Question: Can you do just part e) and f) please. And show all your work, thank you [1.216] PN = 2.408 [0.4381 0.1751 0.1483 = 0.1751

Can you do just part e) and f) please. And show all your work, thank you

Can you do just part e) and f) please. And show all your work, thank you

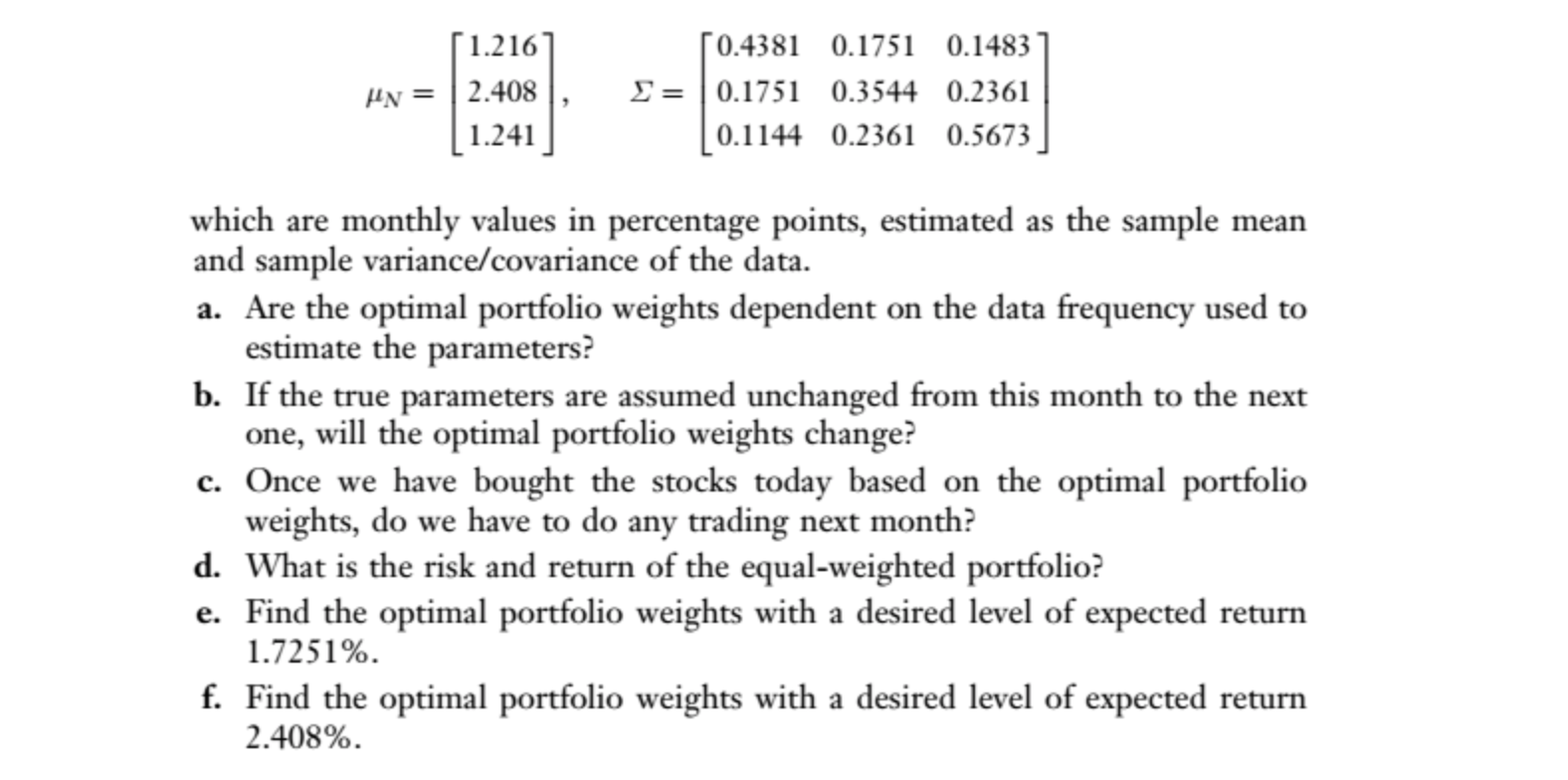

[1.216] PN = 2.408 [0.4381 0.1751 0.1483 = 0.1751 0.3544 0.2361 0.1144 0.2361 0.5673 1.241 which are monthly values in percentage points, estimated as the sample mean and sample variance/covariance of the data. a. Are the optimal portfolio weights dependent on the data frequency used to estimate the parameters? b. If the true parameters are assumed unchanged from this month to the next one, will the optimal portfolio weights change? c. Once we have bought the stocks today based on the optimal portfolio weights, do we have to do any trading next month? d. What is the risk and return of the equal-weighted portfolio? e. Find the optimal portfolio weights with a desired level of expected return 1.7251%. f. Find the optimal portfolio weights with a desired level of expected return 2.408%. [1.216] PN = 2.408 [0.4381 0.1751 0.1483 = 0.1751 0.3544 0.2361 0.1144 0.2361 0.5673 1.241 which are monthly values in percentage points, estimated as the sample mean and sample variance/covariance of the data. a. Are the optimal portfolio weights dependent on the data frequency used to estimate the parameters? b. If the true parameters are assumed unchanged from this month to the next one, will the optimal portfolio weights change? c. Once we have bought the stocks today based on the optimal portfolio weights, do we have to do any trading next month? d. What is the risk and return of the equal-weighted portfolio? e. Find the optimal portfolio weights with a desired level of expected return 1.7251%. f. Find the optimal portfolio weights with a desired level of expected return 2.408%

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts