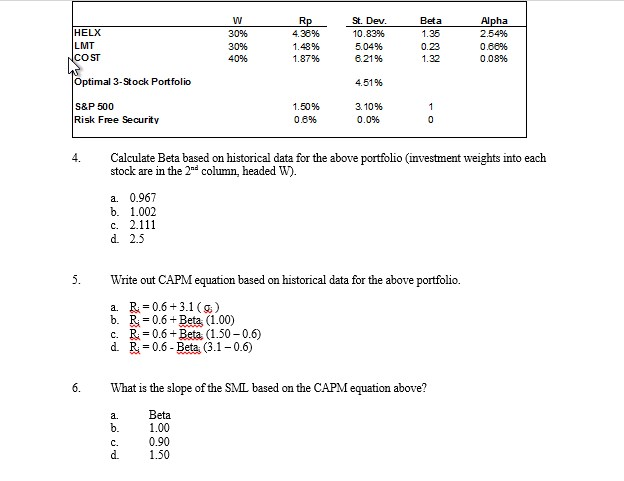

Question: Calculate Beta based on historical data for the above portfolio (investment weights into each stock are in the 2^nd column, headed WO. 0.967 1.002 2.111

Calculate Beta based on historical data for the above portfolio (investment weights into each stock are in the 2^nd column, headed WO. 0.967 1.002 2.111 2.5 Write out CAPM equation based on historical data for the above portfolio. R_i = 0.6 + 3.1 (sigma;) R_i = 0.6 + Beta; (1.00) R_i = 0.6 + Beta; (1.50 - 0.6) R_i = 0.6 - Beta; (3.1 - 0.6) What is the slope of the SML based on the CAPM equation above? Beta 1.00 0.90 1.50

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock