Pete is 65 years old, married, and has three adult children. He is currently employed in the

Question:

Pete is 65 years old, married, and has three adult children. He is currently employed in the energy industry and earns roughly $1 million annually. He anticipates retiring completely from this position next year and relying solely on his portfolio to maintain his and his wife’s combined spending level of $400K annually. In addition to these portfolio assets, they also own a $2 million home in The Woodlands. Pete and his wife have no other financial assets or business interests. Beyond the value held in this portfolio, the only income they will receive is Social Security, which is not particularly impactful given their level of assets and spending. Pete is more risk averse than the average client. His approach to investing generally places wealth preservation as the top priority, followed by keeping up with inflation, and capital appreciation after that. The volatility in financial markets during the onset of the Covid crisis was unsettling to Pete despite his ability to “weather the storm.”

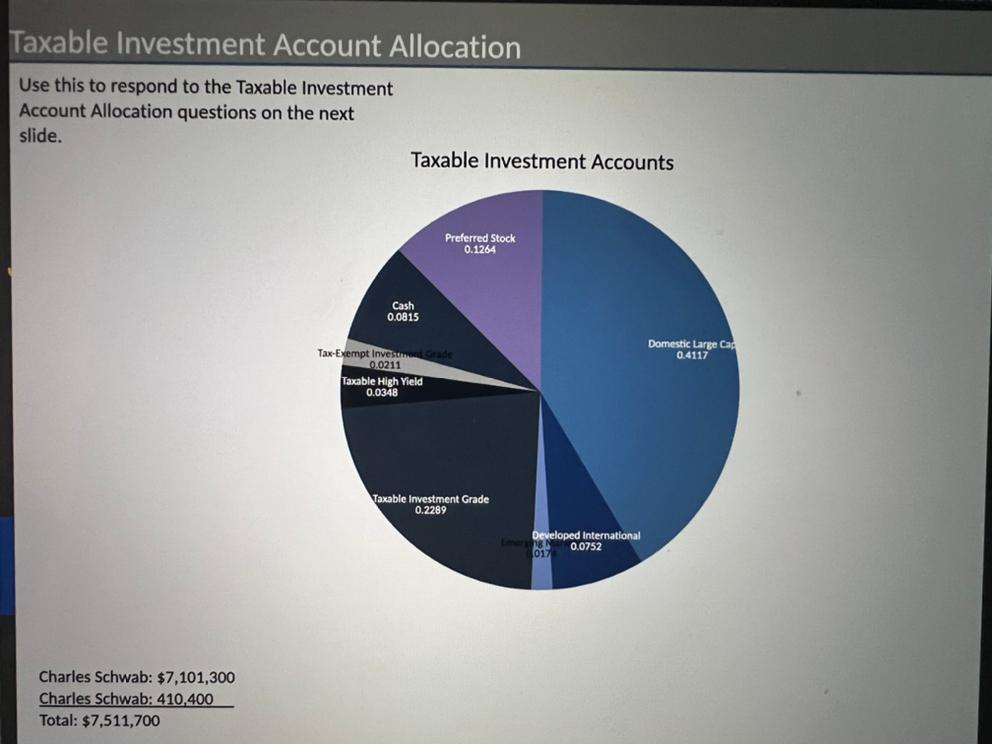

- Given Pete’s high level of income, is the large allocation to taxable bonds in a taxable account appropriate? If not, how could it be corrected to be a more efficient bond allocation?

Expert Answer:

Given Petes high level of income is the large allocation to taxable bonds in a taxable account appro... View the full answer