Question: Can you please solve part C? Andreas Broszio (Geneva). Andreas Broszio just starled as an analyst for Credit Suisse in Geneva, Switzerland. He receives the

Can you please solve part C?

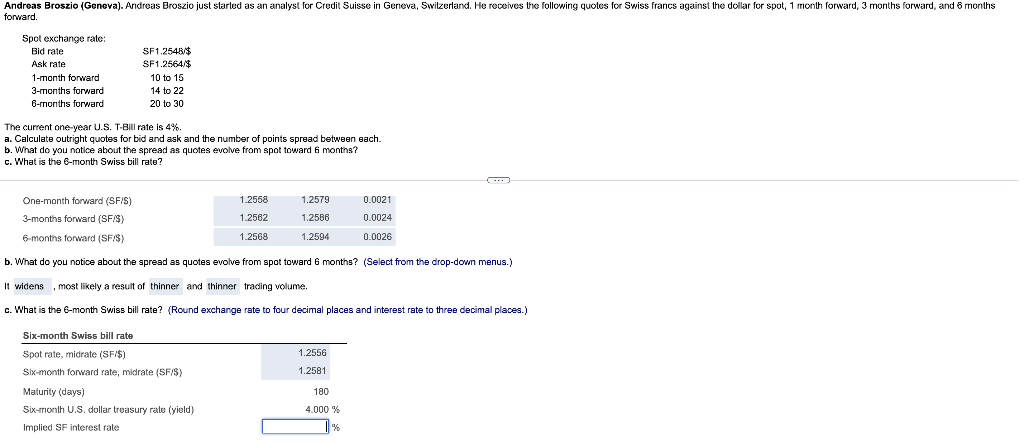

Andreas Broszio (Geneva). Andreas Broszio just starled as an analyst for Credit Suisse in Geneva, Switzerland. He receives the following quotes for Swiss francs against the dollar for spot, 1 month forward, 3 months forward, and 6 months forward. Spot exchange rate: : Bid rate SF1.2548/$ Ask rate SF1.2564/$ 1-month forward 10 to 15 3-months forward 14 to 22 6-months forward 20 to 30 The current one-year U.S. T-Bill rate is 4%. a. Calculate outright quotes for bid and ask and the number of points spread between each. b. What do you notice about the spread as quotes evolve from spot toward 6 months? c. What is the 6-month Swiss bill rate? 1.2558 1.2579 0.0021 One-month forward (SFIS) 3-months forward (SF/S) 1.2562 1.2586 0.0024 6-months forward (SF/S) 1.2568 1.2594 0.0026 b. What do you notice about the spread as quotes evolve from spot toward 6 months? (Select from the drop-down menus.) It widens , most likely a result of thinner and thinner trading volume. c. What is the 6-month Swiss bill rate? (Round exchange rate to four decimal places and interest rate to three decimal places.) Six-month Swiss bill rate 1.2556 Spot rate, midrate (SF/$) Six-month forward rate, midrate (SF/S) 1.2581 180 Maturity (days) Six-month U.S. dollar treasury rate (yield) Implied SF interest rate 4.000% %6

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts