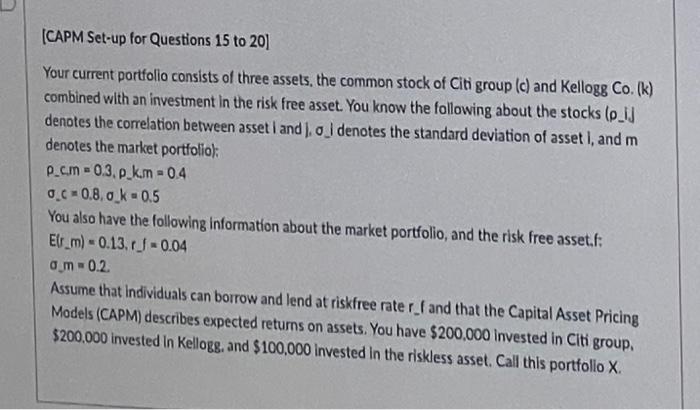

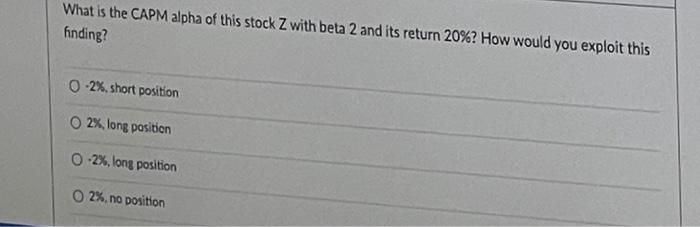

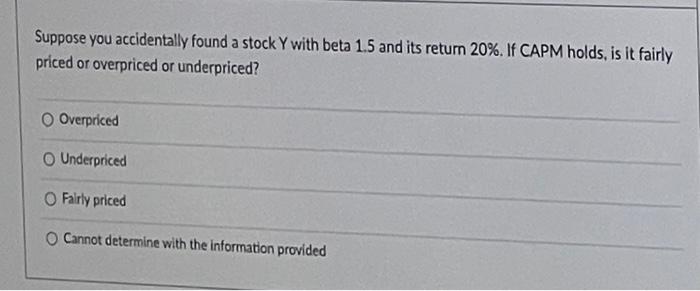

Question: (CAPM Set-up for Questions 15 to 20) Your current portfolio consists of three assets, the common stock of Citi group (c) and Kellogg Co. (k)

(CAPM Set-up for Questions 15 to 20) Your current portfolio consists of three assets, the common stock of Citi group (c) and Kellogg Co. (k) combined with an investment in the risk free asset. You know the following about the stocks (o_J denotes the correlation between asset i and ), o 1 denotes the standard deviation of asset I, and m denotes the market portfoliok p.cm = 0.3.p.k.m - 0.4 0.C 0.8.0_k - 0.5 You also have the following information about the market portfolio, and the risk free asset.f: Elr_m) -0.13.61 -0.04 om -0.2 Assume that Individuals can borrow and lend at riskfree rater fand that the Capital Asset Pricing Models (CAPM) describes expected returns on assets. You have $200,000 invested in Citigroup. $200,000 invested in Kellogs, and $100,000 invested in the riskless asset. Call this portfolio X What is the CAPM alpha of this stock Z with beta 2 and its return 20%? How would you exploit this finding? 02% short position 2x, long position 0 2%, long position O 2%.no position Suppose you accidentally found a stock Y with beta 1.5 and its return 20%. If CAPM holds, is it fairly priced or overpriced or underpriced? Overpriced Underpriced O Fairly priced Cannot determine with the information provided

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts