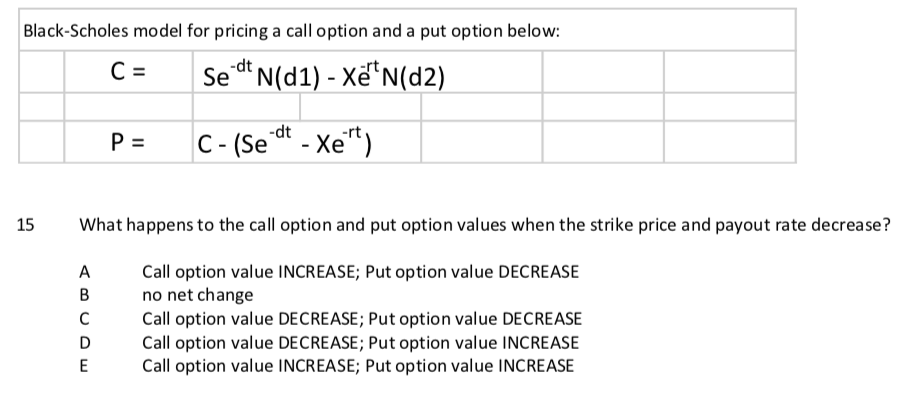

Question: Black-Scholes model for pricing a call option and a put option below: SeN(d1) - Xe'N(d2) C-(Se-dt -Xert) P = 15What happens to the call option

Black-Scholes model for pricing a call option and a put option below: SeN(d1) - Xe'N(d2) C-(Se-dt -Xert) P = 15What happens to the call option and put option values when the strike price and payout rate decrease? A Call option value INCREASE; Put option value DECREASE B no net change C Call option value DECREASE; Put option value DECREASE Call option value DECREASE; Put option value INCREASE E Call option value INCREASE; Put option value INCREASE

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock