Question: can you know how to do it please it is corporate finance u can do beta will cov over the protfolio of variance A portfolio

can you know how to do it please it is corporate finance

u can do beta will cov over the protfolio of variance

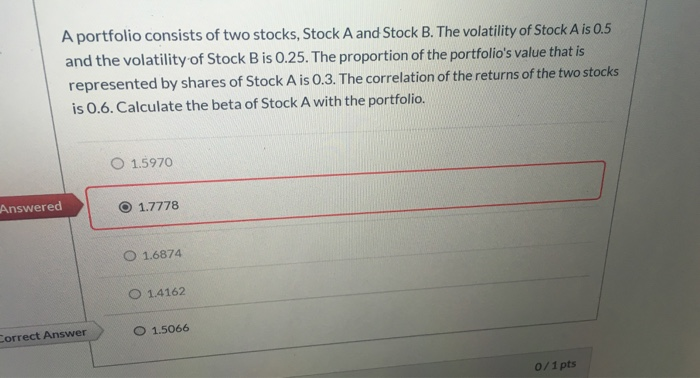

A portfolio consists of two stocks, Stock A and Stock B. The volatility of Stock A is 0.5 and the volatility of Stock B is 0.25. The proportion of the portfolio's value that is represented by shares of Stock A is 0.3. The correlation of the returns of the two stocks is 0.6. Calculate the beta of Stock A with the portfolio. O 1.5970 Answered O 1.7778 O 1.6874 O 1.4162 Correct Answer O 1.5066 0/1 pts

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock