Question: Case Study: Billy Griffiths Billy Griffiths is the newly appointed management accountant for Hopeless Ltd. The company has an appalling history in terms of its

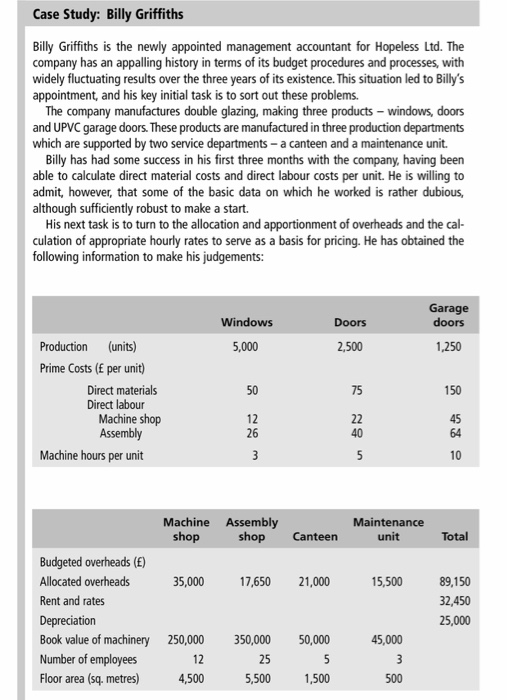

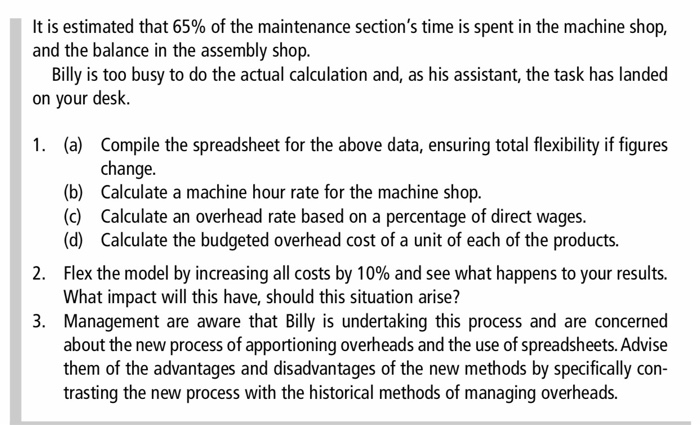

Case Study: Billy Griffiths Billy Griffiths is the newly appointed management accountant for Hopeless Ltd. The company has an appalling history in terms of its budget procedures and processes, with widely fluctuating results over the three years of its existence. This situation led to Billy's appointment, and his key initial task is to sort out these problems. The company manufactures double glazing, making three products - windows, doors and UPVC garage doors. These products are manufactured in three production departments which are supported by two service departments - a canteen and a maintenance unit. Billy has had some success in his first three months with the company, having been able to calculate direct material costs and direct labour costs per unit. He is willing to admit, however, that some of the basic data on which he worked is rather dubious, although sufficiently robust to make a start. His next task is to turn to the allocation and apportionment of overheads and the cal- culation of appropriate hourly rates to serve as a basis for pricing. He has obtained the following information to make his judgements: Windows 5,000 Doors 2,500 Garage doors 1,250 50 75 150 Production (units) Prime Costs ( per unit) Direct materials Direct labour Machine shop Assembly Machine hours per unit 12 26 22 40 45 64 3 un 10 Canteen Maintenance unit Total 21,000 15,500 Machine Assembly shop shop Budgeted overheads (5) Allocated overheads 35,000 17,650 Rent and rates Depreciation Book value of machinery 250,000 350,000 Number of employees 12 25 Floor area (sq. metres) 4,500 5,500 89,150 32,450 25,000 50,000 5 1,500 45,000 3 500 It is estimated that 65% of the maintenance section's time is spent in the machine shop, and the balance in the assembly shop. Billy is too busy to do the actual calculation and, as his assistant, the task has landed on your desk. 1. (a) Compile the spreadsheet for the above data, ensuring total flexibility if figures change. (b) Calculate a machine hour rate for the machine shop. (c) Calculate an overhead rate based on a percentage of direct wages. (d) Calculate the budgeted overhead cost of a unit of each of the products. 2. Flex the model by increasing all costs by 10% and see what happens to your results. What impact will this have, should this situation arise? 3. Management are aware that Billy is undertaking this process and are concerned about the new process of apportioning overheads and the use of spreadsheets. Advise them of the advantages and disadvantages of the new methods by specifically con- trasting the new process with the historical methods of managing overheads. Case Study: Billy Griffiths Billy Griffiths is the newly appointed management accountant for Hopeless Ltd. The company has an appalling history in terms of its budget procedures and processes, with widely fluctuating results over the three years of its existence. This situation led to Billy's appointment, and his key initial task is to sort out these problems. The company manufactures double glazing, making three products - windows, doors and UPVC garage doors. These products are manufactured in three production departments which are supported by two service departments - a canteen and a maintenance unit. Billy has had some success in his first three months with the company, having been able to calculate direct material costs and direct labour costs per unit. He is willing to admit, however, that some of the basic data on which he worked is rather dubious, although sufficiently robust to make a start. His next task is to turn to the allocation and apportionment of overheads and the cal- culation of appropriate hourly rates to serve as a basis for pricing. He has obtained the following information to make his judgements: Windows 5,000 Doors 2,500 Garage doors 1,250 50 75 150 Production (units) Prime Costs ( per unit) Direct materials Direct labour Machine shop Assembly Machine hours per unit 12 26 22 40 45 64 3 un 10 Canteen Maintenance unit Total 21,000 15,500 Machine Assembly shop shop Budgeted overheads (5) Allocated overheads 35,000 17,650 Rent and rates Depreciation Book value of machinery 250,000 350,000 Number of employees 12 25 Floor area (sq. metres) 4,500 5,500 89,150 32,450 25,000 50,000 5 1,500 45,000 3 500 It is estimated that 65% of the maintenance section's time is spent in the machine shop, and the balance in the assembly shop. Billy is too busy to do the actual calculation and, as his assistant, the task has landed on your desk. 1. (a) Compile the spreadsheet for the above data, ensuring total flexibility if figures change. (b) Calculate a machine hour rate for the machine shop. (c) Calculate an overhead rate based on a percentage of direct wages. (d) Calculate the budgeted overhead cost of a unit of each of the products. 2. Flex the model by increasing all costs by 10% and see what happens to your results. What impact will this have, should this situation arise? 3. Management are aware that Billy is undertaking this process and are concerned about the new process of apportioning overheads and the use of spreadsheets. Advise them of the advantages and disadvantages of the new methods by specifically con- trasting the new process with the historical methods of managing overheads

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts