Question: Chapter 11 case #11-33 Pinnacle Manufacturing Part 2 In Part 1 of this case study pages 274-276 you obtained an understanding of internal control and

Chapter 11 case #11-33 Pinnacle Manufacturing Part 2

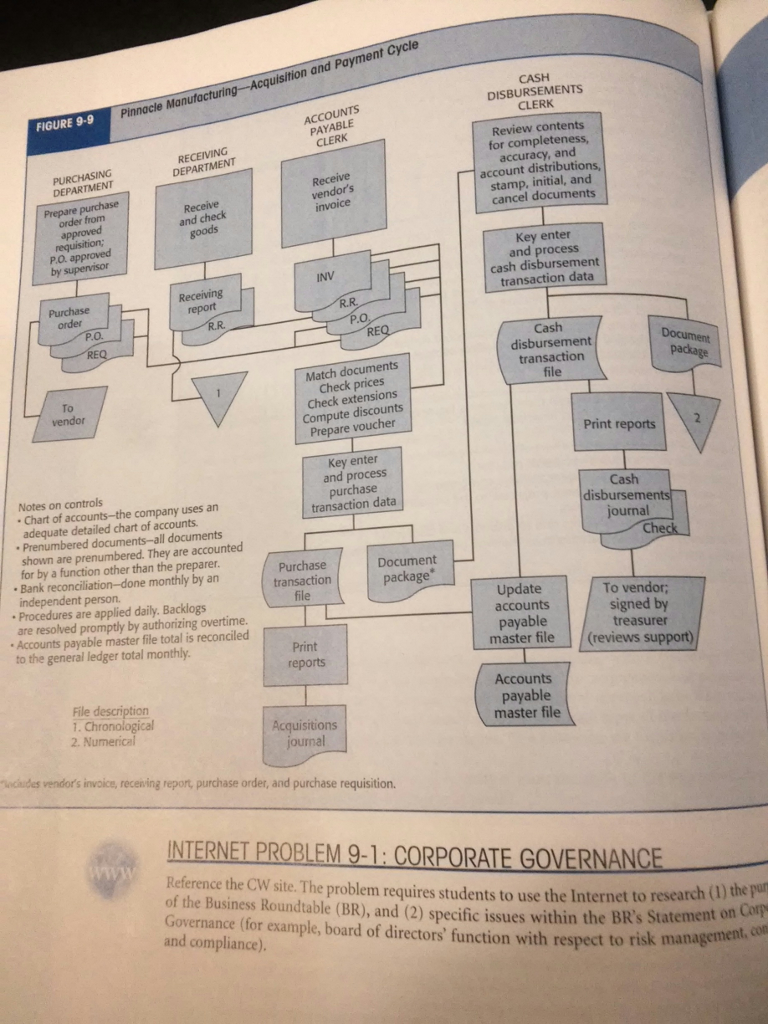

In Part 1 of this case study pages 274-276 you obtained an understanding of internal control and made an initial assessment of control risk for each transaction related audit objective for acquisition and cash disbursement transactions. The purpose of Part 2 is to continue the assessment of control risk by determining the appropriate tests of control and substantive tests of transactions

Assume that Part 1 is was determined that the key internal controls are the following 1-Segregation of the purchasing, receiving, and cash disbursement functions 2-Review of supportive documents and signing of checks by an independent, authorized person 3-Use of prenumbered checks properly accounted for 4-Use of prenumbered purchase orders promptly accounted for 5-Use of prenumberbed document package property accounted for 6-Internal verification of document package before check preparation 7-Independent monthly reconciliation of bank statement

For requirements a and b you should follow a format similar to the one illustrated for sales in Table 11-2 pages 315-316. You should prepare one matrix for acquisitions and a separate one for cash disbursements. Observe that the first column in each matrix should include the transaction related audit objectives from the top row in the worksheet you prepared for Problem 9-31. Also the key internal controls include only those 7 just listed and the tests of controls include only those you developed in requirement a. The substantive tests of transactions procedures should be designed based on an assumption that the results of the tests of controls will be favorable

A Design tests of controls audit procedures that will provide appropriate evidence for each of these controls. Do not include more than 2 sets of control for each internal control

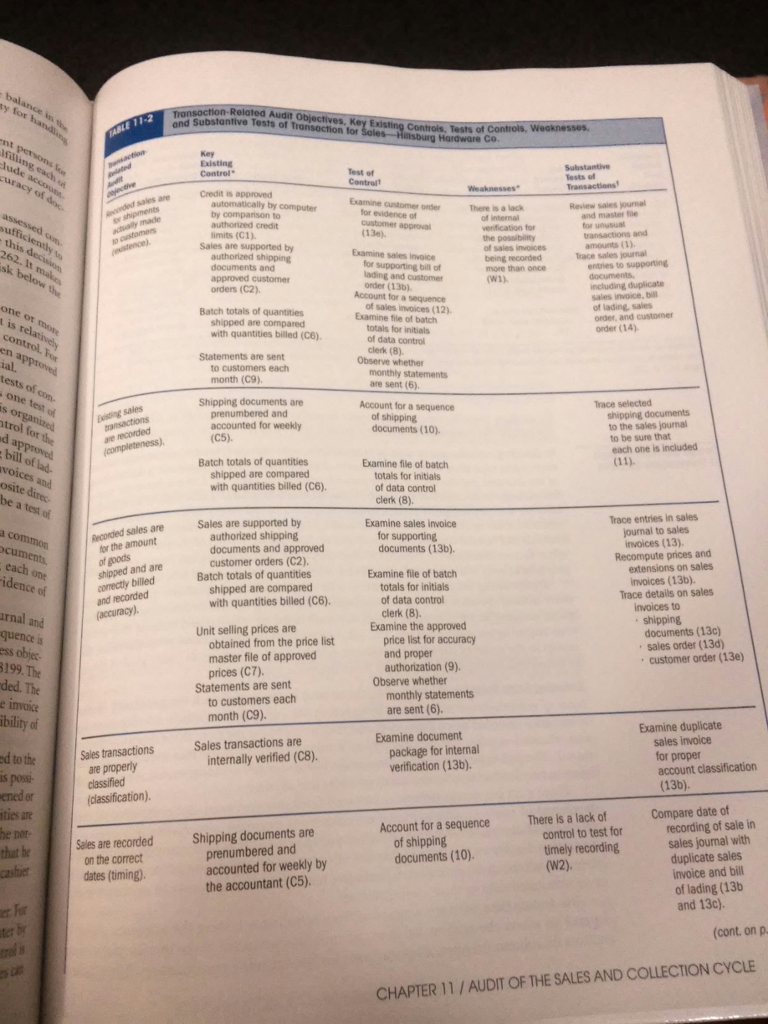

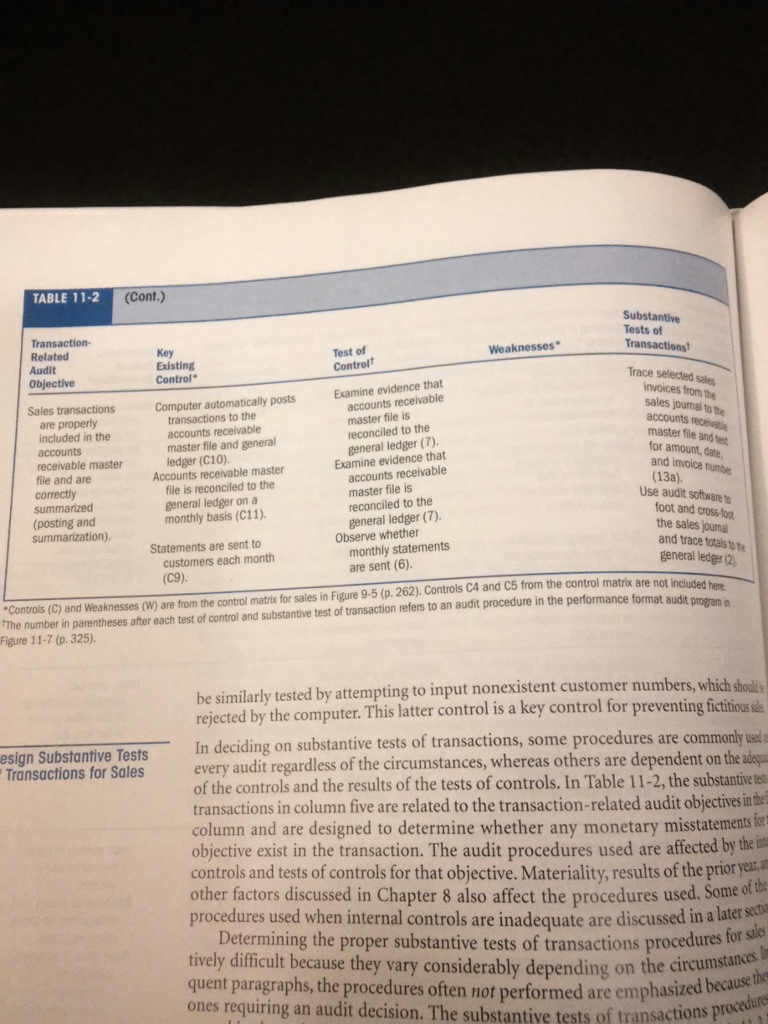

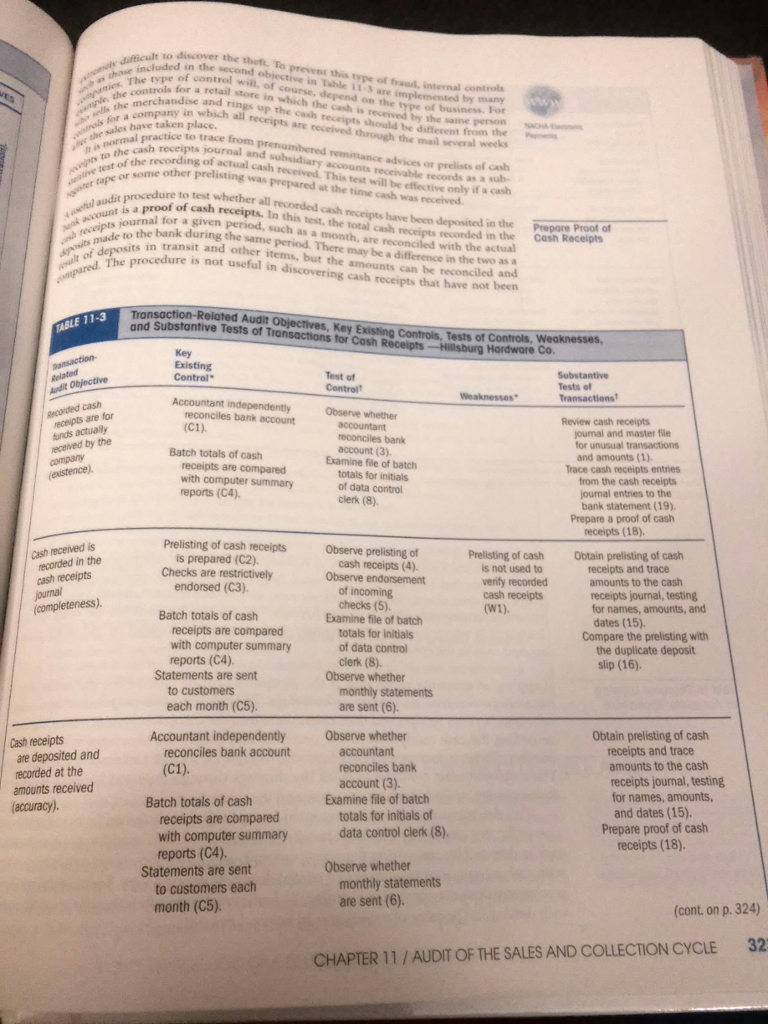

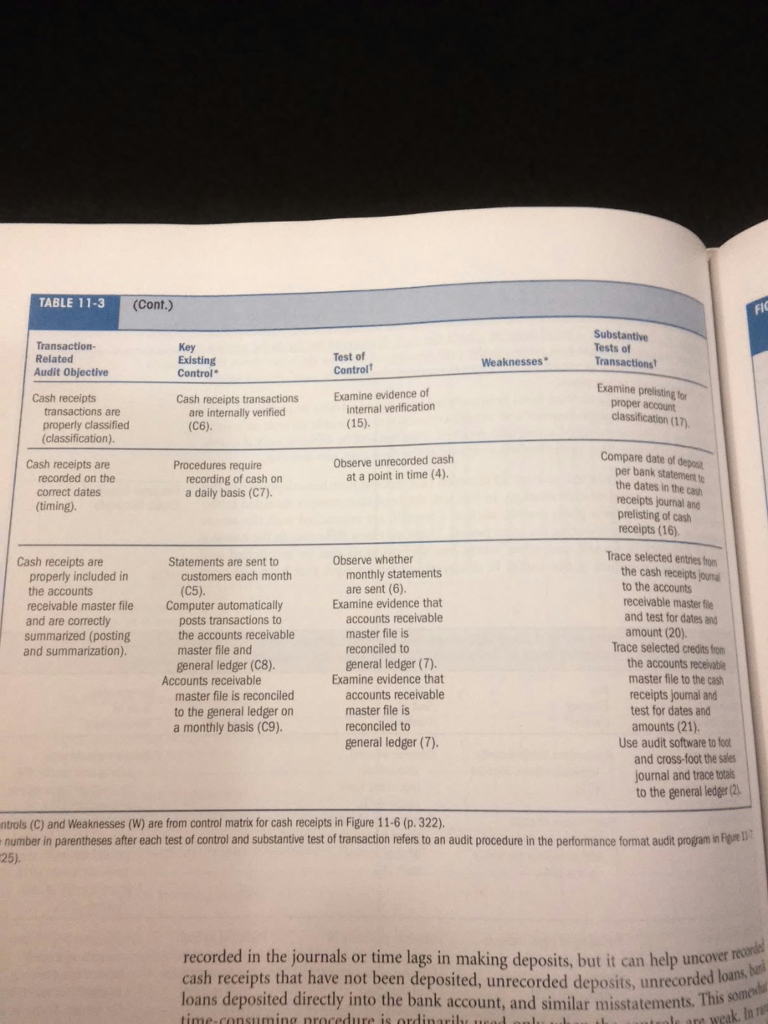

B Although controls appear to be well designed and test of control deviations are not expected last year's results indicate that misstatements may still exist. Therefore you decide to perform substantive tests of transactions for acquisitions and cash disbursements. Design substantive tests of transactions for any objective. Use Tables 11-2 on pages 315-316 and 11-3 on pages 323-324 as frames of reference

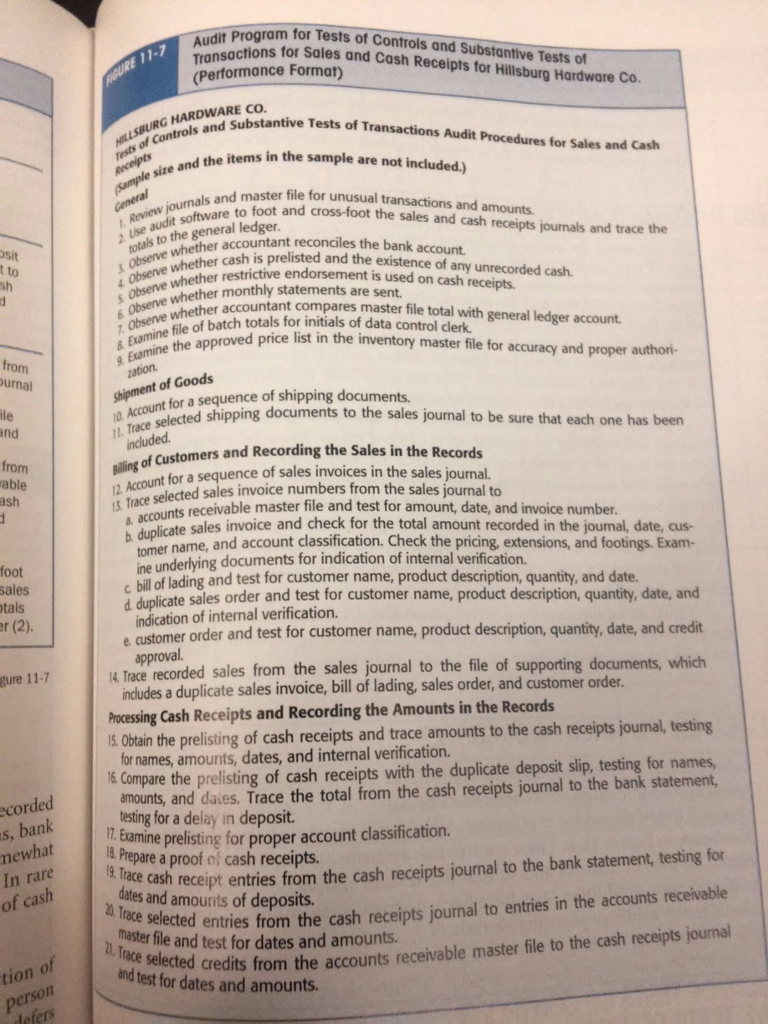

C Combine the tests of controls and substantive tests of transactions designed in requirements a and b into a performance format. Include both tests of acquisitions and cash disbursements in the same audit program. Use Figure 11-7 on page 325 as a frame of reference for preparing the performance format audit program page 276

page 276 page 275

page 275 page 274

page 274

CASH DISBURSEMENTS CLERK FIGURE 9-9 YABLE CLERK Review contents for completeness, accuracy, and account distributions, stamp, initial, and cancel documents RECEIVING DEPARTMENT Receive order from and check .. approved by Key enter and process cash disbursement transaction data INV R. 0. RE Cash disbursement transaction file Match documents Check prices Check extensions Compute discounts Prepare voucher To Print reports Notes on controls Chart of accounts-the company uses an adequate detailed chart of accounts Key enter and process purchase transaction data Cash disburse shown are prenumbered. They are accounted for by a function other than the preparer. Bank reconciliation-done independent person. Procedures are applied daily. Backlogs are resolved promptly by authorizing overtime. Purchase Document package by an file Update accounts payable master file To vendor Accounts payable master file total is reconciled to the general ledger total monthly Print reports signed by treasurer (reviews support) Accounts payable master file File description 2. Numerical Acquisitions cudes vendor's invoice, recening report, purchase order, and purchase requisition. INTERNET PROBLEM 9-1: CORPORATE GOVERNANCE Reference the CW site. The problem requires students to use the Internet to resea of the Business Roundtable (BR), and (2) specific issues within the BR's Statemento Governance (for example, board of directors' function with respect to risk manag and compliance) arch (1) the pun Corp CASH DISBURSEMENTS CLERK FIGURE 9-9 YABLE CLERK Review contents for completeness, accuracy, and account distributions, stamp, initial, and cancel documents RECEIVING DEPARTMENT Receive order from and check .. approved by Key enter and process cash disbursement transaction data INV R. 0. RE Cash disbursement transaction file Match documents Check prices Check extensions Compute discounts Prepare voucher To Print reports Notes on controls Chart of accounts-the company uses an adequate detailed chart of accounts Key enter and process purchase transaction data Cash disburse shown are prenumbered. They are accounted for by a function other than the preparer. Bank reconciliation-done independent person. Procedures are applied daily. Backlogs are resolved promptly by authorizing overtime. Purchase Document package by an file Update accounts payable master file To vendor Accounts payable master file total is reconciled to the general ledger total monthly Print reports signed by treasurer (reviews support) Accounts payable master file File description 2. Numerical Acquisitions cudes vendor's invoice, recening report, purchase order, and purchase requisition. INTERNET PROBLEM 9-1: CORPORATE GOVERNANCE Reference the CW site. The problem requires students to use the Internet to resea of the Business Roundtable (BR), and (2) specific issues within the BR's Statemento Governance (for example, board of directors' function with respect to risk manag and compliance) arch (1) the pun Corp

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts