analytical procedures) by now? K Got it, AP not done yet. But I had a quick scan of the numbers and compared net income and OCF in the last 3 years. Net income looks healthy as it is well- supported by operating cash flow. Look at the numbers below, NI/OCF ratio varies between 0.45 and 0.60. No negative OCF and no "kiss of death" in 1995 and 1996. Not a tough audit this year Required: Turn your clock back to the February 1997 As a senior auditor, please perform the analytical procedures and then write a memo to your manager in your memo, you must highlight those accounts that might be subject to material misstatements and support your conclusions with solid evidence/argument Deluxe Chicken (DC) was established in 1989 by Sebastian Bony. It sells delicious rotisserie-cooked chicken with fresh vegetables and other side dishes through its own stores and franchisee stores, just like Kentucky Fried Chicken (KFC). According to Seb, DC's strategy is to be "a home meal replacement" in the New England and Mid-Atlantic regions. DC went through an impressive expansion. At the end of 1991, the firm operated only 34 stores, with no franchisee stores. But by the end of 1994, the total of stores (company-owned stores and franchise stores) had increased to 534 (491 were franchise stores). It was estimated that DC's franchise store can easily break even if its weekly average revenue per store is higher than $23,000. According to Reuters, its stock price had risen steadily from $8 in November 1993 to $23 in March 1997. DC's auditor is a prestigious Big-8 accounting firm, Firehouse Young LLP. The 1994 and 1995 fiscal year financial statements below were all audited numbers, but the 1996 numbers were unaudited. DC's excellent performance also impressed the Street. Stock analyst Mike Foster of Silverman Sterling forecasted that DC's EPS would grow at an annual rate of around 35% between 1997 and 2001 and gave a strong buy" rating. It was rumored that the wealth management division of Mohan Stanley took a passive 3% stake in this firm. Many hedge funds followed the rumor and added DC's shares to their portfolios. Table 1. CONSOLIDATED INCOME STATEMENTS Fiscal Years Ended December 25, 1994 (in thousands) December 31, 1995 (in thousands) December 29, 1996 (in thousands) $43, 603 40,916 $ 74,662 51,566 33, 251 159, 479 11, 632 96, 151 $115,510 83,950 65,048 264, 508 19, 737 31, 137 41,367 31. 160 42, 172 99,847 Revenue: Royalties and franchise related fees........ Company stores sales............. Interest income............. Total revenue.... Costs and Expenses: Cost of products sold.......... Salaries and benefits.... General and administrative..... Relocation expense Total costs and expenses.... Income From Operations... Other Income (Expense): Interest expense, net...... Gain on issuances of subsidiary's stock. Other income, net.... Total other income (expense). Income Before Income Taxes and Minority Interest....... Incope Taxes......... Minority Interest in (Earnings) of Subsidiary......... Net Income........... 15, 876 22, 637 27,930 5.097 71,540 24,611 92,241 67.238 173, 179 91. 329 (4,235) (13, 179) (14.446) 38, 163 137 23,854 74 314 (4.161) (12,865) 20, 450 4,277 54,373 20,814 115, 183 42, 990 $16, 173 (5.235) $ 66,958 $ 33,559 TABLE 1. CONSOLIDATED INCOME STATEMENTS (to continue) Fiscal Years Ended December 25, 1994 (in thousands) December 31. 1995 (in thousands) December 29, 1996 (in thousands) Net Income Per Common and Equivalent Share... $ 0.38 $ 0.66 $ 1.01 Shares outstanding at year end (in thousands) .... 44,700 59,129 64.246 December 29, 1996 (in thousands) $ TABLE 2. CONSOLIDATED BALANCE SHEETS December 31, 1995 (in thousands) Current Assets: Cash and cash equivalents........... $ 310, 436 Accounts receivable, net............ 13,445 Due from area developers, royalty and interest. 9,614 Notes receivable from area developers, due in 12 months.. 5, 462 Prepayment and other current assets..... 4,858 Total current assets..... 343, 815 Property and Equipment, net...... 258, 550 Long-term Notes Receivable from area developers..... 450, 572 Goodwill, net......... Other Assets, net............. 20,940 Total assets................. $1,073, 877 100,800 22, 438 10,246 12,979 146, 462 334, 748 800, 519 190, 439 71, 448 $1,543, 616 $ $ Current Liabilities: Accounts payable............ Accrued expenses............ Deferred franchise revenue....... Total current liabilities...... Deferred Franchise Revenue........... Convertible Subordinated Debt......... Zero coupon bond Deferred Income Taxes...... Other Noncurrent Liabilities..... Minority Interest....... 12, 292 9,095 8.945 30. 332 2,072 129,872 177, 306 16, 631 833 40, 430 36,547 10,656 87.633 7, 740 129, 841 182, 613 40,216 6,292 153, 441 Stockholders' Equity: Common stock........... Additional paid-in capital........ Retained earnings... 591 675, 611 40,629 716, 831 $1.073, 877 642 827, 611 107,587 935, 840 $1.543, 616 Total liabilities and stockholders' equity............ Shares outstanding at year end (in thousands) ........ 59,129 64,246 TABLE 3. CONSOLIDATED CASH FLOW STATEMENTS December 25. 1994 December 31, 1995 December 29, 1996 (In thousands) (In thousands) (In thousands) Cash Flows from Operating Activities: Net income.. ... $ 16, 173 $ 33,559 66,958 Adjustments Depreciation and amortization........... 6,074 11,442 22,887 Interest expense on zero coupon bond. .. 8, 075 13,793 Gain on issuances of subsidiary's stock (38, 163) Deferred income taxes...... 12, 133 14.059 Minority interest............. 5,235 Provision for write-down of assets...... 14,550 Loss (gain) on disposal of assets. (368) 231 Changes in assets and liabilities MR & due from area developers (7, 800) (10,057) (7,193) Accounts payable and accrued expenses.... 13,724 3,661 48, 674 Deferred franchise revenue.. 5.926 (303) 3. 174 Other assets and liabilities.... (2,088) (3 265) Net cash provided by operating activities 35,918 55, 476 144.910 4,277 Cash Flows from Investing Activities: Purchase of PPE and other assets ...... (168, 797) Proceeds from the sale of PPE assets. 62,342 Loans (notes receivable) to area developers (225, 282) Repayment of notes receivable by area developers 68, 498 Net cash used in investing activities.. (263, 239) (149,231) 80,910 (661, 033) 407, 499 (321, 855) (137,432) 86, 320 (1,467,065) 993, 151 (525, 026) 125, 703 385, 360 112,863 135, 422 130,000 Cash Flows from Financing Activities: Proceeds from issuance of common stock Proceeds from issuance of subsidiary's stock Proceeds from issuance of convertible bond Proceeds from issuance of zero coupon bond Increase in deferred financing cost....... Proceeds from revolving bank credit line.... Repayments of revolving bank credit lin...... Net cash provided by financing activiti.. Net Increase (Decrease). in Cash and Cash Equivalents (7.615) 172, 464 (6,313) 229, 240 (229,240) 551, 511 285, 132 (96, 130) 248. ONS 20,767 (3 799) 43, 250 (117.256) 170, 480 (209,636) Below is some info from footnotes for your reference: 1. Principles of Consolidation. The consolidated financial statements include the accounts of the Company and its subsidiaries. 2. Revenue Recognition. Revenue from Company stores is recognized when food is sold Royalties are recognized when related franchise store revenue is generated. It is 5% of the franchise revenue. Initial franchise fees and area development fees are recognized as DC's revenue when the franchised store opens. Franchisee store also pays 5.75% of its revenue for system-wide marketing use. 3. Franchise store performance is not included in the consolidated financial statements since DC has no equity investment larger than 50% in any store. Area developers are large regional franchises which focus on major U.S. metropolitan markets. The initial investment consists of 25% equity (contributed by independent business people) and 75% loan made from Deluxe Chickens Area developers have no other sources for investment. DC believes that it is difficult for small franchises to get bank loans, therefore, DC always loan the money to support those area developers. Loan is recorded at historical cost. The average interest rate is around 8.2% in 1996. 1996 Below are some disclosed info about all area developers 1995 Total number of area developers 15 Total number of stores open by those developers 627 Gross Revenue (in thousands) $491, 341 Total gross assets aggregated for those developers (in thousands) $513, 926 Debt to Deluxe Chicken Inc. (in thousands) $372,071 Total stockholder's equity (or deficit) (in thousands) (9,891) 841 $865, 082 $640, 534 $555, 105 (102, 754) TABLE 4. NI vs. OCF Fiscal Years Ended December 25, 1994 (in thousands) $16, 173 35,918 December 31, 1995 (in thousands) $ 33, 559 55, 476 December 29, 1996 (in thousands) $ 66,958 144, 910 Net Income..... Net cash provided by operating activities You are a senior auditor at Firehouse Young LLP, assigned to audit DC's 1996 financial statements in early 1997. John is the manager in charge and Kelvin Collins, a straight-A graduate from CSU Southhill, is your junior. Below is some conversation between you (Y) and Kelvin (K). Y: DC is not a difficult account, but audit fee is never fat. So watch out when filling time sheets. BTW, have you ever tried AP (analytical procedures) by now? K: Got it, AP not done yet. But I had a quick scan of the numbers and compared net income and OCF in the last 3 years. Net income looks healthy as it is well- supported by operating cash flow. Look at the numbers below, NI/OCF ratio varies between 0.45 and 0.60. No negative OCF and no "kiss of death in 1995 and 1996. Not a tough audit this year. Required: Turn your clock back to the February 1997. As a senior auditor, please perform the analytical procedures and then write a memo to your manager. In your memo, you must highlight those accounts that might be subject to material misstatements and support your conclusions with solid evidence/argument