Question: Can anyone help me solve this problem? Cox Ross Rubinstein formula In the n-step binomial tree, the discounted risk-neutral expectation of the option payout is

Can anyone help me solve this problem?

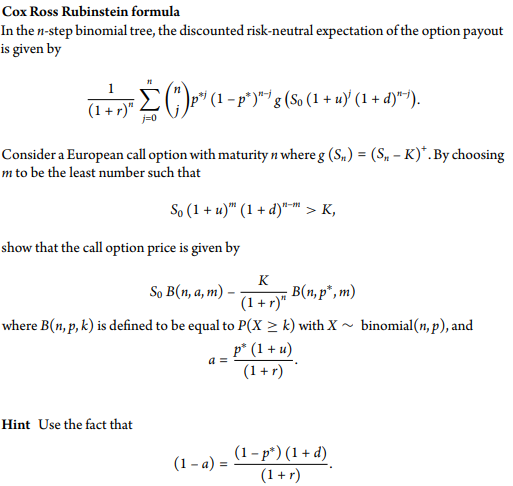

Cox Ross Rubinstein formula In the n-step binomial tree, the discounted risk-neutral expectation of the option payout is given by 11 (1 + (%)P (1 p*)*1g (So(1+u) (1 + a)""). =0 Consider a European call option with maturity n whereg (S.) = (S. - K). By choosing m to be the least number such that So (1 + u) (1 + d)*> K, show that the call option price is given by K S, B(n,a,m) (1+r)" B(n,p", m) where B(n, p,k) is defined to be equal to P(x > k) with X~ binomial(n, p), and P* (1 + 1) (1+r) a = Hint Use the fact that (1 - a) = (1 - p*)(1+d) (1+r) Cox Ross Rubinstein formula In the n-step binomial tree, the discounted risk-neutral expectation of the option payout is given by 11 (1 + (%)P (1 p*)*1g (So(1+u) (1 + a)""). =0 Consider a European call option with maturity n whereg (S.) = (S. - K). By choosing m to be the least number such that So (1 + u) (1 + d)*> K, show that the call option price is given by K S, B(n,a,m) (1+r)" B(n,p", m) where B(n, p,k) is defined to be equal to P(x > k) with X~ binomial(n, p), and P* (1 + 1) (1+r) a = Hint Use the fact that (1 - a) = (1 - p*)(1+d) (1+r)

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts