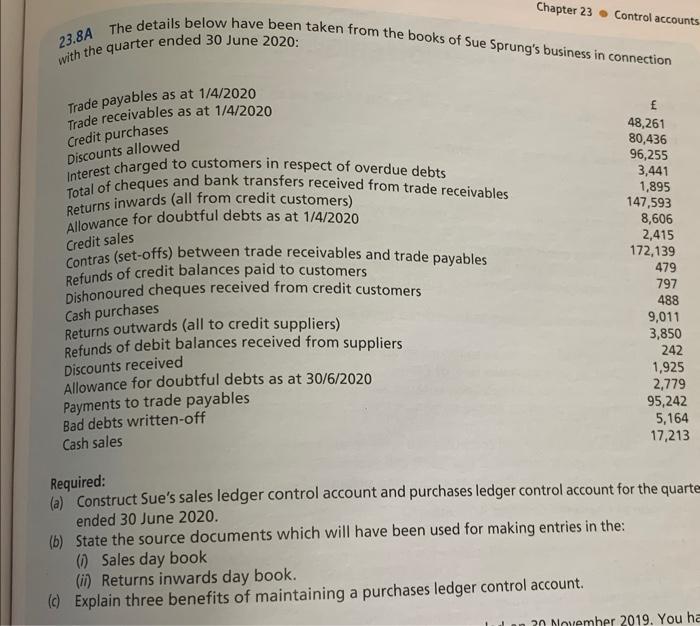

Question: Chapter 23 - Control accounts 23.8A The details below have been taken from the books of Sue Sprung's business in connection with the quarter ended

Chapter 23 - Control accounts 23.8A The details below have been taken from the books of Sue Sprung's business in connection with the quarter ended 30 June 2020: Trade payables as at 1/4/2020 Trade receivables as at 1/4/2020 credit purchases Discounts allowed Interest charged to customers in respect of overdue debts Total of cheques and bank transfers received from trade receivables Returns inwards (all from credit customers) Allowance for doubtful debts as at 1/4/2020 credit sales contras (set-offs) between trade receivables and trade payables Refunds of credit balances paid to customers Dishonoured cheques received from credit customers Cash purchases Returns outwards (all to credit suppliers) Refunds of debit balances received from suppliers Discounts received Allowance for doubtful debts as at 30/6/2020 Payments to trade payables Bad debts written-off Cash sales f 48,261 80,436 96,255 3,441 1,895 147,593 8,606 2,415 172,139 479 797 488 9,011 3,850 242 1,925 2,779 95,242 5,164 17,213 Required: (a) Construct Sue's sales ledger control account and purchases ledger control account for the quarte ended 30 June 2020. (b) State the source documents which will have been used for making entries in the: (i) Sales day book (ii) Returns inwards day book. (c) Explain three benefits of maintaining a purchases ledger control account

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts