Question: can I get help doing E and F . in detail so I understand it. thank you Consolidation subsequent to date of acquisition - Equity

can I get help doing E and F . in detail so I understand it. thank you

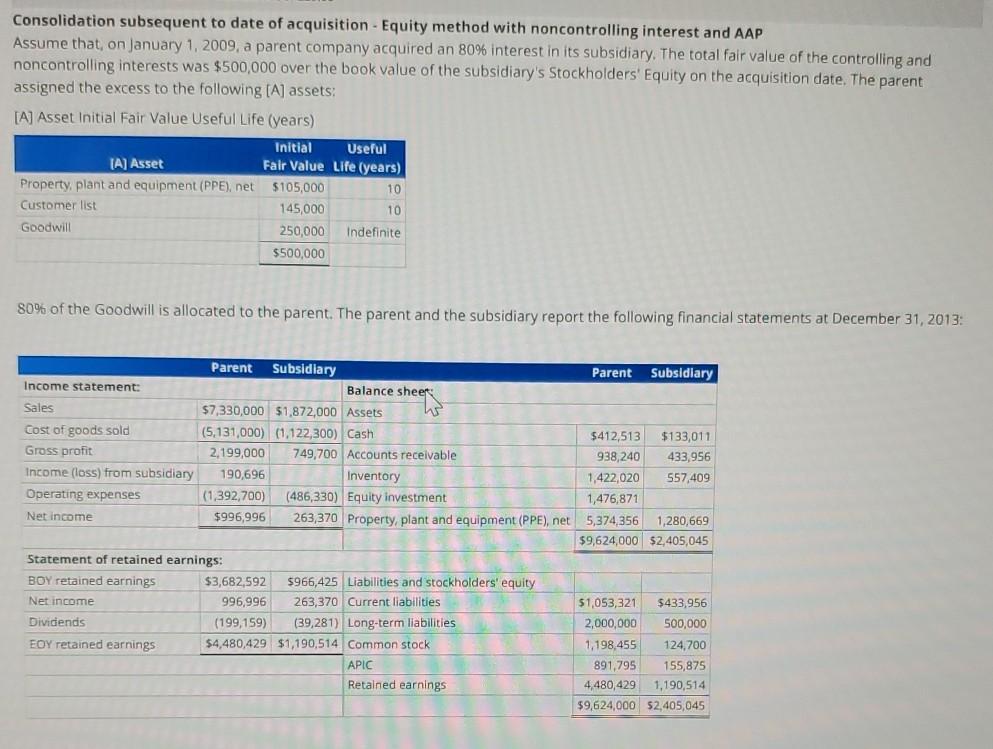

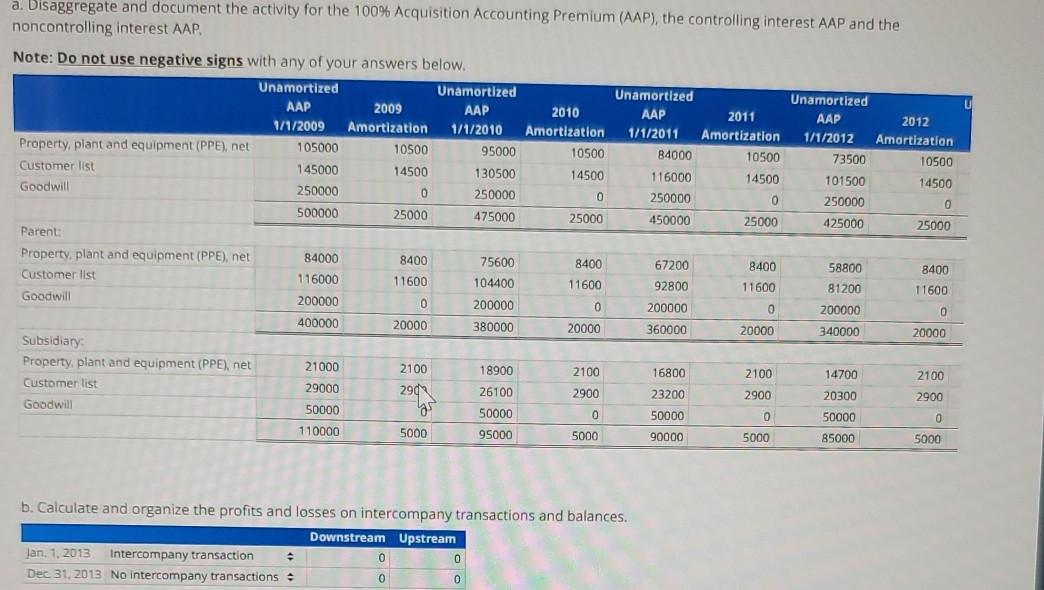

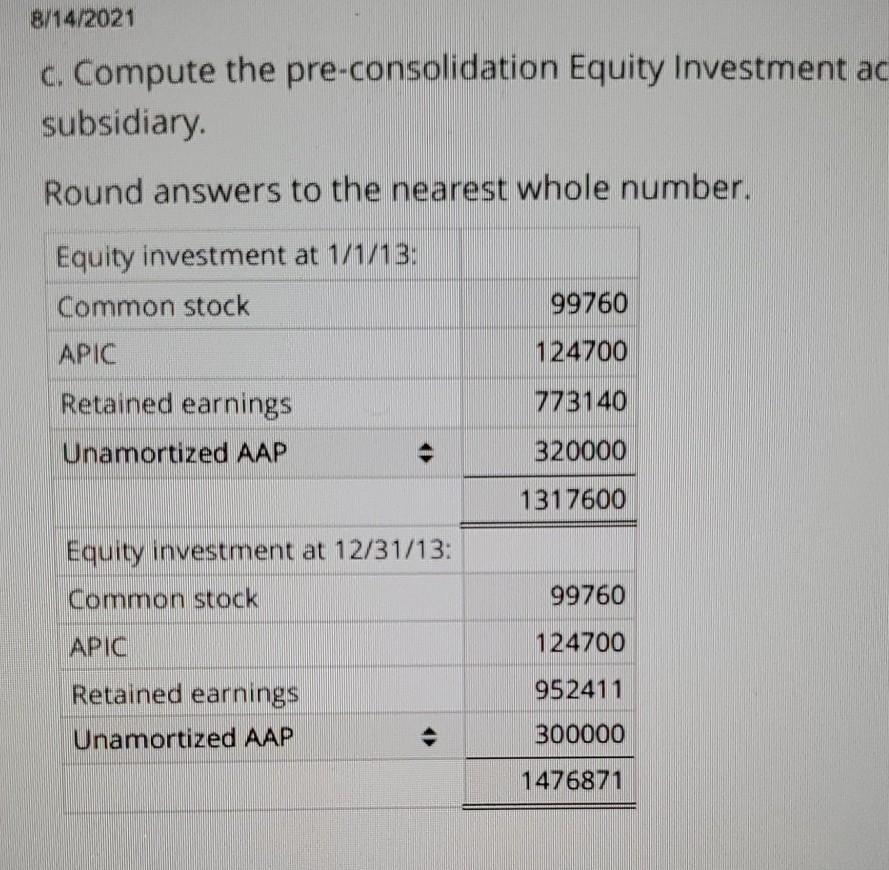

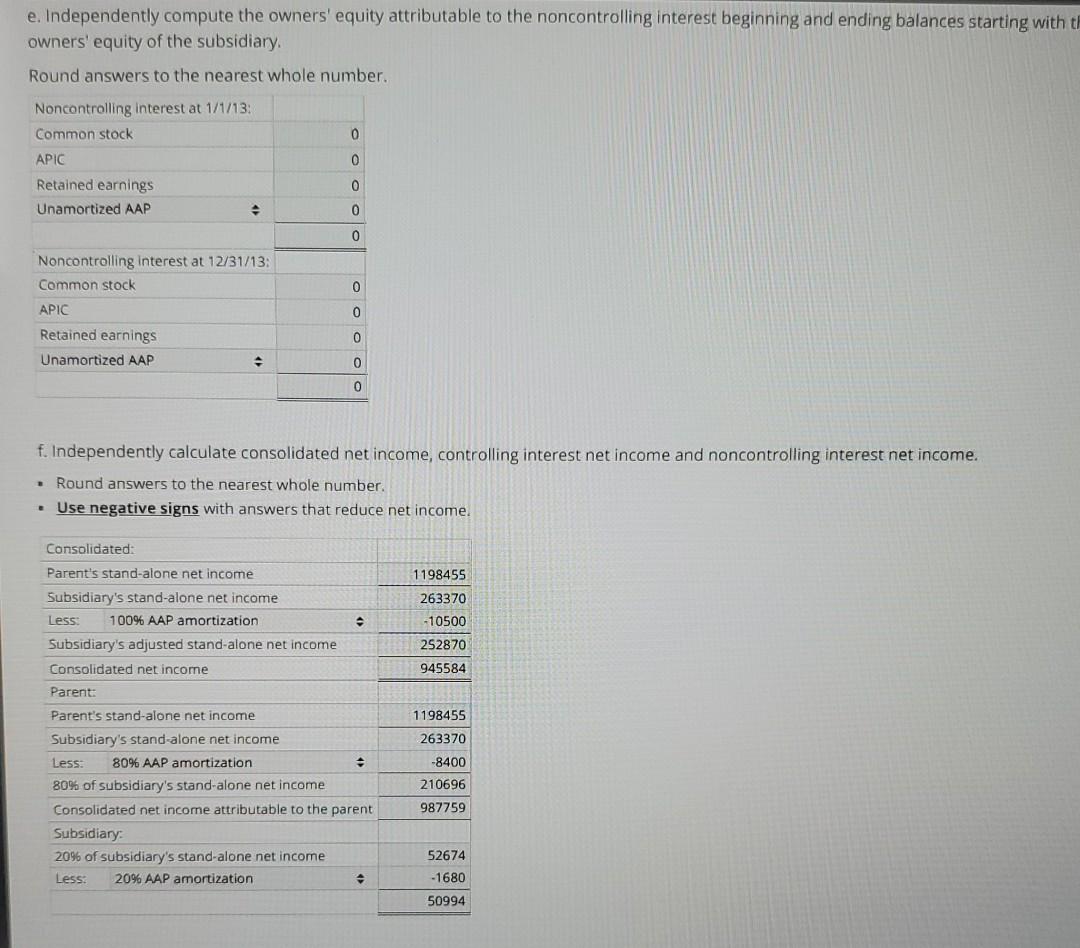

Consolidation subsequent to date of acquisition - Equity method with noncontrolling interest and AAP Assume that, on January 1, 2009, a parent company acquired an 80% interest in its subsidiary. The total fair value of the controlling and noncontrolling interests was $500,000 over the book value of the subsidiary's Stockholders' Equity on the acquisition date. The parent assigned the excess to the following [A] assets: [A] Asset Initial Fair Value Useful Life (years) Initial Useful IA) Asset Fair Value Life (years) Property, plant and equipment (PPE), net $105,000 10 Customer list 145,000 10 Goodwill 250,000 Indefinite $500,000 80% of the Goodwill is allocated to the parent. The parent and the subsidiary report the following financial statements at December 31, 2013: Parent Subsidiary Parent Subsidiary Income statement: Balance sheet Sales $7,330,000 $1,872,000 Assets ws Cost of goods sold (5,131,000) (1.122,300) Cash $412,513 $133,011 Gross profit 2,199,000 749,700 Accounts receivable 938,240 433,956 Income (loss) from subsidiary 190,696 Inventory 1,422,020 557,409 Operating expenses (1.392,700) (486,330) Equity investment 1,476,871 Net income $996,996 263,370 Property, plant and equipment (PPE), net 5,374,356 1,280,669 $9,624,000 $2,405,045 Statement of retained earnings: BOY retained earnings $3,682,592 5966,425 Liabilities and stockholders' equity Net income 996,996 263,370 Current liabilities $1,053,321 $433,956 Dividends (199,159) (39,281) Long-term liabilities 2,000,000 500,000 EOY retained earnings $4,480,429 $1,190,514 Common stock 1,198,455 124,700 APIC 891,795 155,875 Retained earnings 4,480,429 1,190,514 $9,624,000 $2,405,045 a. Disaggregate and document the activity for the 100% Acquisition Accounting Premium (AAP), the controlling interest AAP and the noncontrolling interest AAP. Note: Do not use negative signs with any of your answers below. Unamortized Unamortized Unamortized Unamortized 2009 2010 2011 AAP 2012 1/1/2009 Amortization 1/1/2010 Amortization 1/1/2011 Amortization 1/1/2012 Amortization Property, plant and equipment (PPE), net 105000 10500 95000 10500 84000 10500 73500 10500 Customer list 145000 14500 130500 14500 116000 14500 101500 14500 Goodwill 250000 0 250000 0 250000 0 250000 0 500000 25000 475000 25000 450000 25000 425000 25000 Parent Property, plant and equipment (PPE), net 84000 8400 75600 8400 67200 8400 58800 8400 Customer list 116000 11600 104400 11600 92800 11600 81200 11600 Goodwill 200000 0 200000 0 200000 0 200000 0 400000 20000 380000 20000 360000 20000 340000 20000 Subsidiary: Property, plant and equipment (PPE), net 21000 2100 18900 2100 16800 2100 14700 2100 Customer list 29000 26100 2900 23200 2900 20300 2900 Goodwill 50000 50000 0 50000 0 50000 0 110000 5000 95000 5000 90000 5000 85000 5000 2902 b. Calculate and organize the profits and losses on intercompany transactions and balances. Downstream Upstream Jan 1, 2013 Intercompany transaction 0 0 Dec 31, 2013 No intercompany transactions 0 0 0 B/14/2021 C. Compute the pre-consolidation Equity Investment ac subsidiary. Round answers to the nearest whole number. Equity investment at 1/1/13: Common stock 99760 APIC 124700 773140 Retained earnings Unamortized AAP 320000 1317600 Equity investment at 12/31/13: Common stock 99760 APIC 124700 952411 Retained earnings Unamortized AAP 300000 1476871 e. Independently compute the owners' equity attributable to the noncontrolling interest beginning and ending balances starting with owners' equity of the subsidiary. Round answers to the nearest whole number. 0 Noncontrolling interest at 1/1/13: Common stock APIC Retained earnings Unamortized AAP 0 0 0 0 0 Noncontrolling Interest at 12/31/13: Common stock APIC Retained earnings Unamortized AAP 0 0 0 0 f. Independently calculate consolidated net income, controlling interest net income and noncontrolling interest net income. Round answers to the nearest whole number. Use negative signs with answers that reduce net income. Less 1198455 263370 -10500 252870 945584 Consolidated: Parent's stand-alone net income Subsidiary's stand-alone net income 100% AAP amortization Subsidiary's adjusted stand-alone net income Consolidated net income Parent: Parent's stand-alone net income Subsidiary's stand-alone net income Less 80% AAP amortization . 80% of subsidiary's stand-alone net income Consolidated net income attributable to the parent Subsidiary: 20% of subsidiary's stand-alone net income Less: 20% AAP amortization 1198455 263370 -8400 210696 987759 52674 -1680 50994

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts