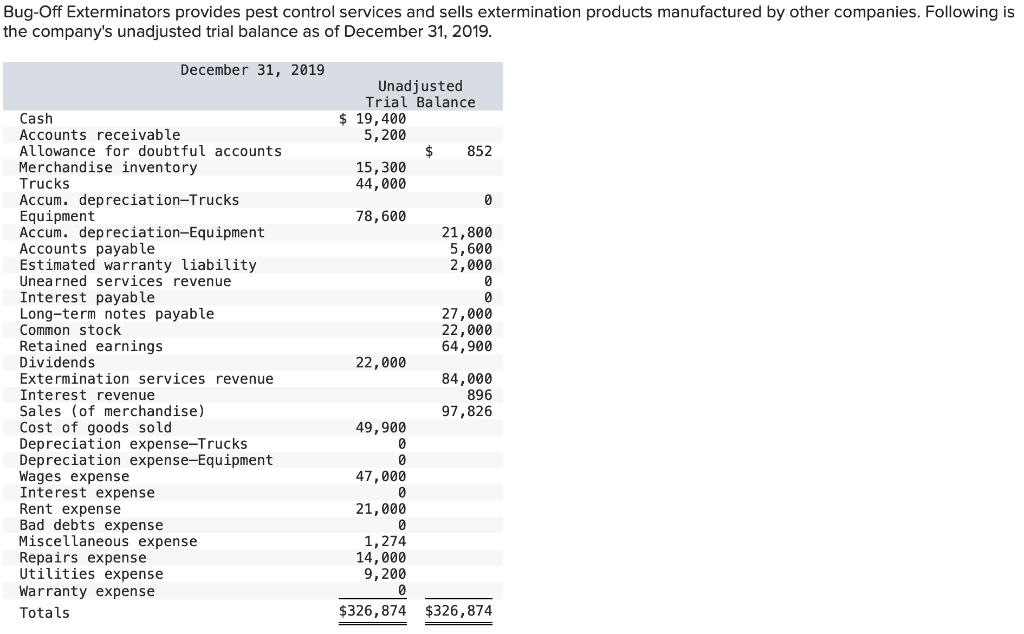

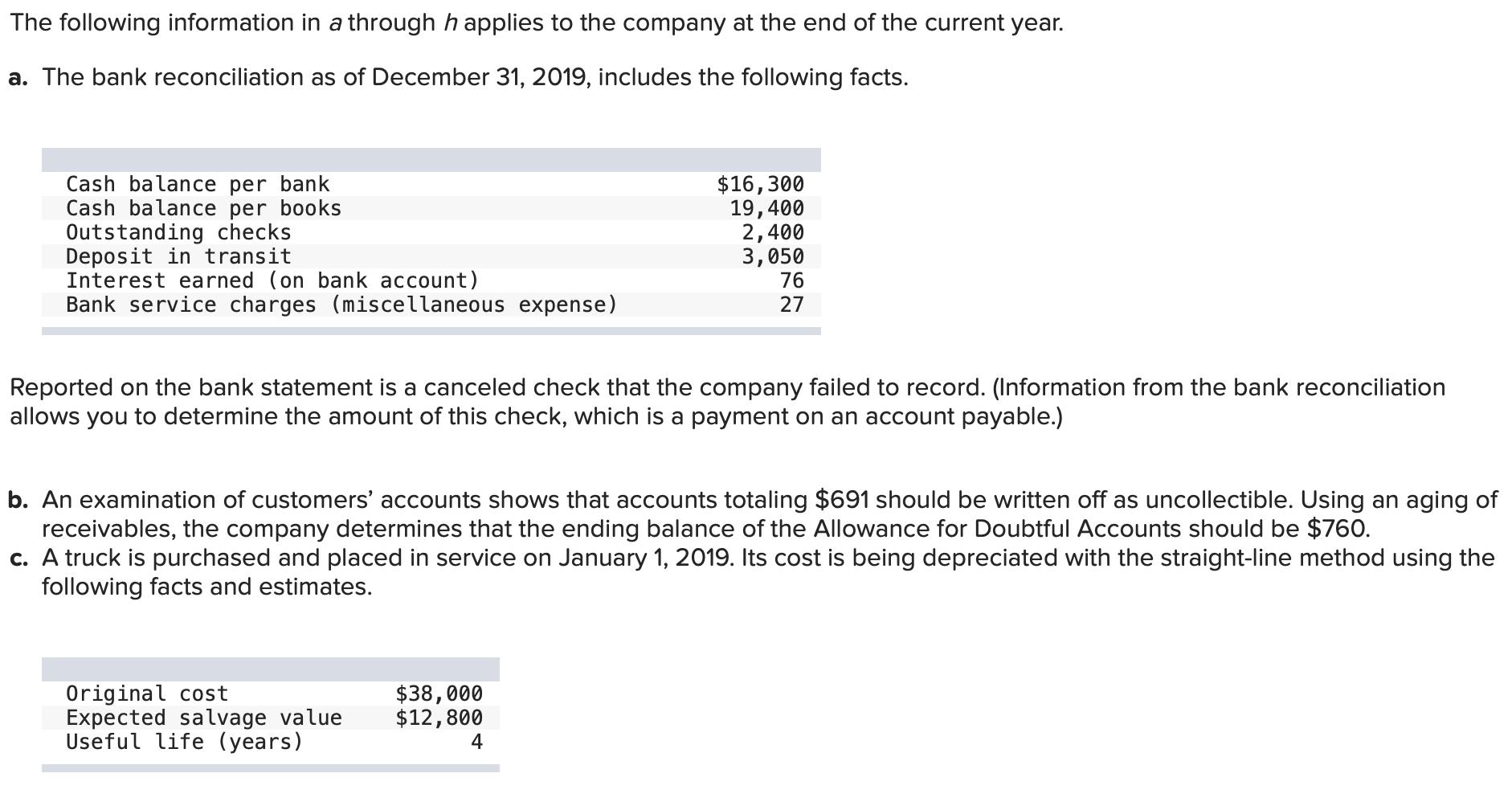

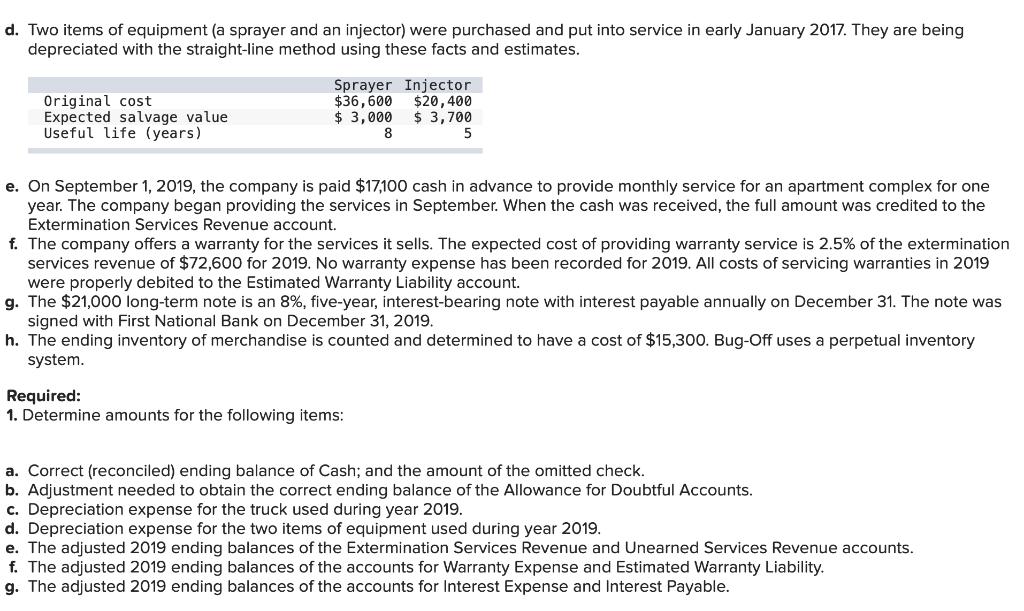

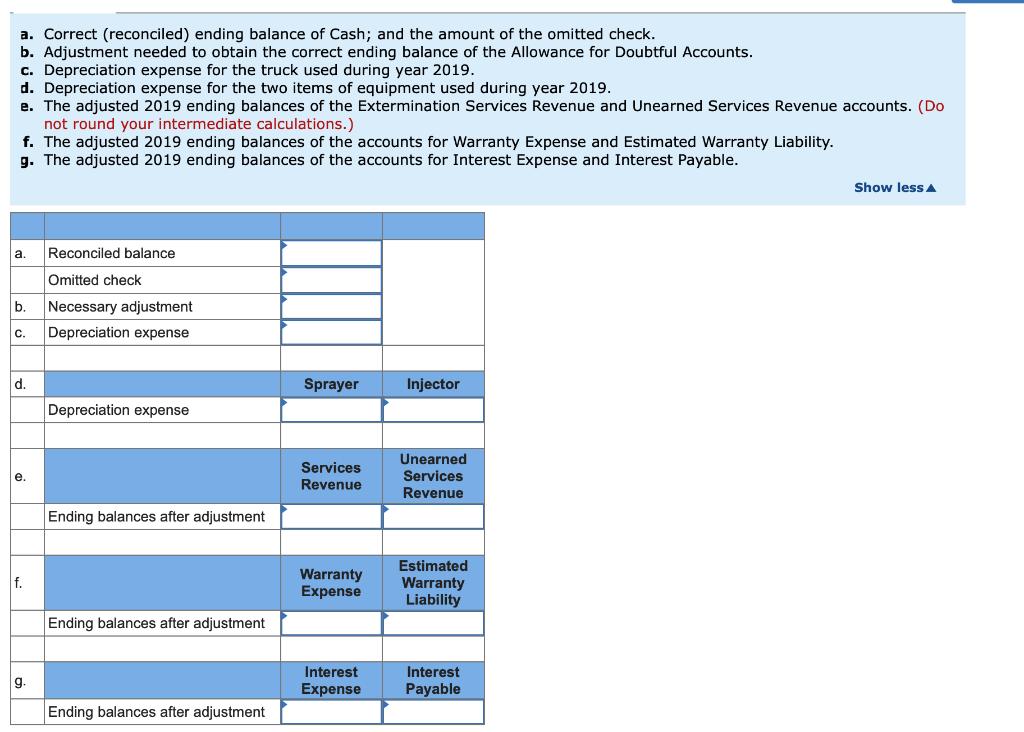

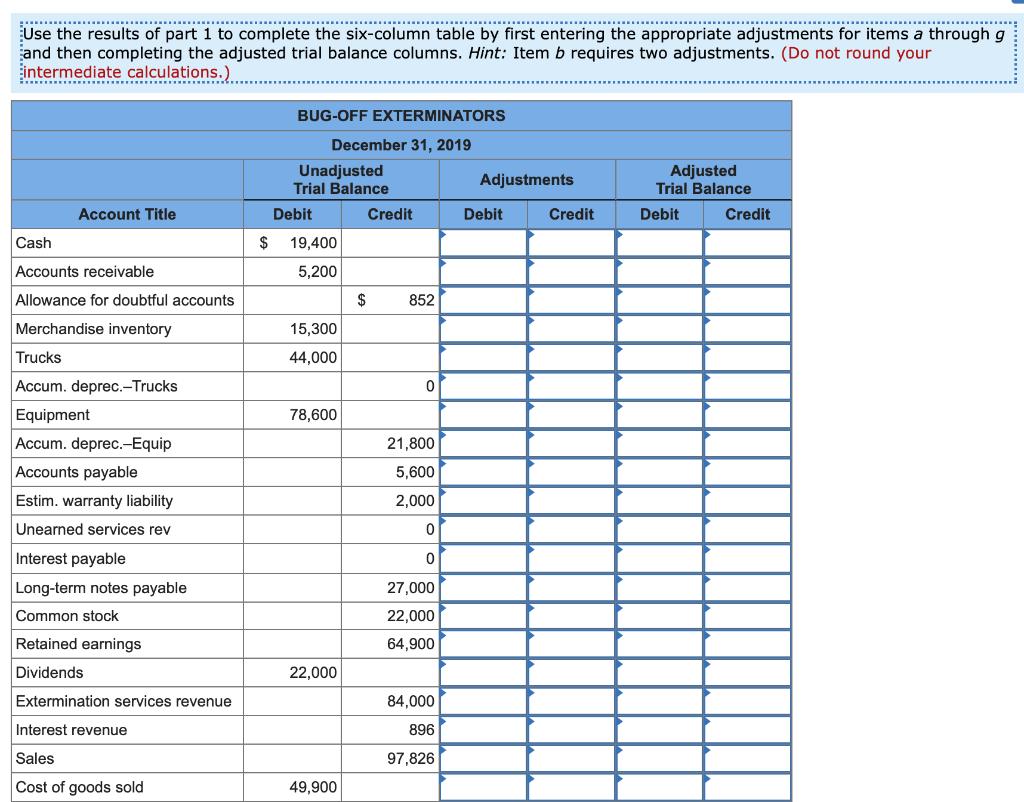

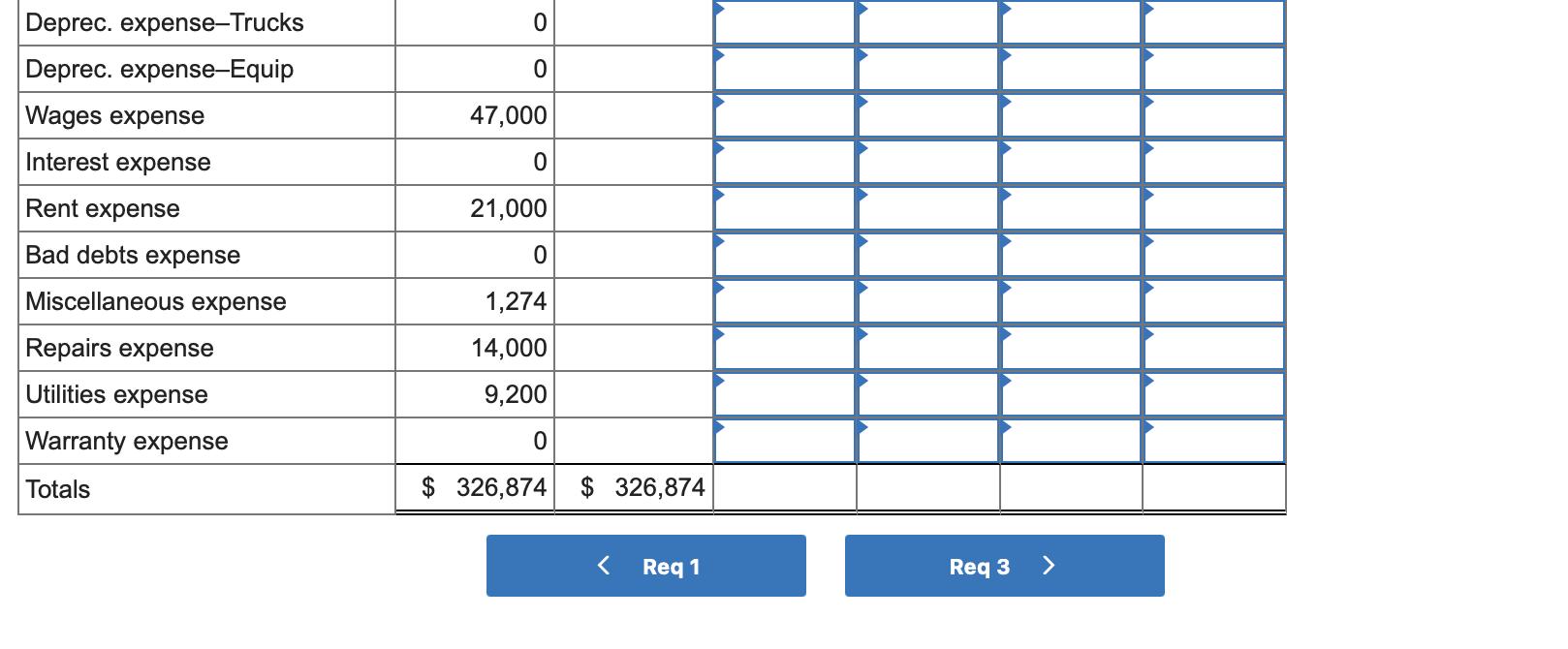

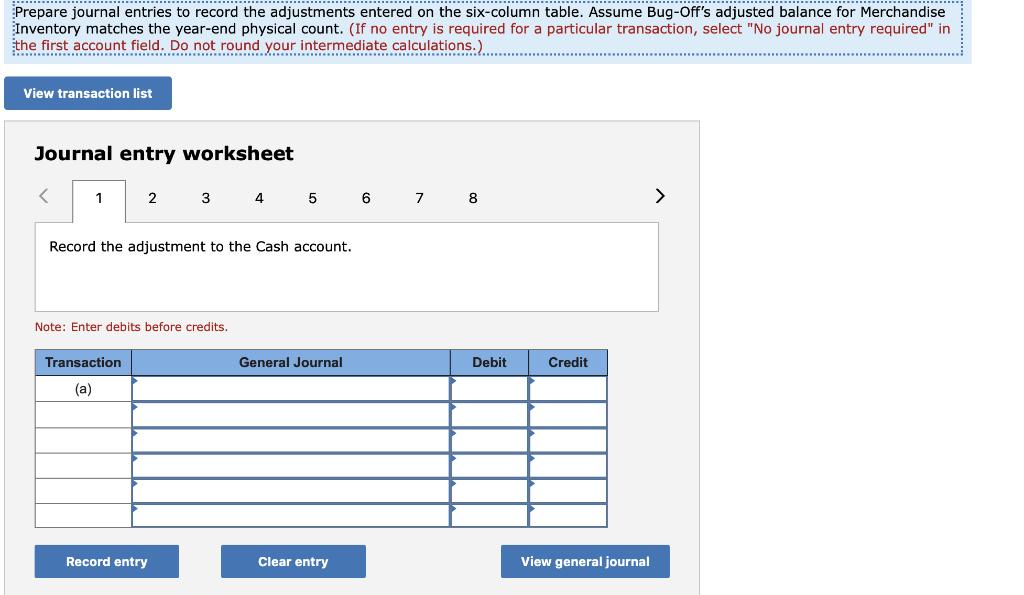

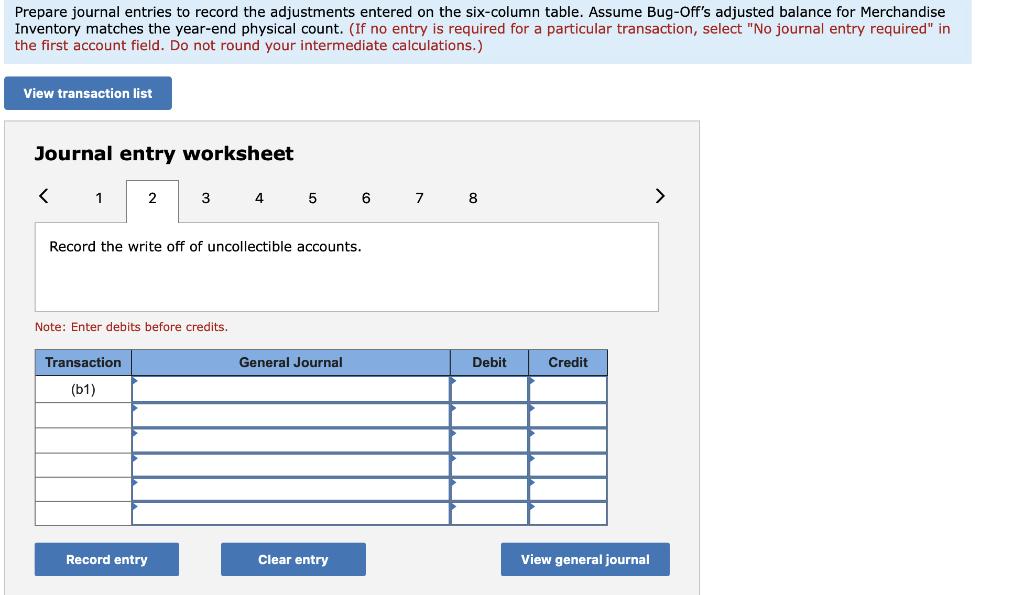

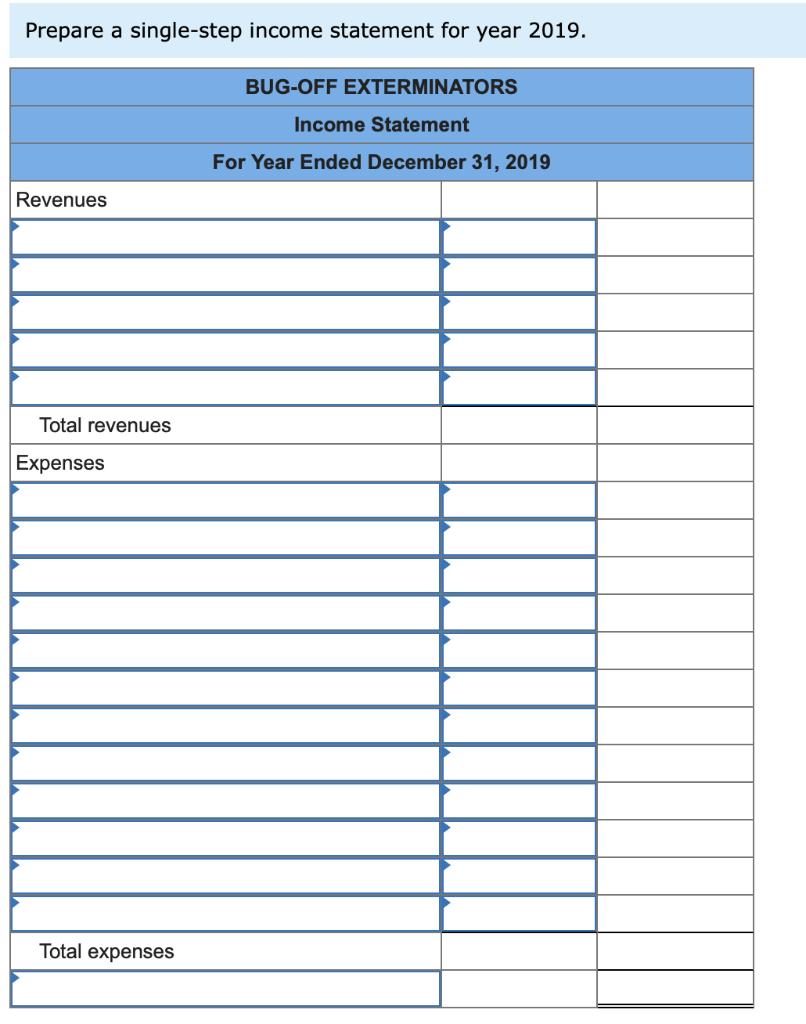

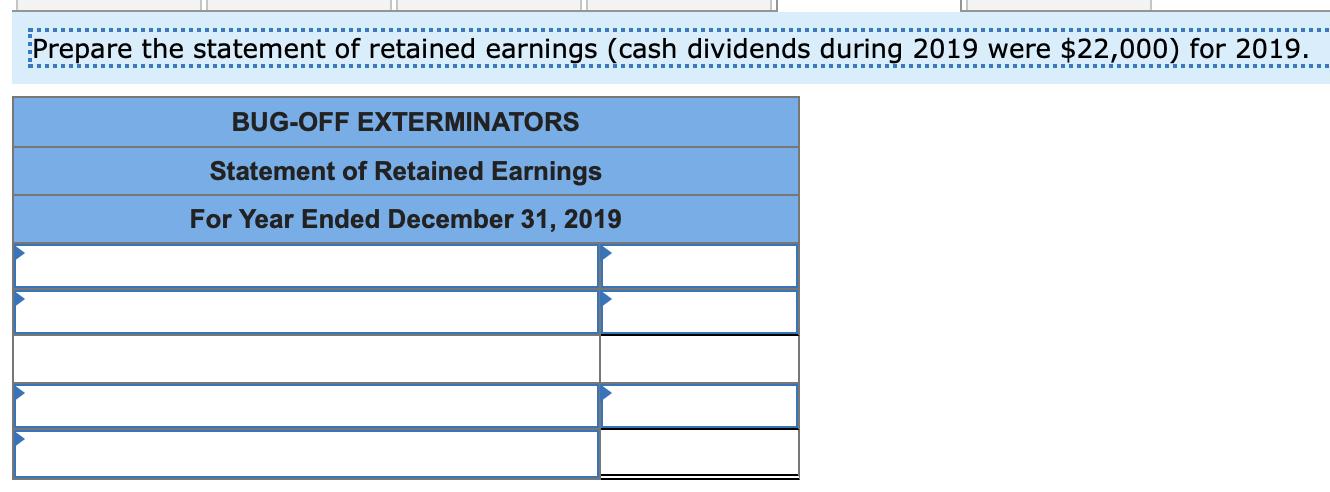

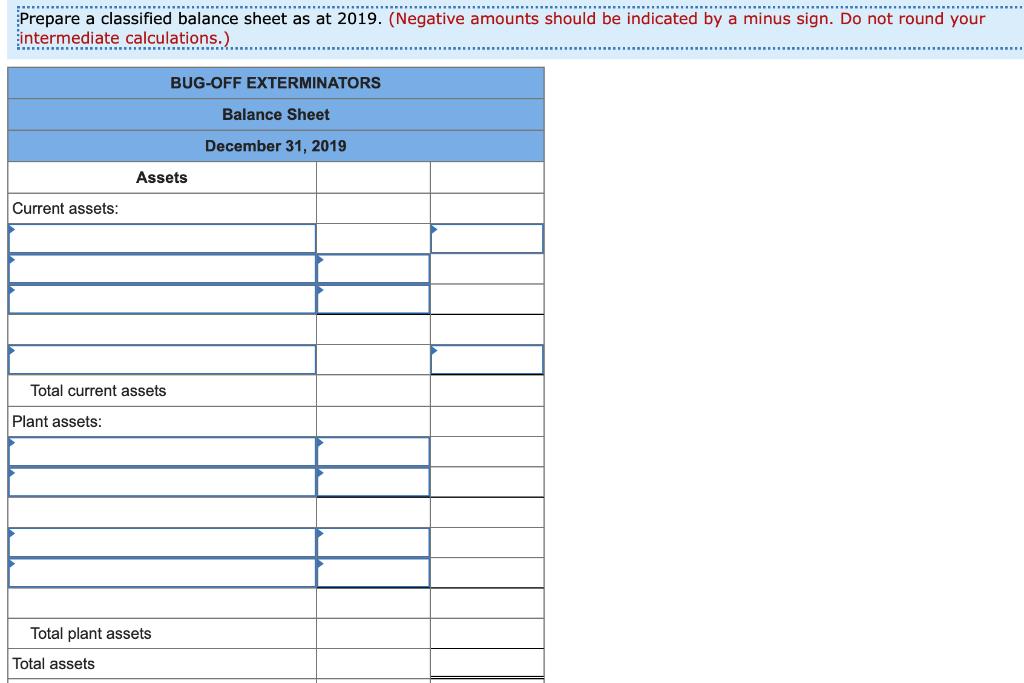

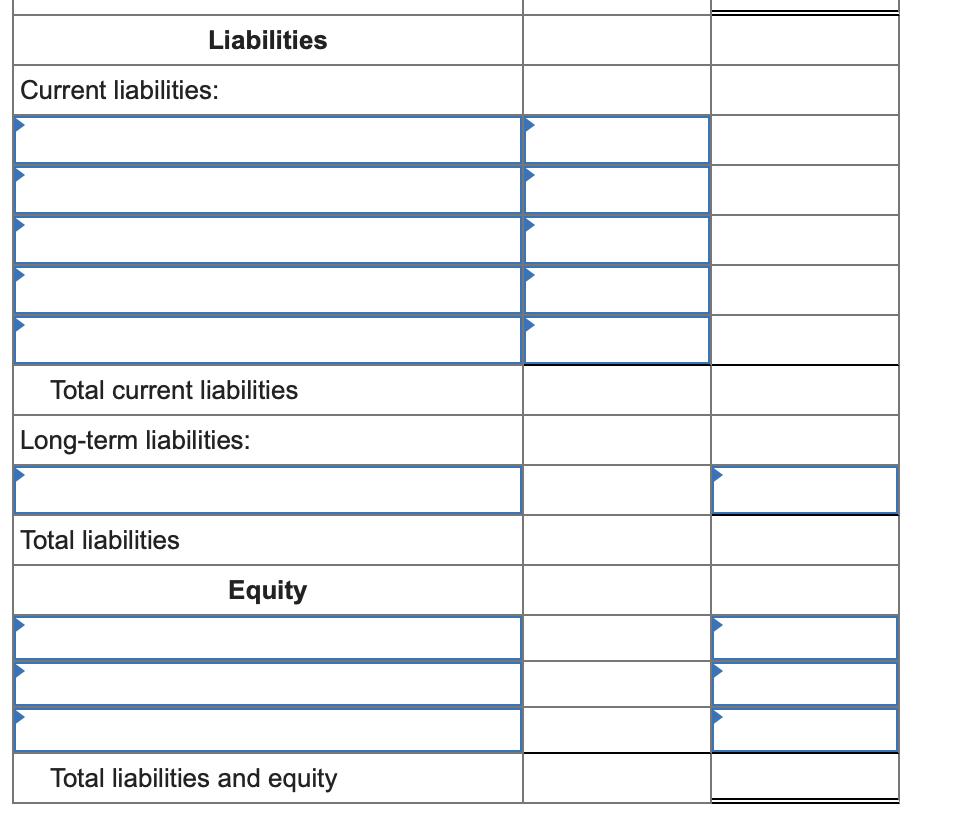

Question: Bug-Off Exterminators provides pest control services and sells extermination products manufactured by other companies. Following is the company's unadjusted trial balance as of December