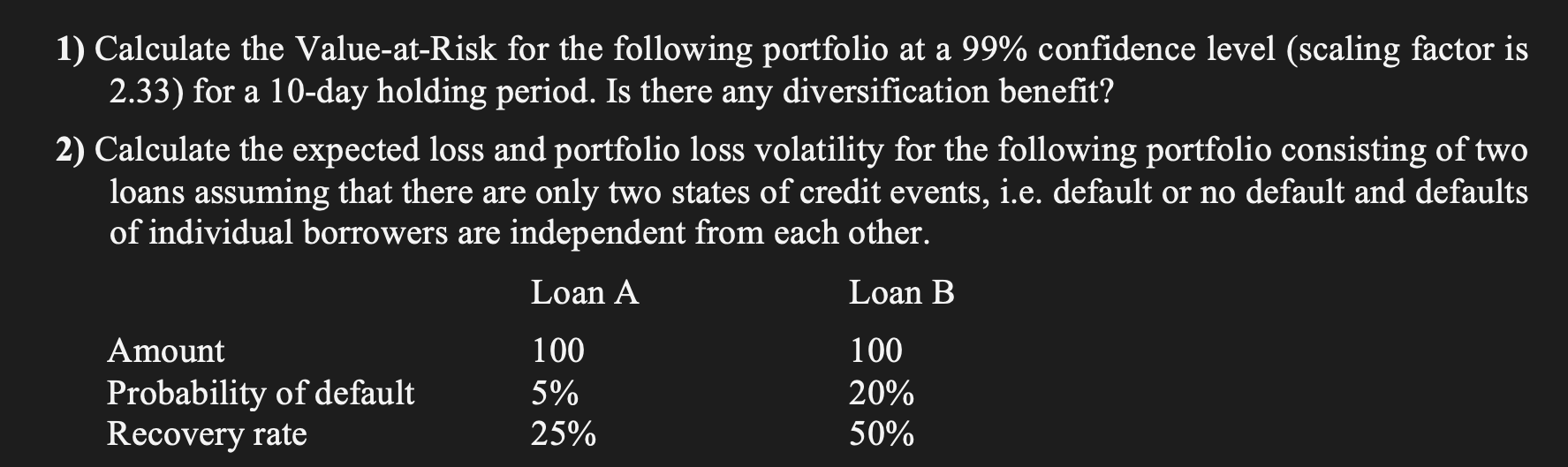

Question: Calculate the Value - at - Risk for the following portfolio at a 9 9 % confidence level ( scaling factor is 2 . 3

Calculate the ValueatRisk for the following portfolio at a confidence level scaling factor is

for a day holding period. Is there any diversification benefit?

Calculate the expected loss and portfolio loss volatility for the following portfolio consisting of two

loans assuming that there are only two states of credit events, ie default or no default and defaults

of individual borrowers are independent from each other.

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock