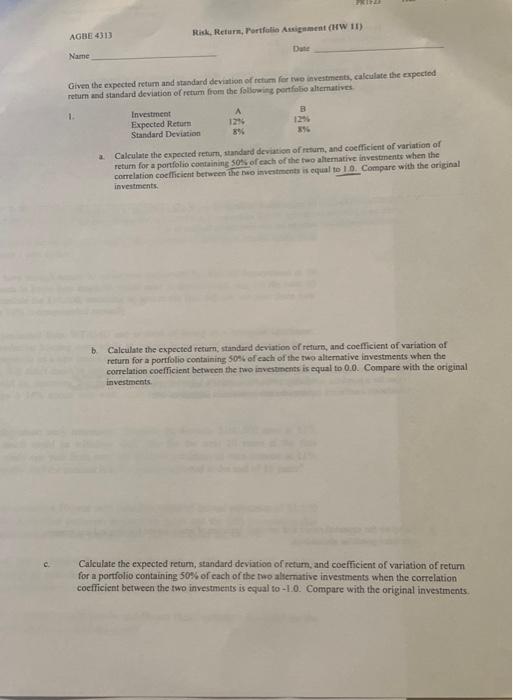

Question: C. AGBE 4313 Name 1. Given the expected return and standard deviation of return for two investments, calculate the expected return and standard deviation of

AGBE 4) Risk, Return, Rortfoli Assignment (HW if) Name Daite return and standard deviation of retum from the followe is 3 ponfolio alternatives 1. correlation coefficient between the nso investrocnts is equal to 1.0 . Compare with the ariginal invelments. b. Calculate the expoctod retim, standard deviation of refium, and coefficient of variation of refurn for a portfolio containing 5046 of each of the two alternative investments when the correlation coefficient betwren the rwo investrents is equal to 0.0 . Compare with the original investments: Calculate the expected retum, standard deviation of return, and coefficient of variation of return for a portiolio containing 50% of cach of the two aliemative investments when the correlation coefficient between the two investments is equal to -1.0 . Compare with the original investiments

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts