Question: Can you help me further understand the answer key for each part of the question? I need a more beginner friendly explanation, in simplest terms

Can you help me further understand the answer key for each part of the question? I need a more beginner friendly explanation, in simplest terms possible. Thank you so much!

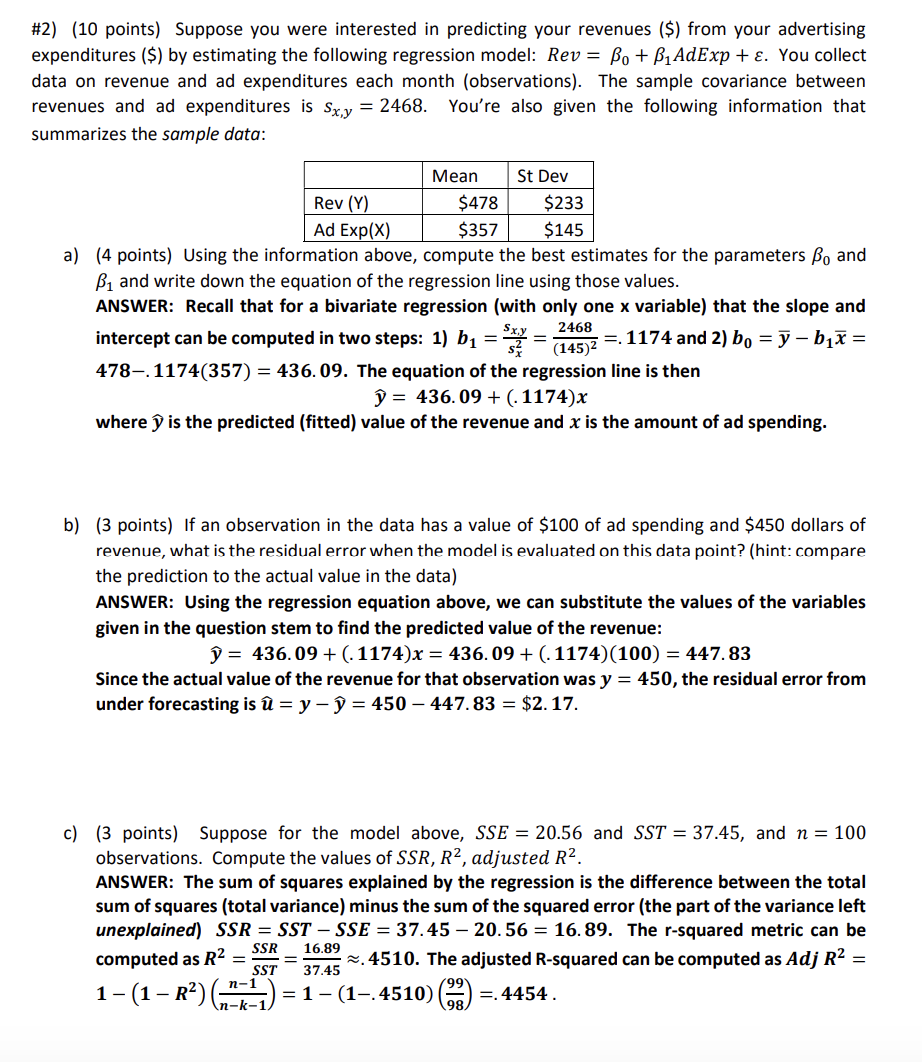

\#2) (10 points) Suppose you were interested in predicting your revenues (\$) from your advertising expenditures ( $ ) by estimating the following regression model: Rev=0+1AdExp+. You collect data on revenue and ad expenditures each month (observations). The sample covariance between revenues and ad expenditures is sx,y=2468. You're also given the following information that summarizes the sample data: a) (4 points) Using the information above, compute the best estimates for the parameters 0 and 1 and write down the equation of the regression line using those values. ANSWER: Recall that for a bivariate regression (with only one x variable) that the slope and intercept can be computed in two steps: 1) b1=sx2sx,y=(145)22468=.1174 and 2) b0=yb1x= 478.1174(357)=436.09. The equation of the regression line is then y=436.09+(.1174)x where y^ is the predicted (fitted) value of the revenue and x is the amount of ad spending. b) (3 points) If an observation in the data has a value of $100 of ad spending and $450 dollars of revenue, what is the residual error when the model is evaluated on this data point? (hint: compare the prediction to the actual value in the data) ANSWER: Using the regression equation above, we can substitute the values of the variables given in the question stem to find the predicted value of the revenue: y=436.09+(.1174)x=436.09+(.1174)(100)=447.83 Since the actual value of the revenue for that observation was y=450, the residual error from under forecasting is u=yy=450447.83=$2.17. c) (3 points) Suppose for the model above, SSE=20.56 and SST=37.45, and n=100 observations. Compute the values of SSR,R2, adjusted R2. ANSWER: The sum of squares explained by the regression is the difference between the total sum of squares (total variance) minus the sum of the squared error (the part of the variance left unexplained) SSR=SSTSSE=37.4520.56=16.89. The r-squared metric can be computed as R2=SSTSSR=37.4516.89.4510. The adjusted R-squared can be computed as Adj R2= 1(1R2)(nk1n1)=1(1.4510)(9899)=.4454

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts