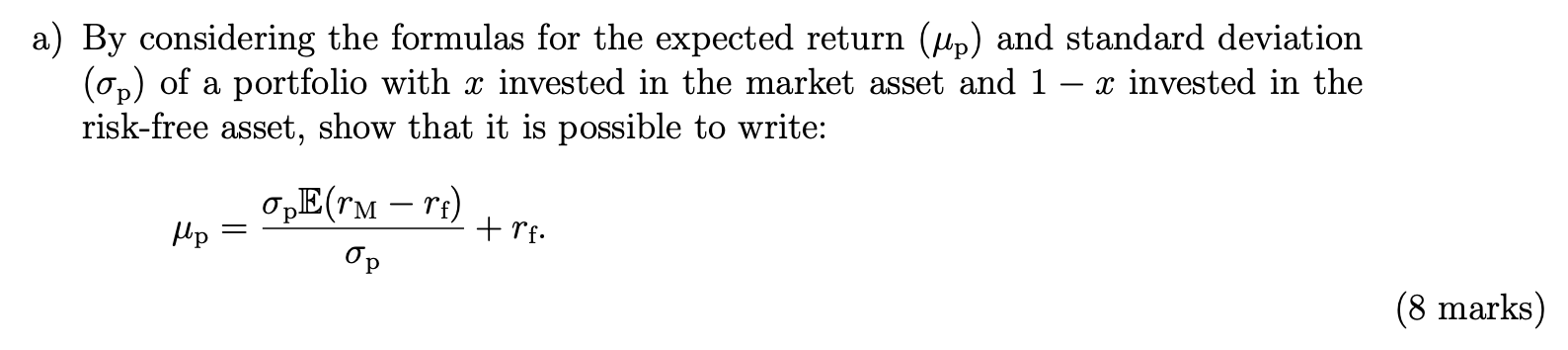

Question: By considering the formulas for the expected return (p) and standard deviation (p) of a portfolio with x invested in the market asset and 1

By considering the formulas for the expected return (p) and standard deviation (p) of a portfolio with x invested in the market asset and 1 x invested in the risk-free asset, show that it is possible to write: p = pE(rM rf) p + rf . (8 marks)

a) By considering the formulas for the expected return (up) and standard deviation (op) of a portfolio with x invested in the market asset and 1 x invested in the risk-free asset, show that it is possible to write: o E(rm rt) +re Mp Op (8 marks)

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock