Question: Case Study 1 As we know, Implementation of enterprise resource planning systems is a complex technological and organizational business undertaking that requires the knowledge of

Case Study 1

As we know, Implementation of enterprise resource planning systems is a complex technological and organizational business undertaking that requires the knowledge of a process approach to overcome its implementation constraints (Epizitone & Olugbara, 2019). Thus, through ERP Systems traditional batches controls and audit trails are no longer available, modules have automated entries for each others, all transactions are integrated and stored in one common database, need of extensive and complex access security and authority matrix, need also complex network and database access security matrix and controls needed should be different from traditional systems. Several companies were already involved in some form of continuous auditing or control monitoring while others are attempting to adopt more advanced audit technologies especially after ERP implementation. They believed by applying a continuous audit, there are measurable differences in the risk of fraud and errors, and also it will improve ability to assess risks and needed controls upon these risks within ERP environment. According to the background, analyze from results of internal auditor inside of organization (sample total of 13 companies) using ERP systems and adopting continues audit and also without continue audit, presented in table 1 and table 2.

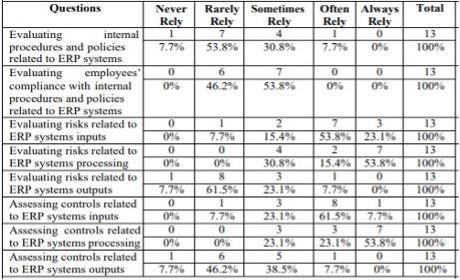

Table 1 Data Analysis For Internal Auditors Answers For Companies With ERP Continuous Internal Audit

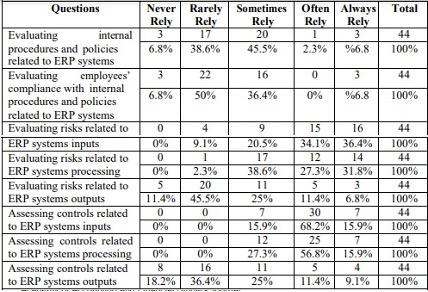

Table 2 Data Analysis For Internal Auditors Answers For Companies Without ERP Continuous Internal Audit

As Table 1 and 2 declared that external auditor rarely relies on internal continuous auditors work in evaluating ERP internal procedures and policies, evaluating employees compliance with ERP internal procedures and policies plus assessing controls of ERP systems outputs. Table 1 illustrate that external auditor sometimes rely on internal continuous auditors work in evaluating risks and assessing controls related to ERP systems input while table 2 external auditor sometimes rely on internal auditors work in evaluating risks related to ERP systems input, evaluating risks and assessing controls related to ERP system processing.

The last, table 1 declare external auditor sometimes rely on internal auditors work in evaluating risks related to ERP systems input, evaluating risks and assessing controls related to ERP system processing while Table 2 declared that external auditor almost relies on internal continuous auditors work in assessing controls related to ERP systems input. So we can conclude, ERP system has a significant impact on the efficiency, fraud risk reduction, knowledge application, as well as the credibility of the auditing team, the most important factors for the successful use of fraud mitigation techniques rely on ERP systems, which have continuous audit functions.

Question: 1. Why do we need to do an evaluation like the case above after ERP implementation? Why would an auditor need to be involved in after ERP implementations? Explain your answer based on the case!

Questions Total Never Rely 1 7.7% Rarely Sometimes Rely Rely 7 4 53.8% 30.8% Often Always Rely Rely 1 0 7.7% 0% 13 100 0 0% 6 46.2% 7 53.8% 0 0% 0 0% 13 100% Evaluating intemal procedures and policies related to ERP systems Evaluating employees compliance with internal procedures and policies related to ERP systems Evaluating risks related to ERP systems inputs Evaluating risks related to ERP systems processing Evaluating risks related to ERP systems outputs Assessing controls related to ERP systems inputs Assessing controls related to ERP systems processing Assessing controls related to ERP systems outputs 2 15.4% 4 30.89 0 0% 0 0% 1 7.7% 0 0% 0 096 1 7.7% 1 7.79 O 0% 8 61.5% 1 7.7% 0 0% 6 46.2% 23.196 3 23.196 3 23.1% 5 38.59% 7 3 53.8% 23.1% 2 7 15.4% 53.8% 1 0 779 0% 8 1 61.596 7.7% 3 7 23.19653.8% 0 7.7% 0% 13 100% 13 100% 13 100% 13 100% 13 100% 13 100% Never Rarely Sometimes Often Always Total Rely Rely Rely Rely Rely 3 17 20 1 3 44 6.8% 38.6% 45.5% 2.3% %6.8 100% 3 22 16 0 3 44 6.8% 50% 36.4% 0% %6.8 100% Questions Evaluating internal procedures and policies related to ERP systems Evaluating employees compliance with internal procedures and policies related to ERP systems Evaluating risks related to ERP systems inputs Evaluating risks related to ERP systems processing Evaluating risks related to ERP systems outputs Assessing controls related to ERP systems inputs Assessing controls related to ERP systems processing Assessing controls related to ERP systems outputs 9 20.5% 17 38.6% 11 0 0% 0 0% 5 11.4% 0 0% 0 0% 8 18.2% 4 9.1% 1 2.3% 20 45.5% 0 0% 0 0% 16 36.4% 25% 7 15.9% 12 27.3% 11 25% 15 16 34.1% 36.4% 12 14 27.3% 31.8% 5 3 11.4% 6.8% 30 7 68.2% 15.9% 25 7 56.8% 15.9% 5 4 11.4% 9.1% 44 100% 44 100% 44 100% 44 100% 44 100% 44 100%Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts