Question: Can I PLEASE get b and c solved step by step? Or whatever you can do please. I will RATE 5 STARS. U can use

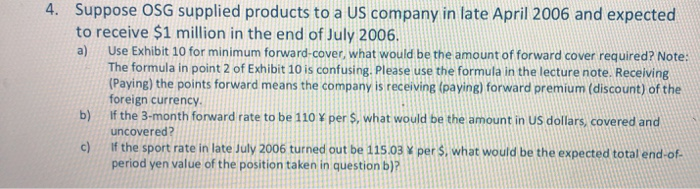

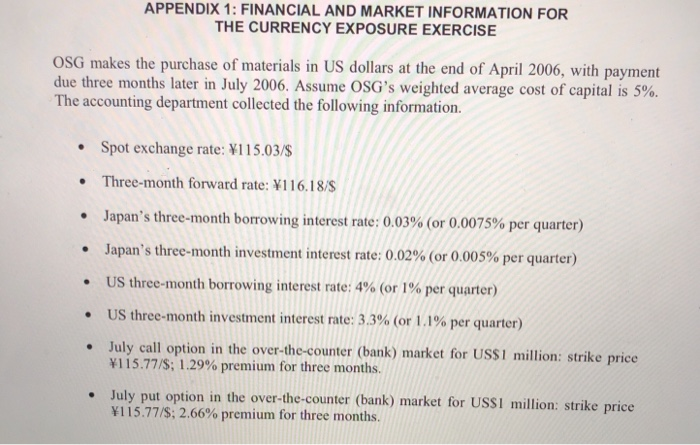

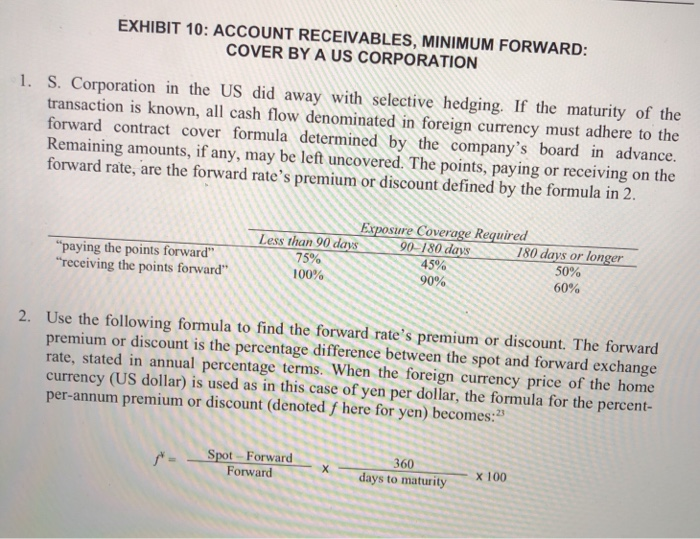

Suppose OSG supplied products to a US company in late April 2006 and expected to receive $1 million in the end of July 2006. 4. a) Use Exhibit 10 for minimum forward-cover, what would be the amount of forward cover required? Note: The formula in point 2 of Exhibit 10 is confusing. Please use the formula in the lecture note. Receiving (Paying) the points forward means the company is receiving (paying) forward premium (discount) of the foreign currency. If the 3-month forward rate to be 110 per $, what would be the amount in US dollars, covered and b) uncovered? If the sport rate in late July 2006 turned out be 115.03 Y per $, what would be the expected total end-of- c) period yen value of the position taken in question b)? APPENDIX 1: FINANCIAL AND MARKET INFORMATION FOR THE CURRENCY EXPOSURE EXERCISE OSG makes the purchase of materials in US dollars at the end of April 2006, with payment due three months later in July 2006. Assume OSG's weighted average cost of capital is 5%. The accounting department collected the following information. Spot exchange rate: 115.03/$ Three-month forward rate: 116.18/S Japan's three-month borrowing interest rate: 0.03% (or 0.0075% per quarter) Japan's three-month investment interest rate: 0.02% (or 0.005% per quarter) US three-month borrowing interest rate: 4% (or 1% per quarter) US three-month investment interest rate: 3.3% (or 1.1% per quarter) July call option in the over-the-counter (bank) market for US$1 million: strike price 115.77/$; 1.29% premium for three months. July put option in the over-the-counter (bank) market for USS1 million: strike price 115.77/S; 2.66% premium for three months. EXHIBIT 10: ACCOUNT RECEIVABLES, MINIMUM FORWARD: COVER BY A US CORPORATION 1. S. Corporation in the US did away with selective hedging. If the maturity of the transaction is known, all cash flow denominated in foreign currency must adhere to the forward contract cover formula determined by the company's board in advance. Remaining amounts, if any, may be left uncovered. The points, paying or receiving on the forward rate, are the forward rate's premium or discount defined by the formula in 2. Exposure Coverage Required 90-180 days 45% 180 days or longer 50% Less than 90 days 75% "paying the points forward" "receiving the points forward" 100% 90% 60% 2. Use the following formula to find the forward rate's premium or discount. The forward premium or discount is the percentage difference between the spot and forward exchange rate, stated in annual percentage terms. When the foreign currency price of the home currency (US dollar) is used as in this case of yen per dollar, the formula for the percent- per-annum premium or discount (denoted here for yen) becomes:" Spot Forward Forward 360 x 100 days to maturity Suppose OSG supplied products to a US company in late April 2006 and expected to receive $1 million in the end of July 2006. 4. a) Use Exhibit 10 for minimum forward-cover, what would be the amount of forward cover required? Note: The formula in point 2 of Exhibit 10 is confusing. Please use the formula in the lecture note. Receiving (Paying) the points forward means the company is receiving (paying) forward premium (discount) of the foreign currency. If the 3-month forward rate to be 110 per $, what would be the amount in US dollars, covered and b) uncovered? If the sport rate in late July 2006 turned out be 115.03 Y per $, what would be the expected total end-of- c) period yen value of the position taken in question b)? APPENDIX 1: FINANCIAL AND MARKET INFORMATION FOR THE CURRENCY EXPOSURE EXERCISE OSG makes the purchase of materials in US dollars at the end of April 2006, with payment due three months later in July 2006. Assume OSG's weighted average cost of capital is 5%. The accounting department collected the following information. Spot exchange rate: 115.03/$ Three-month forward rate: 116.18/S Japan's three-month borrowing interest rate: 0.03% (or 0.0075% per quarter) Japan's three-month investment interest rate: 0.02% (or 0.005% per quarter) US three-month borrowing interest rate: 4% (or 1% per quarter) US three-month investment interest rate: 3.3% (or 1.1% per quarter) July call option in the over-the-counter (bank) market for US$1 million: strike price 115.77/$; 1.29% premium for three months. July put option in the over-the-counter (bank) market for USS1 million: strike price 115.77/S; 2.66% premium for three months. EXHIBIT 10: ACCOUNT RECEIVABLES, MINIMUM FORWARD: COVER BY A US CORPORATION 1. S. Corporation in the US did away with selective hedging. If the maturity of the transaction is known, all cash flow denominated in foreign currency must adhere to the forward contract cover formula determined by the company's board in advance. Remaining amounts, if any, may be left uncovered. The points, paying or receiving on the forward rate, are the forward rate's premium or discount defined by the formula in 2. Exposure Coverage Required 90-180 days 45% 180 days or longer 50% Less than 90 days 75% "paying the points forward" "receiving the points forward" 100% 90% 60% 2. Use the following formula to find the forward rate's premium or discount. The forward premium or discount is the percentage difference between the spot and forward exchange rate, stated in annual percentage terms. When the foreign currency price of the home currency (US dollar) is used as in this case of yen per dollar, the formula for the percent- per-annum premium or discount (denoted here for yen) becomes:" Spot Forward Forward 360 x 100 days to maturity

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts