Case Study: Google Inc.s Acquisition of AdMob; Questions 1,5 1. How do investors evaluate young technology companies

Question:

Case Study:

Google Inc.’s Acquisition of AdMob; Questions 1,5

1. How do investors evaluate young technology companies such as Google and how do these

investor evaluations in turn impact management decisions? >> (Hint: Entrepreneurial value-based management framework).

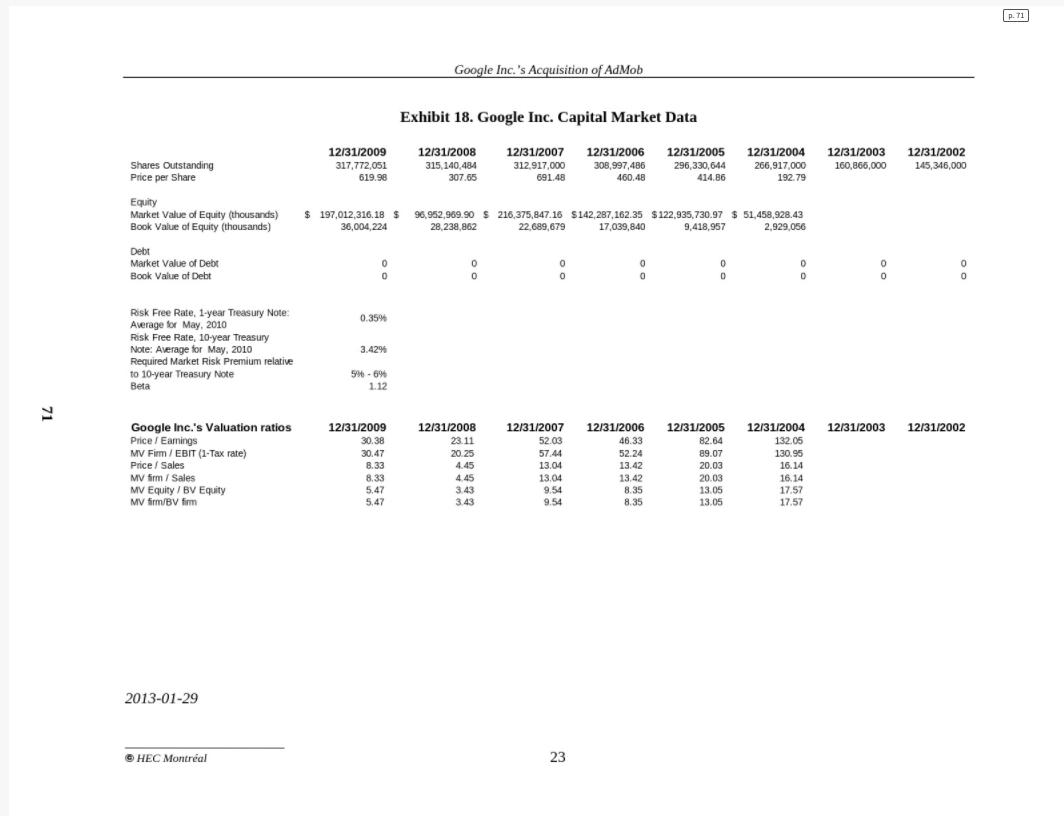

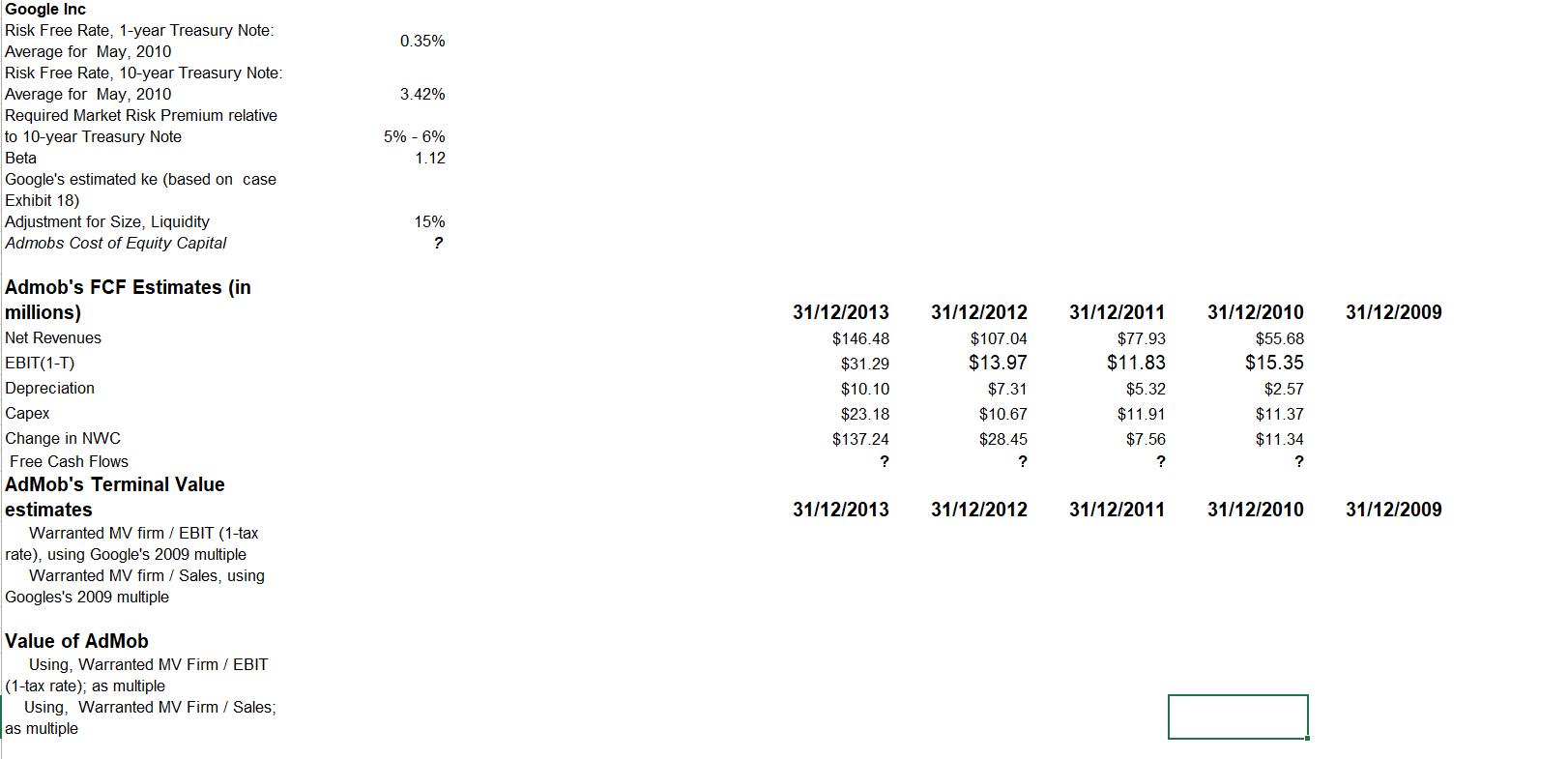

5. How would you value AdMob at the end of 2009:

> as a stand-alone firm, (Hint: _ fill out the spreadsheet)

> as an acquisition target.

Spreadsheet: