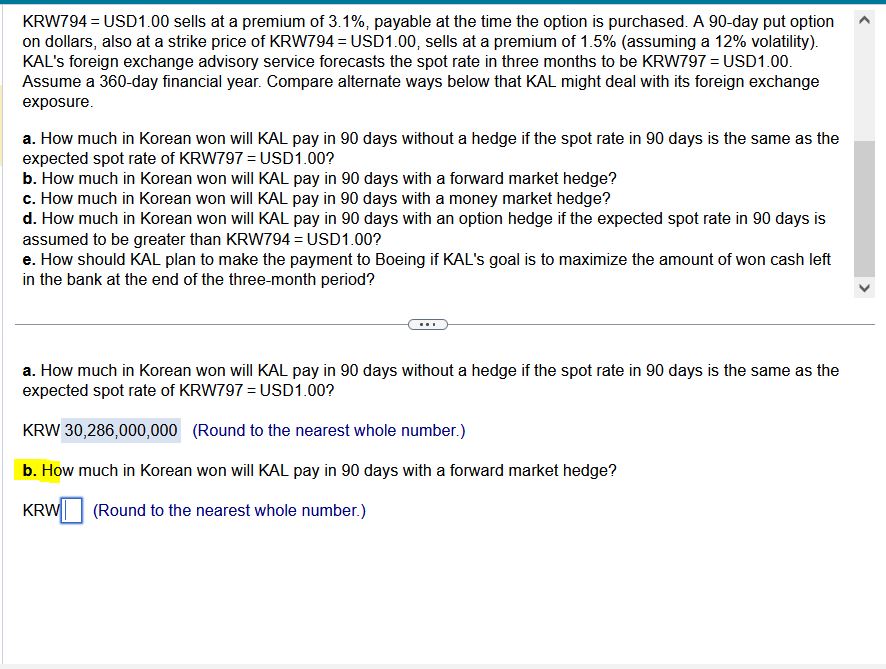

Question: Can you please help solve B. A is already correct. But I could use help on C,D,E as well. Thank you!! KRW794 = USD1.00 sells

Can you please help solve B. A is already correct. But I could use help on C,D,E as well. Thank you!!

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock