Question: Can someone help me solve and show your work for each step please:) this is all the information given Cox Ross Rubinstein formula In the

Can someone help me solve and show your work for each step please:)

this is all the information given

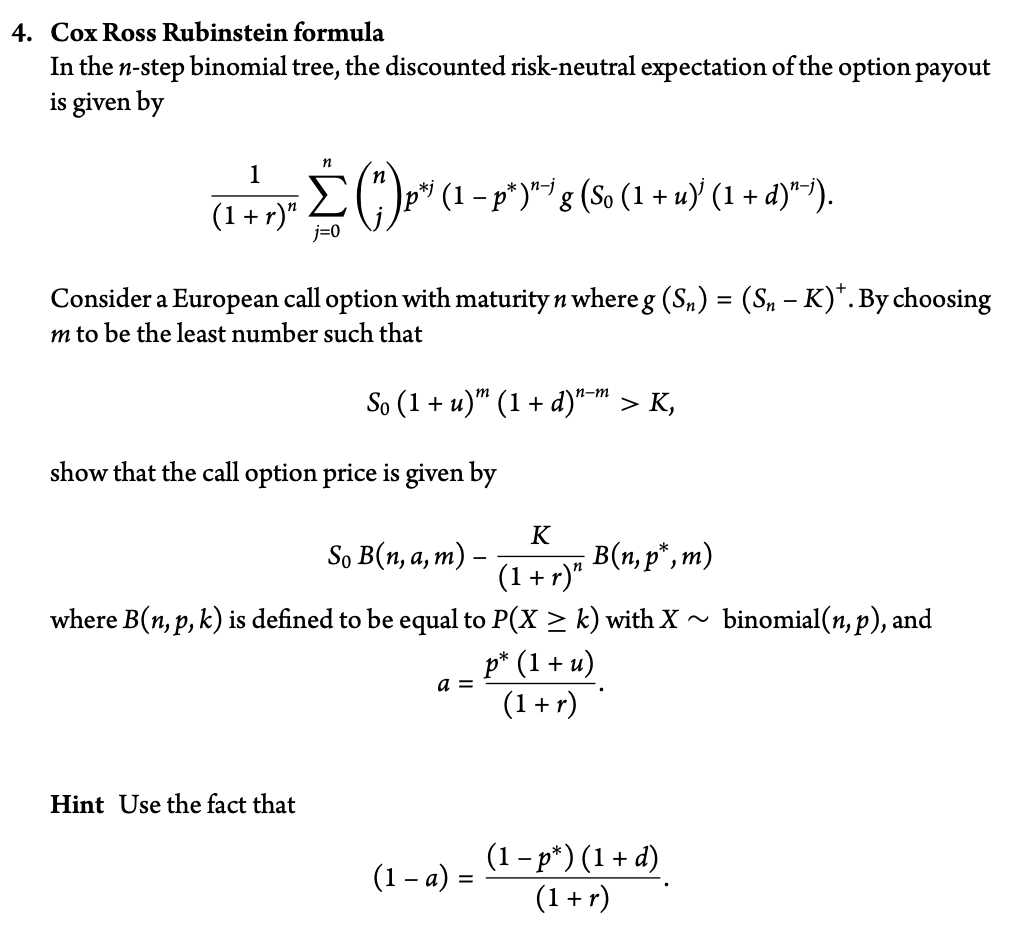

Cox Ross Rubinstein formula In the n-step binomial tree, the discounted risk-neutral expectation of the option payout is given by (1+r)n1j=0n(nj)pj(1p)njg(S0(1+u)j(1+d)nj) Consider a European call option with maturity n where g(Sn)=(SnK)+. By choosing m to be the least number such that S0(1+u)m(1+d)nm>K show that the call option price is given by S0B(n,a,m)(1+r)nKB(n,p,m) where B(n,p,k) is defined to be equal to P(Xk) with Xbinomial(n,p), and a=(1+r)p(1+u) Hint Use the fact that (1a)=(1+r)(1p)(1+d) Cox Ross Rubinstein formula In the n-step binomial tree, the discounted risk-neutral expectation of the option payout is given by (1+r)n1j=0n(nj)pj(1p)njg(S0(1+u)j(1+d)nj) Consider a European call option with maturity n where g(Sn)=(SnK)+. By choosing m to be the least number such that S0(1+u)m(1+d)nm>K show that the call option price is given by S0B(n,a,m)(1+r)nKB(n,p,m) where B(n,p,k) is defined to be equal to P(Xk) with Xbinomial(n,p), and a=(1+r)p(1+u) Hint Use the fact that (1a)=(1+r)(1p)(1+d)

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts