Question: Brownien Motion version: March 30, 2021 Consider the following simple model for the exchange rate between USD and EUR. The conversion rate from USD to

Brownien Motion

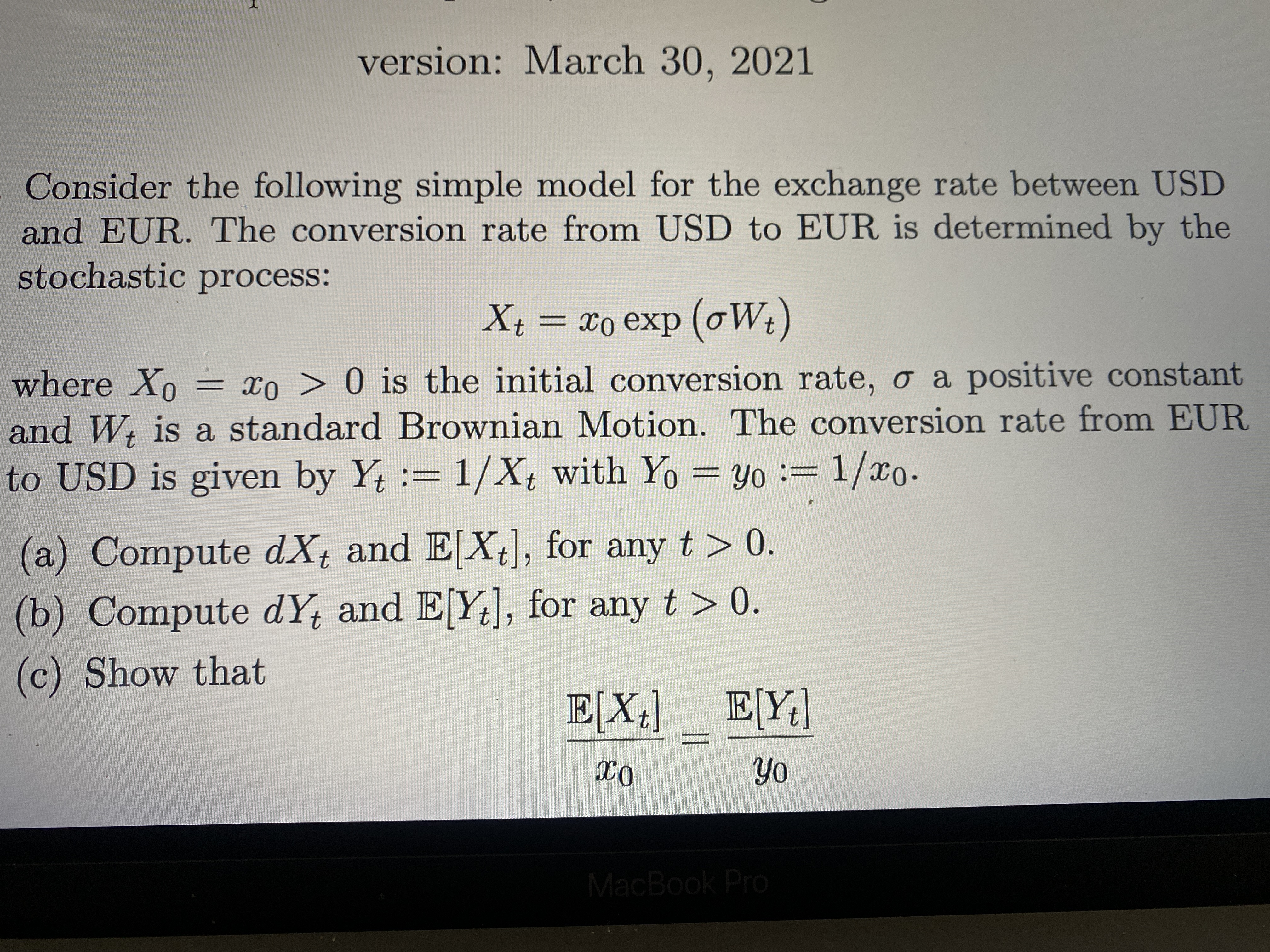

version: March 30, 2021 Consider the following simple model for the exchange rate between USD and EUR. The conversion rate from USD to EUR is determined by the stochastic process: Xt = No exp (oWt) where Xo = x0 > 0 is the initial conversion rate, o a positive constant and We is a standard Brownian Motion. The conversion rate from EUR to USD is given by Yt := 1/ Xt with Yo - yo := 1/xo. (a) Compute dXt and E[Xt], for any t > 0. (b) Compute dYt and E[Y+], for any t > 0. (c) Show that EX.] EY.] yo MacBook Pro

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock