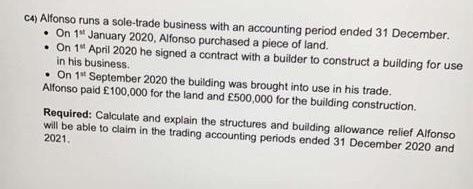

C4) Alfonso runs a sole-trade business with an accounting period ended 31 December. On 1st...

Fantastic news! We've Found the answer you've been seeking!

Question:

Transcribed Image Text:

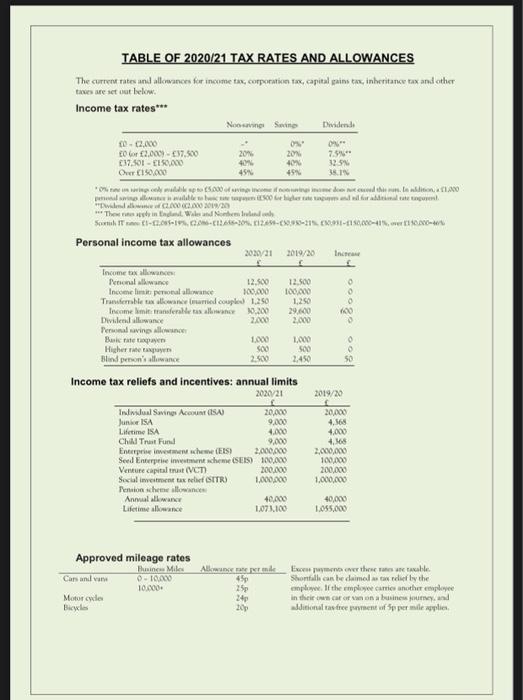

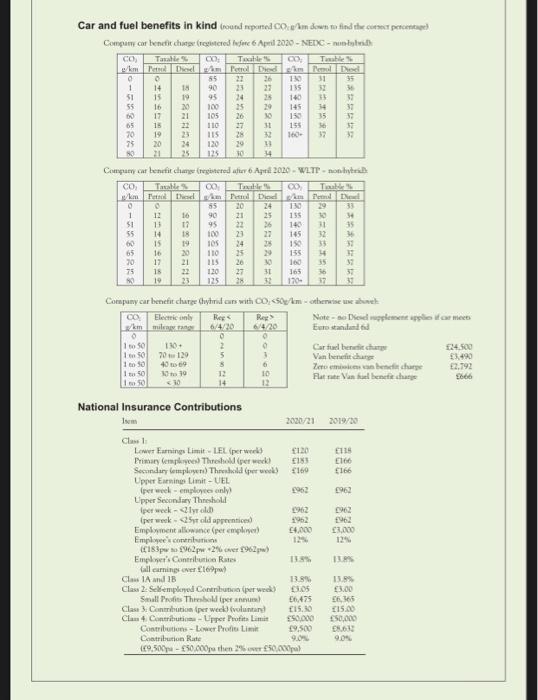

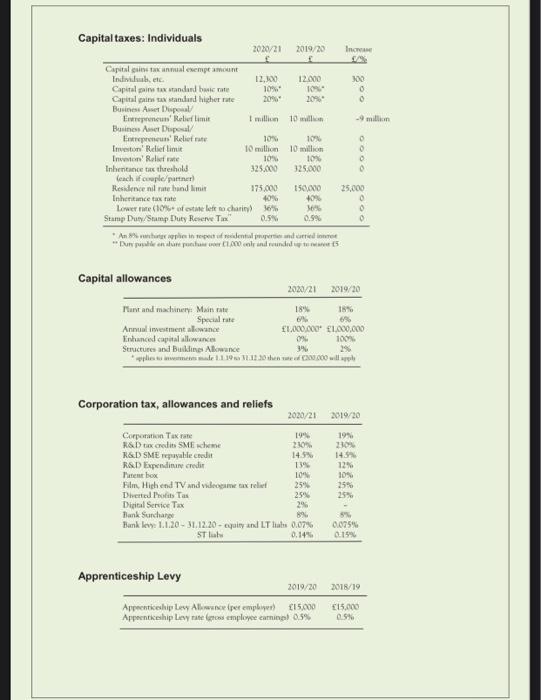

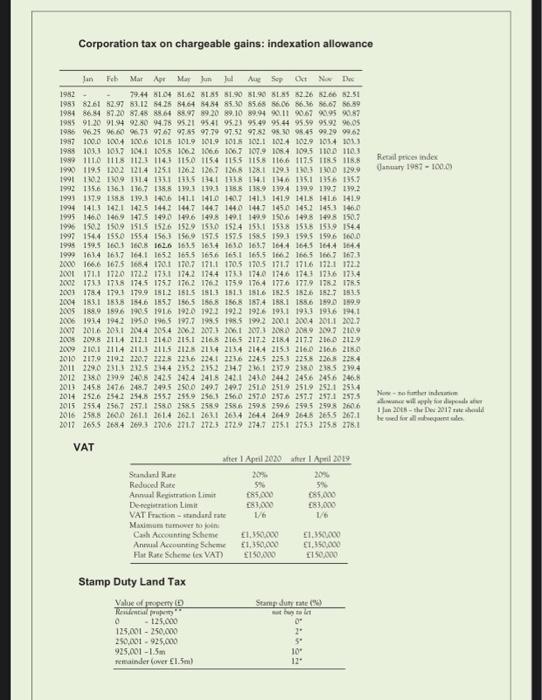

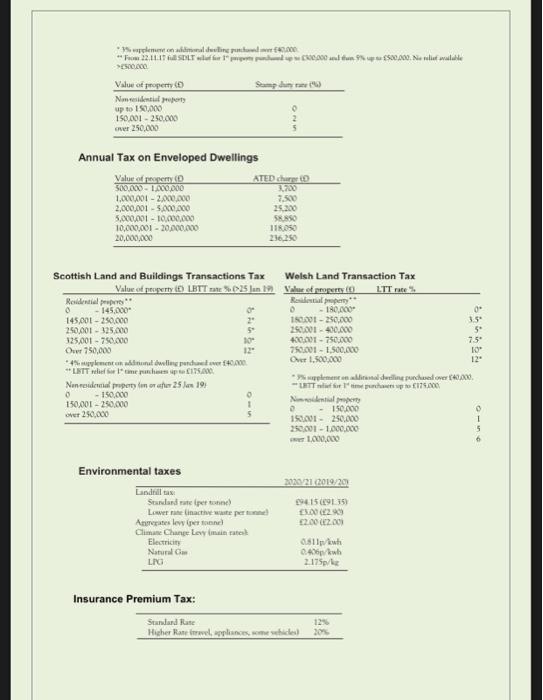

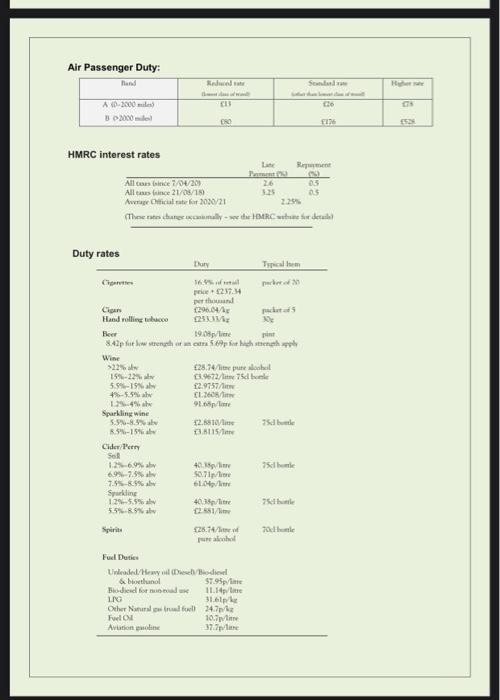

C4) Alfonso runs a sole-trade business with an accounting period ended 31 December. • On 1st January 2020, Alfonso purchased a piece of land. • On 1st April 2020 he signed a contract with a builder to construct a building for use in his business. • On 1 September 2020 the building was brought into use in his trade. Alfonso paid £100,000 for the land and £500,000 for the building construction. Required: Calculate and explain the structures and building allowance relief Alfonso will be able to claim in the trading accounting periods ended 31 December 2020 and 2021. TABLE OF 2020/21 TAX RATES AND ALLOWANCES The current rates and allowances for income tax, corporation tax, capital gains taxx, inheritance tax and other taxes are set out below. Income tax rates*** 10-12,000 to or £2,000)-£37,500 £37,501-£150,000 Over £150,000 Personal savings allowance Basic rate payen Higher rate taxpayer Blind person's allowance Income tax allowances Personal allowance Income limit personal allowance Transferable tax allowance (married coupled 1.250 Income limit transferable tas allowance 30.000 Dividend allowance 2.000 Cars and an penal single is available to be tape 500 for higher rate tages and all for additional tate toge "Dividend allowance of C2000 2000 2019/20 The res apply in England Wales and No Sortih IT E-12085-19%, 120-1266-20% 1259-09-21% 01-1150,000-41% over 15000- Personal income tax allowances Motorcycles Bicycles Noosavings Sing Individual Savings Account (ISA) Junior ISA Lifetime ISA 20% Approved mileage rates Business Miles 0-10,000 10,000 Venture capital trust (VCT) Social investment tax relief (STR) Pension scheme allowances Annual allowance Lifetime allowance 2020/21 2019/20 f 12,500 100,000 Child Truit Funl Enterprise investment scheme (EIS) Seed Enterprise investment scheme (SEIS) 1,000 500 2,500 Income tax reliefs and incentives: annual limits 2020/21 20% 40% 0%" 12,500 100,000 20,000 9,000 4.000 9,000 2,000,000 100,000 200,000 1,000,000 Allowance rate per mde 45p 25p 24p 20p 40,000 1,073,100 1,250 29,600 2,000 1,000 500 2450 Dividends 0%" 7.5%** 32.5% 38.1% Increase ०००००००० 600 2019/20 50 f 20,000 4,368 4,000 4,368 2,000,000 100,000 200,000 1,000,000 40,000 1,055,000 Excess payments over these rates are taxable. Shortfall can be claimed as tax relief by the employee. If the employee carries another employee in their own car or van on a business journey, and additional rasfree psement of 5p per mile applies. Car and fuel benefits in kind (round reported CO, g/km down to find the corect percentage) Company car benefit charge (registered before 6 April 2020-NEDC-nuolybrid Co CO; Table e/km Petrol Diesel km Petrol Died 0 1 51 $2883: 55 16 60 17 18 20 80 21 CO₂ /km 0 1 $1 55 75 80 CO km 0 14 15 0 1 to 50 1 to 50 to 50 19 1 1 to 50 150 Isem 12 13 14 18 19 20 21 22 23 24 25 15 16 16 17 85 90 95 100 105 110 115 120 125 130+ 70129 40 to 69 30 to 30 30 95 18 100 19 105 20 110 21 115 18 22 120 19 23 125 CO₂ Taxable% km Penol Died 26 130 23 27 135 24 28 140 Reg 6/4/20 HAAAABAAR 0 2 5 8 12 14 22 25 26 Company car benefit change (registered after 6 Aprill 2020-WLTP-non-hybri Taxable% 00 Truble Fetsol Diesel km Petrol Diod g/km 0 130 135 30 140 31 145 150 55 20 90 (all earnings over £169) 27 28 29 30 S8825855 21 22 24 27 National Insurance Contributions ABARRERAS 30 31 155 32 160- 33 29 145 34 150 34 24 25 26 28 29 30 31 32 Company car benefit charge (hybrid cars with CO, <50g/km-otherwise use abiel Reg Electric only mileage range 6/4/20 O O 3 6 10 12 Class 1 Lower Earnings Limit-LEL (per week Primary (employees) Threshold (per week) Secondary employers) Threshold (per week) Upper Earnings Limit - UEL (per week-employees only) Upper Secondary Threshold (per week-21yr old) (per week-<25yr old apprentices) Employment allowance (per employer) Employee's contributions (183pw to £962pw 2% over £962) Employer's Contribution Rates Class 1A and 18 Class 2: Selemployed Contribution (per week) Small Profits Threshold (per annum) Class 3. Contribution (per week) (voluntary) Clan 4 Contributions - Upper Profits Limit Contributions-Lower Profi Limit Contribution Rate £120 £183 £160 £962 31 37 1962 1962 £4,000 SEGIHAN 2020/21 33 13.8% 00₂ Tiable % 13.8% £3.05 £6,475 35 36 32 (£9,500-£50,000pa then 2% over £50,000pal BARRERR 35 36 33 155 34 160 35 165 36 37 170- 37 37 £15.30 £50,000 £9,500 9.0% 37 Fed Dil 29 33 37 37 37 34 35 36 Note-no Diesel upplement applies if car meets Euro standard 6d Car fuel benefit change Van benefit charge Zero emosies van benefit charge Flat rate Van fuel benefit change 2019/20 £118 £166 £166 £962 1962 £962 £3,000 12% 13.8% 13.8% £3.00 £6,365 £15.00 £50,000 18,632 9.0% £24.500 £3,490 £2,792 £666 Capital taxes: Individuals Capital gains tax annual exempe amount Individual, etc. Capital gains tax standard basic rate Capital gains tax standard higher rate Business Asset Disposal Entrepreneurs' Relief limit Business Asset Disposal/ Entrepreneurs' Relief te Investor Relief limit Investon' Relief rate Inhentance tax threshold (each if couple/partner) Residence nil rate band limit Capital allowances 2020/21 2019/20 Plant and machinery: Main rate Special rate Inheritance tax rate Lower rate (10% of estane left to charity) Stamp Duty/Stamp Duty Reserve Tax 12,300 10% 20%* 20% I million 10 million 10% 10% 10 million 10 million 10% 10% 325,000 325,000 175,000 40% 36% Apprenticeship Levy 0.5% 12.000 applies in respect of residential properties and carried in *An 8% "Duy puble on share ponchuse over 1000 only and rounded up to 15 Corporation tax, allowances and reliefs Corporation Tax rate R&D tax credits SME scheme R&D SME repayable credit R&D Expenditure credit Patentbox Film, High end TV and videogame tax relief Diverted Profits Tas 0.9% 150,000 25,000 40% 36% Annual investment allowance Enhanced capital allowances Structures and Buildings Allowance *applies to investments made 1.1.19s 31.12.20 then of 200,000 will appl 2020/21 19% 230% 14.5% 13% 10% 25% 25% 2% Digital Service Tax Bank Surcharge 8% Bank levy: 1.1.20- 31.12.20-equity and LT lis 0.07% ST lab 0.14% Increase 5/% 300 0 0 2019/20 2020/21 18% 18% 6% 6% £1,000,000 £1,000,000 0% 3% Apprenticeship Levy Allowance (per employer) £15,000 Apprenticeship Levy rate (gross employee earnings) 0.5% -9 million 0000 100% 2% 2019/20 0 0 0 8% 0.075% 0.15% 2019/20 19% 230% 14.9% 12% 10% 25% 25% 2018/19 £15,000 0.5% Corporation tax on chargeable gains: indexation allowance Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec 1982 1983 82.61 82.97 1984 86.84 87.20 79.44 81.04 81.62 8185 81.90 81.90 8185 8226 8266 82.51 83.12 84.25 84.64 84.34 85.30 85.68 86.06 86.36 86.67 86.89 87.48 88.64 88.97 89.20 89.10 89.94 90.11 90.67 9095 90.87 1985 91.20 91.94 92.80 94.78 95.21 9541 95.23 95.49 95.44 95.59 95.92 96.05 1986 96.25 96.60 96.73 97.67 97.85 97.79 97.52 97.82 98.30 98.45 99.29 99.62 1987 100.0 1004 1006 1015 1019 101.9 101 102.1 1024 102.9 103.4 103.3 1988 1033 103.7 104.1 105.5 106.2 106.6 106.7 107.9 108.4 1095 1100 1103 1999 1110 1118 1123 1143 1150 1154 1155 1158 1166 1175 1185 118.8 1990 119.5 1202 1214 1251 126.2 1267 126.8 128.1 129.3 130.3 130.0 129.9 1991 130.2 1309 1314 1331 1335 1341 1338 1341 1346 1351 135.6 135.7 1992 135.6 136.3 136.7 138.5 139.3 139.3 1388 1389 1394 1399 139.7 139.2 1991 137.9 1388 139.3 1406 141.1 141.0 140.7 1413 1419 1418 1416 1419 1994 1413 142.1 142.5 1442 1447 1447 1440 144.7 1450 145.2 1453 146.0 1995 1460 1469 1475 1490 1496 1498 149.1 1499 1506 1498 1498 150.7 1996 1502 1509 1515 1526 1529 1530 1524 1531 1538 1538 1539 154.4 1997 1544 1550 1554 1563 1569 1575 1575 158.5 1993 1995 1596 160.0 1998 199.5 1601 1608 1626 1635 1634 163.0 163.7 164.4 164.5 164.4 164.4 1999 1634 1637 164.1 1652 1655 1656 1651 1655 1662 1665 1667 167.3 2000 166.6 1675 1684 1701 1707 1711 1705 1705 171.7 1716 1721 1722 2001 171.1 1720 172.2 1751 1742 1744 1733 1740 1746 1743 1736 1734 2002 1733 1738 1745 1757 1762 1762 1759 1764 1776 1779 1782 178.5 2003 1784 1793 1799 1812 1815 1813 1813 1816 1825 1826 1827 1835 2004 1831 1838 1846 1857 1865 1868 1568 1874 1881 2005 188.9 1896 1905 1916 1920 1921 1922 1926 1931 2006 1934 1942 1950 1965 197.7 1985 1985 199.2 2001 2007 2016 2031 2044 2054 2062 2073 2061 2073 2080 2089 209.7 210.9 2008 209.8 2114 2121 2140 215.1 2168 2165 2172 2184 2177 2160 2129 2009 2101 2114 2113 2115 2128 2134 2134 214.4 2153 2160 2166 218.0 2010 217.9 2192 220.7 1225 2236 2241 2236 224.5 2253 2258 2268 228.4 2011 2290 2313 232.5 2344 2352 2352 2347 2361 2379 2380 2385 2394 2012 2380 2999 240.8 2425 2424 2418 242.1 2430 244.2 2456 2456 246.8 2013 2458 2476 248.7 2495 250.0 249.7 249.7 2510 2519 2519 2521 2534 2014 252.6 2542 254.8 255.7 2559 2563 2560 257.0 257.6 257.7 2574 257.5 2015 2554 2567 257.1 258.0 2585 2589 2586 2598 2596 259.5 2598 260.6 2016 2588 2600 261.1 2614 262.1 2631 2634 2644 2649 2648 265.5 267.1 2017 265.5 2684 269.3 2706 271.7 272.3 2729 274.7 275.1 275.3 275.8 278.1 1886 1590 159.9 1933 1936 194.1 2004 2011 202.7 VAT Standard Rate Reduced Rate Annual Registration Limit Deregistration Limit VAT Fraction-standard rate Maximum tumover to join Cash Accounting Scheme Annual Accounting Scheme Flat Rate Scheme (ex VAT) Stamp Duty Land Tax Value of property ( Rendential property 0 -125,000 after 1 April 2020 after 1 April 2019 20% 3% €85.000 £83,000 1/6 125,001-250,000 250,001-925,000 925,001-1.5m remainder (over £1.5m) 20% 5% £85,000 £83,000 1/6 £1,350,000 £1,350,000 £150,000 £1,350,000 £1,350,000 £150,000 Stamp duty rate (%) 2" Sº 10" Retail prices index January 1987-100.00 New-nofher indexation ance will apply for depends ar 1 Jan 2018-the Dec 2017 te should be used for all subsequent sales 3% plemene on additional desling punch From 22.11.17 full SDLT wlff 1p >500.000 Value of property ( Nam idential property up to 150,000 150,001-250,000 over 250,000 20,000,000 Annual Tax on Enveloped Dwellings Value of property ( 500.000-1.000.000 1,000,001-2,000,000 2,000,001-5,000,000 5,000,001-10,000,000 10,000,001-20,000,000 Residential property 0 -145,000 0 145,001-250,000 250,001-325,000 325,001-750,000 Over 750,000 Scottish Land and Buildings Transactions Tax Value of property (0) LBTT rate %025 Jan 19 Nonresidencial property on or after 25 Jan 19: - 150,000 150,001-250,000 over 250,000 4% supplement on additional dwelleng panded over 140,000 LETT relief S1 came punches up to £175,000 Environmental taxes 40,000 pundup C00,000 and 9% up to £500,000. Nellable Stamp duty rate (6) Electricity Natural Gas LPG - - - 1 ATED charge (O 3,700 7,500 25,200 10° 12" Angregates levy (per tonne) Climate Change Levy (main rates Standard rate (per tonne) Lower rate (inactive waste per tunnel 58,850 118,050 236,250 Welsh Land Transaction Tax LTT rate% Value of property (0) Residential property** 0 -180,000 180,001-250,000 250,001-400,000 400,001-750,000 750,001-1,500,000 Over 1,500,000 Nimnidential property 0 - 150,000 150,001 - 250,000 250001-1,000,000 1,000,000 2020/21 (2019/20 £94.15 (291.35) £5.00 (£2.90) £2.00 (200) 9% supplement on additional dwelling purchased over £40,000. LETT forme purchases up to £175.000 0811p/kwh 0.406p/kwh 2.175p/kg 0* 3.5° 5° Insurance Premium Tax: Standard Rate Higher Rate (travel, appliances, some vehicles) 20% 7.5 10⁰ 12⁰ 9150 6 Air Passenger Duty: Rand A10-2000 miles) B2000) HMRC interest rates Duty rates Cigan Hand rolling tobacco Wine >22% alw 15%-22% 5.9%-15% 4%-5.5% al 12%-4% a Sparkling wine 5.5%-85% av 8.5%-15% Cider Perry Sol 1.2% 6.9% aby 6.9%-7.5% av 7.5%-85% av All cars since 7/04/20 All taxes (ince 21/08/18) Average Official rate for 2020/21 2.29% (These rate change occally-see the HMRC webne for deta Sparkling 12%-5,5% av 5.5%-85% Spirits Redwol ta Dury Beer 19.08/e pint 8.42p for low strength or an cars 5.69p for high strength apply E13 080 16.9% price+237.34 per thousand 1296.04/3g (23333/ 12.8810/ £3.8115/ 4038/ 50.71p/le £25.74/ £28.74/lit pure alcohol £3.9672/ 75cl bon 12.9757/ EL.2608/ 40.35p/litre £2581/ LPG Other Natural girl full Fuel Ol Aviation puoline Lane Pement 26 3.25 Fuel Duties Unleaded/Heavy oil (Diesel/Biodiesel & bioethanol Biodiesel for non-road use $7.95/ 11.14p/le 31.6l/kg 24.7p/k 10.7p/li 37.7p/le Typical hem parker of 20 packet of 5 30e Regument 2 05 0.5 751 ble 75db Sondad 70 bole £26 1176 Higher 175 £528 C4) Alfonso runs a sole-trade business with an accounting period ended 31 December. • On 1st January 2020, Alfonso purchased a piece of land. • On 1st April 2020 he signed a contract with a builder to construct a building for use in his business. • On 1 September 2020 the building was brought into use in his trade. Alfonso paid £100,000 for the land and £500,000 for the building construction. Required: Calculate and explain the structures and building allowance relief Alfonso will be able to claim in the trading accounting periods ended 31 December 2020 and 2021. TABLE OF 2020/21 TAX RATES AND ALLOWANCES The current rates and allowances for income tax, corporation tax, capital gains taxx, inheritance tax and other taxes are set out below. Income tax rates*** 10-12,000 to or £2,000)-£37,500 £37,501-£150,000 Over £150,000 Personal savings allowance Basic rate payen Higher rate taxpayer Blind person's allowance Income tax allowances Personal allowance Income limit personal allowance Transferable tax allowance (married coupled 1.250 Income limit transferable tas allowance 30.000 Dividend allowance 2.000 Cars and an penal single is available to be tape 500 for higher rate tages and all for additional tate toge "Dividend allowance of C2000 2000 2019/20 The res apply in England Wales and No Sortih IT E-12085-19%, 120-1266-20% 1259-09-21% 01-1150,000-41% over 15000- Personal income tax allowances Motorcycles Bicycles Noosavings Sing Individual Savings Account (ISA) Junior ISA Lifetime ISA 20% Approved mileage rates Business Miles 0-10,000 10,000 Venture capital trust (VCT) Social investment tax relief (STR) Pension scheme allowances Annual allowance Lifetime allowance 2020/21 2019/20 f 12,500 100,000 Child Truit Funl Enterprise investment scheme (EIS) Seed Enterprise investment scheme (SEIS) 1,000 500 2,500 Income tax reliefs and incentives: annual limits 2020/21 20% 40% 0%" 12,500 100,000 20,000 9,000 4.000 9,000 2,000,000 100,000 200,000 1,000,000 Allowance rate per mde 45p 25p 24p 20p 40,000 1,073,100 1,250 29,600 2,000 1,000 500 2450 Dividends 0%" 7.5%** 32.5% 38.1% Increase ०००००००० 600 2019/20 50 f 20,000 4,368 4,000 4,368 2,000,000 100,000 200,000 1,000,000 40,000 1,055,000 Excess payments over these rates are taxable. Shortfall can be claimed as tax relief by the employee. If the employee carries another employee in their own car or van on a business journey, and additional rasfree psement of 5p per mile applies. Car and fuel benefits in kind (round reported CO, g/km down to find the corect percentage) Company car benefit charge (registered before 6 April 2020-NEDC-nuolybrid Co CO; Table e/km Petrol Diesel km Petrol Died 0 1 51 $2883: 55 16 60 17 18 20 80 21 CO₂ /km 0 1 $1 55 75 80 CO km 0 14 15 0 1 to 50 1 to 50 to 50 19 1 1 to 50 150 Isem 12 13 14 18 19 20 21 22 23 24 25 15 16 16 17 85 90 95 100 105 110 115 120 125 130+ 70129 40 to 69 30 to 30 30 95 18 100 19 105 20 110 21 115 18 22 120 19 23 125 CO₂ Taxable% km Penol Died 26 130 23 27 135 24 28 140 Reg 6/4/20 HAAAABAAR 0 2 5 8 12 14 22 25 26 Company car benefit change (registered after 6 Aprill 2020-WLTP-non-hybri Taxable% 00 Truble Fetsol Diesel km Petrol Diod g/km 0 130 135 30 140 31 145 150 55 20 90 (all earnings over £169) 27 28 29 30 S8825855 21 22 24 27 National Insurance Contributions ABARRERAS 30 31 155 32 160- 33 29 145 34 150 34 24 25 26 28 29 30 31 32 Company car benefit charge (hybrid cars with CO, <50g/km-otherwise use abiel Reg Electric only mileage range 6/4/20 O O 3 6 10 12 Class 1 Lower Earnings Limit-LEL (per week Primary (employees) Threshold (per week) Secondary employers) Threshold (per week) Upper Earnings Limit - UEL (per week-employees only) Upper Secondary Threshold (per week-21yr old) (per week-<25yr old apprentices) Employment allowance (per employer) Employee's contributions (183pw to £962pw 2% over £962) Employer's Contribution Rates Class 1A and 18 Class 2: Selemployed Contribution (per week) Small Profits Threshold (per annum) Class 3. Contribution (per week) (voluntary) Clan 4 Contributions - Upper Profits Limit Contributions-Lower Profi Limit Contribution Rate £120 £183 £160 £962 31 37 1962 1962 £4,000 SEGIHAN 2020/21 33 13.8% 00₂ Tiable % 13.8% £3.05 £6,475 35 36 32 (£9,500-£50,000pa then 2% over £50,000pal BARRERR 35 36 33 155 34 160 35 165 36 37 170- 37 37 £15.30 £50,000 £9,500 9.0% 37 Fed Dil 29 33 37 37 37 34 35 36 Note-no Diesel upplement applies if car meets Euro standard 6d Car fuel benefit change Van benefit charge Zero emosies van benefit charge Flat rate Van fuel benefit change 2019/20 £118 £166 £166 £962 1962 £962 £3,000 12% 13.8% 13.8% £3.00 £6,365 £15.00 £50,000 18,632 9.0% £24.500 £3,490 £2,792 £666 Capital taxes: Individuals Capital gains tax annual exempe amount Individual, etc. Capital gains tax standard basic rate Capital gains tax standard higher rate Business Asset Disposal Entrepreneurs' Relief limit Business Asset Disposal/ Entrepreneurs' Relief te Investor Relief limit Investon' Relief rate Inhentance tax threshold (each if couple/partner) Residence nil rate band limit Capital allowances 2020/21 2019/20 Plant and machinery: Main rate Special rate Inheritance tax rate Lower rate (10% of estane left to charity) Stamp Duty/Stamp Duty Reserve Tax 12,300 10% 20%* 20% I million 10 million 10% 10% 10 million 10 million 10% 10% 325,000 325,000 175,000 40% 36% Apprenticeship Levy 0.5% 12.000 applies in respect of residential properties and carried in *An 8% "Duy puble on share ponchuse over 1000 only and rounded up to 15 Corporation tax, allowances and reliefs Corporation Tax rate R&D tax credits SME scheme R&D SME repayable credit R&D Expenditure credit Patentbox Film, High end TV and videogame tax relief Diverted Profits Tas 0.9% 150,000 25,000 40% 36% Annual investment allowance Enhanced capital allowances Structures and Buildings Allowance *applies to investments made 1.1.19s 31.12.20 then of 200,000 will appl 2020/21 19% 230% 14.5% 13% 10% 25% 25% 2% Digital Service Tax Bank Surcharge 8% Bank levy: 1.1.20- 31.12.20-equity and LT lis 0.07% ST lab 0.14% Increase 5/% 300 0 0 2019/20 2020/21 18% 18% 6% 6% £1,000,000 £1,000,000 0% 3% Apprenticeship Levy Allowance (per employer) £15,000 Apprenticeship Levy rate (gross employee earnings) 0.5% -9 million 0000 100% 2% 2019/20 0 0 0 8% 0.075% 0.15% 2019/20 19% 230% 14.9% 12% 10% 25% 25% 2018/19 £15,000 0.5% Corporation tax on chargeable gains: indexation allowance Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec 1982 1983 82.61 82.97 1984 86.84 87.20 79.44 81.04 81.62 8185 81.90 81.90 8185 8226 8266 82.51 83.12 84.25 84.64 84.34 85.30 85.68 86.06 86.36 86.67 86.89 87.48 88.64 88.97 89.20 89.10 89.94 90.11 90.67 9095 90.87 1985 91.20 91.94 92.80 94.78 95.21 9541 95.23 95.49 95.44 95.59 95.92 96.05 1986 96.25 96.60 96.73 97.67 97.85 97.79 97.52 97.82 98.30 98.45 99.29 99.62 1987 100.0 1004 1006 1015 1019 101.9 101 102.1 1024 102.9 103.4 103.3 1988 1033 103.7 104.1 105.5 106.2 106.6 106.7 107.9 108.4 1095 1100 1103 1999 1110 1118 1123 1143 1150 1154 1155 1158 1166 1175 1185 118.8 1990 119.5 1202 1214 1251 126.2 1267 126.8 128.1 129.3 130.3 130.0 129.9 1991 130.2 1309 1314 1331 1335 1341 1338 1341 1346 1351 135.6 135.7 1992 135.6 136.3 136.7 138.5 139.3 139.3 1388 1389 1394 1399 139.7 139.2 1991 137.9 1388 139.3 1406 141.1 141.0 140.7 1413 1419 1418 1416 1419 1994 1413 142.1 142.5 1442 1447 1447 1440 144.7 1450 145.2 1453 146.0 1995 1460 1469 1475 1490 1496 1498 149.1 1499 1506 1498 1498 150.7 1996 1502 1509 1515 1526 1529 1530 1524 1531 1538 1538 1539 154.4 1997 1544 1550 1554 1563 1569 1575 1575 158.5 1993 1995 1596 160.0 1998 199.5 1601 1608 1626 1635 1634 163.0 163.7 164.4 164.5 164.4 164.4 1999 1634 1637 164.1 1652 1655 1656 1651 1655 1662 1665 1667 167.3 2000 166.6 1675 1684 1701 1707 1711 1705 1705 171.7 1716 1721 1722 2001 171.1 1720 172.2 1751 1742 1744 1733 1740 1746 1743 1736 1734 2002 1733 1738 1745 1757 1762 1762 1759 1764 1776 1779 1782 178.5 2003 1784 1793 1799 1812 1815 1813 1813 1816 1825 1826 1827 1835 2004 1831 1838 1846 1857 1865 1868 1568 1874 1881 2005 188.9 1896 1905 1916 1920 1921 1922 1926 1931 2006 1934 1942 1950 1965 197.7 1985 1985 199.2 2001 2007 2016 2031 2044 2054 2062 2073 2061 2073 2080 2089 209.7 210.9 2008 209.8 2114 2121 2140 215.1 2168 2165 2172 2184 2177 2160 2129 2009 2101 2114 2113 2115 2128 2134 2134 214.4 2153 2160 2166 218.0 2010 217.9 2192 220.7 1225 2236 2241 2236 224.5 2253 2258 2268 228.4 2011 2290 2313 232.5 2344 2352 2352 2347 2361 2379 2380 2385 2394 2012 2380 2999 240.8 2425 2424 2418 242.1 2430 244.2 2456 2456 246.8 2013 2458 2476 248.7 2495 250.0 249.7 249.7 2510 2519 2519 2521 2534 2014 252.6 2542 254.8 255.7 2559 2563 2560 257.0 257.6 257.7 2574 257.5 2015 2554 2567 257.1 258.0 2585 2589 2586 2598 2596 259.5 2598 260.6 2016 2588 2600 261.1 2614 262.1 2631 2634 2644 2649 2648 265.5 267.1 2017 265.5 2684 269.3 2706 271.7 272.3 2729 274.7 275.1 275.3 275.8 278.1 1886 1590 159.9 1933 1936 194.1 2004 2011 202.7 VAT Standard Rate Reduced Rate Annual Registration Limit Deregistration Limit VAT Fraction-standard rate Maximum tumover to join Cash Accounting Scheme Annual Accounting Scheme Flat Rate Scheme (ex VAT) Stamp Duty Land Tax Value of property ( Rendential property 0 -125,000 after 1 April 2020 after 1 April 2019 20% 3% €85.000 £83,000 1/6 125,001-250,000 250,001-925,000 925,001-1.5m remainder (over £1.5m) 20% 5% £85,000 £83,000 1/6 £1,350,000 £1,350,000 £150,000 £1,350,000 £1,350,000 £150,000 Stamp duty rate (%) 2" Sº 10" Retail prices index January 1987-100.00 New-nofher indexation ance will apply for depends ar 1 Jan 2018-the Dec 2017 te should be used for all subsequent sales 3% plemene on additional desling punch From 22.11.17 full SDLT wlff 1p >500.000 Value of property ( Nam idential property up to 150,000 150,001-250,000 over 250,000 20,000,000 Annual Tax on Enveloped Dwellings Value of property ( 500.000-1.000.000 1,000,001-2,000,000 2,000,001-5,000,000 5,000,001-10,000,000 10,000,001-20,000,000 Residential property 0 -145,000 0 145,001-250,000 250,001-325,000 325,001-750,000 Over 750,000 Scottish Land and Buildings Transactions Tax Value of property (0) LBTT rate %025 Jan 19 Nonresidencial property on or after 25 Jan 19: - 150,000 150,001-250,000 over 250,000 4% supplement on additional dwelleng panded over 140,000 LETT relief S1 came punches up to £175,000 Environmental taxes 40,000 pundup C00,000 and 9% up to £500,000. Nellable Stamp duty rate (6) Electricity Natural Gas LPG - - - 1 ATED charge (O 3,700 7,500 25,200 10° 12" Angregates levy (per tonne) Climate Change Levy (main rates Standard rate (per tonne) Lower rate (inactive waste per tunnel 58,850 118,050 236,250 Welsh Land Transaction Tax LTT rate% Value of property (0) Residential property** 0 -180,000 180,001-250,000 250,001-400,000 400,001-750,000 750,001-1,500,000 Over 1,500,000 Nimnidential property 0 - 150,000 150,001 - 250,000 250001-1,000,000 1,000,000 2020/21 (2019/20 £94.15 (291.35) £5.00 (£2.90) £2.00 (200) 9% supplement on additional dwelling purchased over £40,000. LETT forme purchases up to £175.000 0811p/kwh 0.406p/kwh 2.175p/kg 0* 3.5° 5° Insurance Premium Tax: Standard Rate Higher Rate (travel, appliances, some vehicles) 20% 7.5 10⁰ 12⁰ 9150 6 Air Passenger Duty: Rand A10-2000 miles) B2000) HMRC interest rates Duty rates Cigan Hand rolling tobacco Wine >22% alw 15%-22% 5.9%-15% 4%-5.5% al 12%-4% a Sparkling wine 5.5%-85% av 8.5%-15% Cider Perry Sol 1.2% 6.9% aby 6.9%-7.5% av 7.5%-85% av All cars since 7/04/20 All taxes (ince 21/08/18) Average Official rate for 2020/21 2.29% (These rate change occally-see the HMRC webne for deta Sparkling 12%-5,5% av 5.5%-85% Spirits Redwol ta Dury Beer 19.08/e pint 8.42p for low strength or an cars 5.69p for high strength apply E13 080 16.9% price+237.34 per thousand 1296.04/3g (23333/ 12.8810/ £3.8115/ 4038/ 50.71p/le £25.74/ £28.74/lit pure alcohol £3.9672/ 75cl bon 12.9757/ EL.2608/ 40.35p/litre £2581/ LPG Other Natural girl full Fuel Ol Aviation puoline Lane Pement 26 3.25 Fuel Duties Unleaded/Heavy oil (Diesel/Biodiesel & bioethanol Biodiesel for non-road use $7.95/ 11.14p/le 31.6l/kg 24.7p/k 10.7p/li 37.7p/le Typical hem parker of 20 packet of 5 30e Regument 2 05 0.5 751 ble 75db Sondad 70 bole £26 1176 Higher 175 £528

Expert Answer:

Answer rating: 100% (QA)

Land pruchased on 01012020 for Singed Contract on 010420... View the full answer

Related Book For

Andersons Business Law and the Legal Environment

ISBN: 978-0324786668

21st Edition

Authors: David p. twomey, Marianne moody Jennings

Posted Date:

Students also viewed these accounting questions

-

Hobart Ltd commenced its operation on 1 January 2020 and the financial statements are as follows: Hobart Ltd Balance Sheet (31 December 2020) Current Assets Cash Accounts Receivable Inventory...

-

In 2015, Chin Corp. purchased a piece of land for $2,500,000. In 2018, the land was sold for $3,500,000. Required: Prepare the journal entry to record the sale of Chin Corp's land.

-

A company bought a machine on 1 January 2020 for RM170,000. It is expected to last for 10 years and then be sold for scrap for RM10,000. Usage over the next 10 years is expected to be: Year...

-

Determine the range of the 2x function y = 3 sec 3

-

The following data (all in billion $) are the sales and costs (excluding selling and general and administrative costs) of McDonalds for company-operated restaurants (i.e., excluding franchise...

-

What is the consolidated total of non-controlling interest appearing on the balance sheet? a. $85,500. b. $83,100. c. $87,000. d. $70,500. Use the following data for problem On January 1, Jarel...

-

Using only the factor formulas given in Table 2.6, derive Equation 7.5 starting with Equation 7.3. TABLE 2.6 Summary of Discrete Compounding Interest Factors. To Find Given Factor Symbol Name P F...

-

Recognition of Profit on Long-Term Contracts During 2010 Nilsen Company started a construction job with a contract price of $1,600,000. The job was completed in 2012. The following information is...

-

Unusual shapes! At this point, we've gotten pretty comfortable with calculating the perimeter and area of squares and rectangles. In this assignment, we'll make a program that calculates these values...

-

There is an array A made of N integers. Your task is to choose as many integers from A as possible so that, when they are put in ascending order, all of the differences between all pairs of...

-

T is time to look at the thoughts of the ACDBN board of directors as they relate to religion in immigrant life. Start this discussion by watching the "faithful transitions: religion in immigrant...

-

Given the below data and assumptions: What is the ending Net Fixed Asset balance for 2021? Please follow the BASE method to complete your calculation. Note: Please provide your answer to the nearest...

-

A police car traveling at 95.0 km/h is traveling west, chasing a motorist traveling at 80.0 km/h. If they are originally 250 m apart, in what time interval will the police car overtake the motorist?

-

A parallel plate capacitor whose capacitance is 13.5 pF is charged by a battery to a potential difference V= 12.5 V between its plates. The battery is disconnected, and a porcelain slab (k= 6.5) is...

-

Given the below data and assumptions: What is the Change in OWC for 2021? Note: Please provide your answer to the nearest integer with no comma or $ sign e.g. if the answer is $1,234,567, type in...

-

Let f be a given function; let the domain of f be A := (-, ) and let the range of f be B := (0, ). Assuming that f possesses an inverse f-, answer the below. (Note. The abbreviations "-infty",...

-

Software testingA small software company is working on anintegrated inventory control system for a very largenational shoe manufacturer. The system will gathersales information daily from shoe stores...

-

Find the velocity, acceleration, and speed of a particle with the given position function. r(t) = (t 2 , sin t - t cos t, cos t + t sin t), t > 0

-

The Department of Health and Human Services has proposed new guidelines for the interpretation of federal statutes on gifts, incentives, and other benefits bestowed on physicians by pharmaceutical...

-

Which of the following is not correct concerning computer software purchased by Gultch Company from Softtouch Company? Softtouch originally created this software. a. Gultch can make backup copies in...

-

On July 24, 2002, the Recording Industry Association of America (RIAA) served its first subpoena to obtain the identity of a Verizon subscriber alleged to have made more than 600 copyrighted songs...

-

Find the input-output differential equation relating \(v_{o}\) and \(v_{i}(t)\) for the circuit shown below. w R R Vo v(t) R L

-

Consider the following circuit where \(i_{i}(t)\) is the input current and \(i_{o}(t)\) is the output current. (a) Obtain the State-Variable Matrix model \((A, B, C, D)\) for the circuit. (b) Obtain...

-

(a) For the following circuit find the State-Variable Matrix model (A, B, C, D) where \(v_{o}\) is the output voltage and \(v_{i}\) is the input voltage. (b) Also, find the input-output differential...

Study smarter with the SolutionInn App