Question: Can you please help with just 2a? West Coast Semiconductor (WCS) was founded in Palo Alto, California, in 1984 by a team of engineers led

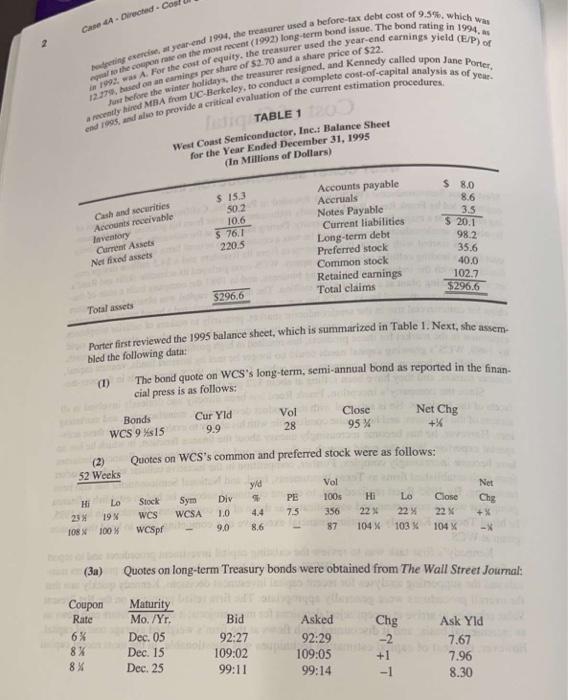

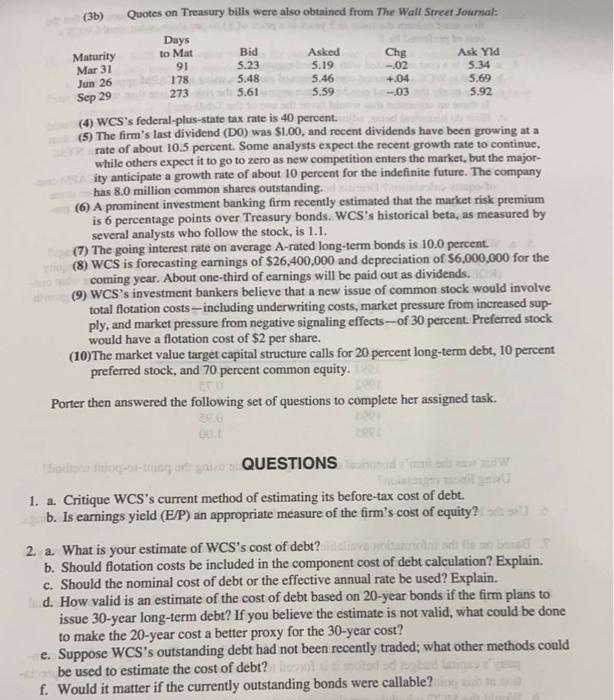

West Coast Semiconductor (WCS) was founded in Palo Alto, California, in 1984 by a team of engineers led by Frank Reed. Reed took early retirement that year from his position as an engineering professor at a major West Coast university. During his tenure at the university, Reed was actively involved in semiconductor research, and he was a consultant to several firms in the industry. WCS started with a $500.000 investment from its founders and a $4.5 million design contract from a leading cellular telephone company. WCS soon parlayed its scientific skills and Reed's familiarity with the industry into a thriving business, and in 1987 the company built a state-of-theart manufacturing plant at a cost of $100 million. The necessary capital was obtained from venture capitalists and commercial banks. WCS has since produced and marketed a broad range of computer chips for commercial use in the semiconductor market, primarily to makers of cellular telephones and laptop computers. Continued innovation in its memory and logic products, along with a rapid expansion in the market for these products, has resulted in high profitability and very rapid growth. By 1989. WCS's growing capital needs could no longer be met by internal funds, venture capital, and its ability to borrow, so the company went public. Currently, WCS shares trade in the over-thecounter market, and they have been selling at about $22 per share. Since the company's inception, Frank Reed has been directly and tirelessly involved in all facets of the business. He is satisfied with the product development, manufacturing, and marketing aspects of the business, and he is quite comfortable with his ability to evaluate and guide these activities. However, he has become increasingly uneasy about the finance function, in which he has no special expertise. With the rapid growth in the scope and size of the business, financial decisions have become increasingly complex. Further, competition in the lucrative cellular telephone market from such established firms as Texas Instruments, Intel, and National Semiconductor has also been increasing. By 1995 Reed realized that, to ensure continued success, he had to establish a finance group that was as competent and sophisticated as those of his competitors. Therefore, in late 1995, he hired Thomas Kennedy, a senior financial executive of a competing firm, to head the finance group at WCS. Kennedy's first task was to review the existing capital investment procedures and to report his findings and recommendations to WCS's board of directors. In going over the procedures manuals and the supporting analyses for recent capital investment decisions, Kennedy quickly saw that the overall procedures were generally appropriate: The firm relied primarily on the Net Present Value criterion to arrive at accept/reject decisions for most projects; it estimated future cash flows on an incremental basis; and it discounted cash flows at the firm's weighted average cost of capital. However, the cost of capital estimation techniques was questionable. In the most recent capital TABLE 1 Weat Coast Senticonductor, Inc.i Balance Sheet bled the following data: (1) The bond quote on WCS's long-term, semi-annual bond as reported in the finan-ial nmess is as follows: (2) Quotes on WCS's common and preferred stock were as follows: (3a) Quotes on long-term Treasury bonds were obtained from The Wall Street Journal: (3b) Quotes on Treasury bills were also obtained from The Wall Srreer Joumal: (4) WCS's federal-plus-state tax rate is 40 percent. (5) The firm's last dividend (D0) was $1.00, and recent dividends have been growing at a rate of about 10.5 percent. Some analysts expect the recent growth rate to continue. while others expect it to go to zero as new competition enters the market, but the majority anticipate a growth rate of about 10 percent for the indefinite future. The company has 8.0 million common shares outstanding. (6) A prominent investment banking firm recently estimated that the market risk premium is 6 percentage points over Treasury bonds. WCS's historical beta, as measured by several analysts who follow the stock, is 1.1. (7) The going interest rate on average A-rated long-term bonds is 10.0 percent. (8) WCS is forecasting earnings of $26,400,000 and depreciation of $6,000,000 for the coming year. About one-third of earnings will be paid out as dividends. (9) WCS's investment bankers believe that a new issue of common stock would involve total flotation costs - including underwriting costs, market pressure from increased supply, and market pressure from negative signaling effects - of 30 percent. Preferred stock would have a flotation cost of $2 per share. (10)The market value target capital structure calls for 20 percent long-term debt, 10 percent preferred stock, and 70 percent common equity. Porter then answered the following set of questions to complete her assigned task. QUESTIONS 1. a. Critique WCS's current method of estimating its before-tax cost of debt. b. Is earnings yield ( E/P) an appropriate measure of the firm's cost of equity? 2. a. What is your estimate of WCS's cost of debt? b. Should flotation costs be included in the component cost of debt calculation? Explain. c. Should the nominal cost of debt or the effective annual rate be used? Explain. d. How valid is an estimate of the cost of debt based on 20 -year bonds if the firm plans to issue 30-year long-term debt? If you believe the estimate is not valid, what could be done to make the 20 -year cost a better proxy for the 30 -year cost? e. Suppose WCS's outstanding debt had not been recently traded; what other methods could be used to estimate the cost of debt? f. Would it matter if the currently outstanding bonds were callable? West Coast Semiconductor (WCS) was founded in Palo Alto, California, in 1984 by a team of engineers led by Frank Reed. Reed took early retirement that year from his position as an engineering professor at a major West Coast university. During his tenure at the university, Reed was actively involved in semiconductor research, and he was a consultant to several firms in the industry. WCS started with a $500.000 investment from its founders and a $4.5 million design contract from a leading cellular telephone company. WCS soon parlayed its scientific skills and Reed's familiarity with the industry into a thriving business, and in 1987 the company built a state-of-theart manufacturing plant at a cost of $100 million. The necessary capital was obtained from venture capitalists and commercial banks. WCS has since produced and marketed a broad range of computer chips for commercial use in the semiconductor market, primarily to makers of cellular telephones and laptop computers. Continued innovation in its memory and logic products, along with a rapid expansion in the market for these products, has resulted in high profitability and very rapid growth. By 1989. WCS's growing capital needs could no longer be met by internal funds, venture capital, and its ability to borrow, so the company went public. Currently, WCS shares trade in the over-thecounter market, and they have been selling at about $22 per share. Since the company's inception, Frank Reed has been directly and tirelessly involved in all facets of the business. He is satisfied with the product development, manufacturing, and marketing aspects of the business, and he is quite comfortable with his ability to evaluate and guide these activities. However, he has become increasingly uneasy about the finance function, in which he has no special expertise. With the rapid growth in the scope and size of the business, financial decisions have become increasingly complex. Further, competition in the lucrative cellular telephone market from such established firms as Texas Instruments, Intel, and National Semiconductor has also been increasing. By 1995 Reed realized that, to ensure continued success, he had to establish a finance group that was as competent and sophisticated as those of his competitors. Therefore, in late 1995, he hired Thomas Kennedy, a senior financial executive of a competing firm, to head the finance group at WCS. Kennedy's first task was to review the existing capital investment procedures and to report his findings and recommendations to WCS's board of directors. In going over the procedures manuals and the supporting analyses for recent capital investment decisions, Kennedy quickly saw that the overall procedures were generally appropriate: The firm relied primarily on the Net Present Value criterion to arrive at accept/reject decisions for most projects; it estimated future cash flows on an incremental basis; and it discounted cash flows at the firm's weighted average cost of capital. However, the cost of capital estimation techniques was questionable. In the most recent capital TABLE 1 Weat Coast Senticonductor, Inc.i Balance Sheet bled the following data: (1) The bond quote on WCS's long-term, semi-annual bond as reported in the finan-ial nmess is as follows: (2) Quotes on WCS's common and preferred stock were as follows: (3a) Quotes on long-term Treasury bonds were obtained from The Wall Street Journal: (3b) Quotes on Treasury bills were also obtained from The Wall Srreer Joumal: (4) WCS's federal-plus-state tax rate is 40 percent. (5) The firm's last dividend (D0) was $1.00, and recent dividends have been growing at a rate of about 10.5 percent. Some analysts expect the recent growth rate to continue. while others expect it to go to zero as new competition enters the market, but the majority anticipate a growth rate of about 10 percent for the indefinite future. The company has 8.0 million common shares outstanding. (6) A prominent investment banking firm recently estimated that the market risk premium is 6 percentage points over Treasury bonds. WCS's historical beta, as measured by several analysts who follow the stock, is 1.1. (7) The going interest rate on average A-rated long-term bonds is 10.0 percent. (8) WCS is forecasting earnings of $26,400,000 and depreciation of $6,000,000 for the coming year. About one-third of earnings will be paid out as dividends. (9) WCS's investment bankers believe that a new issue of common stock would involve total flotation costs - including underwriting costs, market pressure from increased supply, and market pressure from negative signaling effects - of 30 percent. Preferred stock would have a flotation cost of $2 per share. (10)The market value target capital structure calls for 20 percent long-term debt, 10 percent preferred stock, and 70 percent common equity. Porter then answered the following set of questions to complete her assigned task. QUESTIONS 1. a. Critique WCS's current method of estimating its before-tax cost of debt. b. Is earnings yield ( E/P) an appropriate measure of the firm's cost of equity? 2. a. What is your estimate of WCS's cost of debt? b. Should flotation costs be included in the component cost of debt calculation? Explain. c. Should the nominal cost of debt or the effective annual rate be used? Explain. d. How valid is an estimate of the cost of debt based on 20 -year bonds if the firm plans to issue 30-year long-term debt? If you believe the estimate is not valid, what could be done to make the 20 -year cost a better proxy for the 30 -year cost? e. Suppose WCS's outstanding debt had not been recently traded; what other methods could be used to estimate the cost of debt? f. Would it matter if the currently outstanding bonds were callable

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts