Question: Can someone help me solve this question and please show all work 1. Suppose that you have the return to a securities A and B

Can someone help me solve this question and please show all work

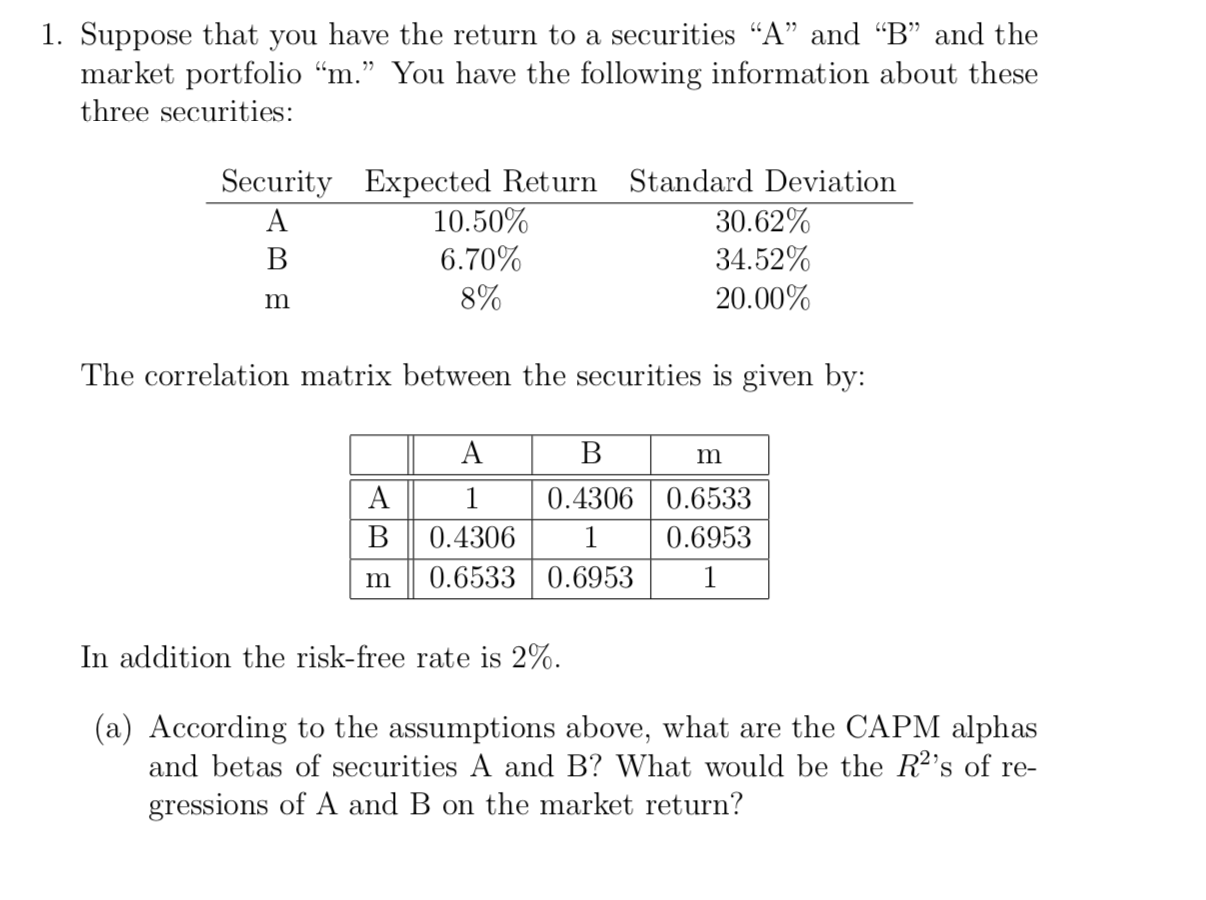

1. Suppose that you have the return to a securities A and B and the market portfolio m. You have the following information about these three securities: Security Expected Return Standard Deviation A 10.50% 30.62% B 6.70% 34.52% 8% 20.00% m The correlation matrix between the securities is given by: A B A B m 1 0.4306 0.6533 0.4306 1 0.6953 0.6533 0.6953 1 m In addition the risk-free rate is 2%. (a) According to the assumptions above, what are the CAPM alphas and betas of securities A and B? What would be the Ra's of re- gressions of A and B on the market return? 1. Suppose that you have the return to a securities A and B and the market portfolio m. You have the following information about these three securities: Security Expected Return Standard Deviation A 10.50% 30.62% B 6.70% 34.52% 8% 20.00% m The correlation matrix between the securities is given by: A B A B m 1 0.4306 0.6533 0.4306 1 0.6953 0.6533 0.6953 1 m In addition the risk-free rate is 2%. (a) According to the assumptions above, what are the CAPM alphas and betas of securities A and B? What would be the Ra's of re- gressions of A and B on the market return

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts