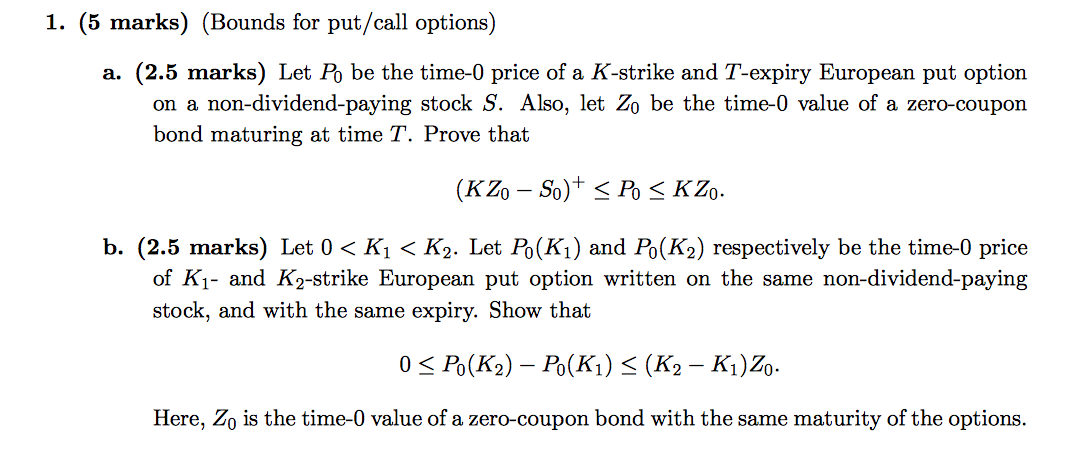

Question: Can anyone please help me to solve this question? Thanks. . (5 marks) (Bounds for put/call options) a. (2.5 marks) Let Po be the time0

Can anyone please help me to solve this question? Thanks.

. (5 marks) (Bounds for put/call options) a. (2.5 marks) Let Po be the time0 price of a K-strike and T-expiry European put option on a non-dividend-paying stock 3. Also, let Z0 be the time-0 value of a zero-coupon bond maturing at time T. Prove that (K20 So}+ 5 P0 5 K29. b. (2.5 marks) Let 0

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock