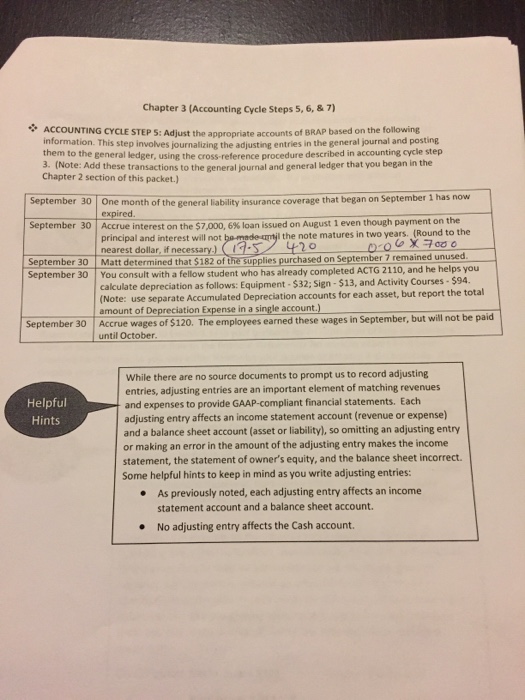

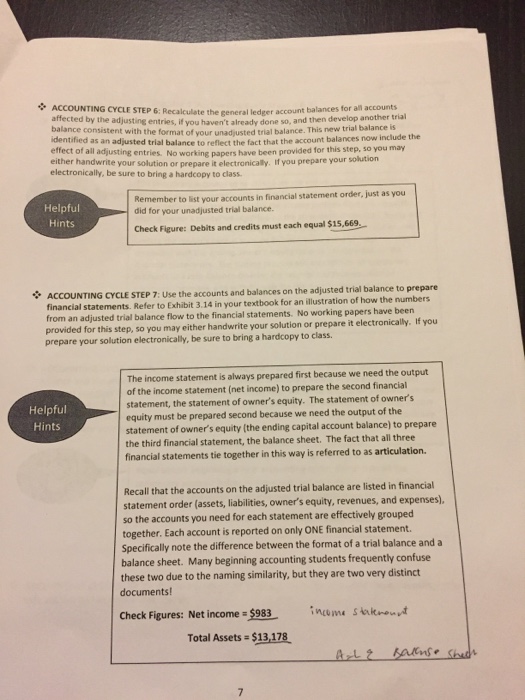

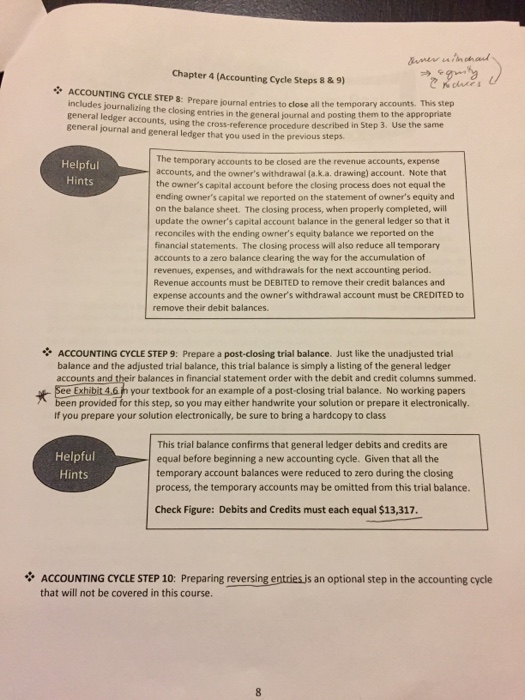

Question: Chapter 3 (Accounting Cycle Steps 5, 6,&7) ACCOUNTING CYCLE STEPS: Adjust the appropriate accounts of BRAP based on the following information. This step involves journalizing

Chapter 3 (Accounting Cycle Steps 5, 6,&7) ACCOUNTING CYCLE STEPS: Adjust the appropriate accounts of BRAP based on the following information. This step involves journalizing the adjusting entries in the general journal and posting them to the general ledger, using the cross-reference procedure described in accounting cycle step h unote Add these transactions to the general journal and general ledger that you began in the Chapter 2 section of this packet.) September 30 One month of the general iability insurance coverage that began on September 1 has now September 30 | Accrue interest on the $7,000, 6% loan issued on August 1 even though payment on the principal and interest will not l the note matures in two years. (Round to the nearest dollar, if necessary)S2 September 30 Matt determined that $182 of the supplies purchased on September 7 remained unused September 30 You consult with a fellow student who has already completed ACTG 2110, a calculate depreciation as follows: Equipment- $32; Sign-$13, and Activity Courses $94. (Note: use separate Accumulated Depreciation accounts for each asset, but report the total amount of Depreciation Expense in a single account.) Accrue wages of $120. The employees earned these wages in September, but will not be paid September 30 until October While there are no source documents to prompt us to record adjusting entries, adjusting entries are an important element of matching revenues and expenses to provide GAAP-compliant financial statements. Each adjusting entry affects an income statement account (revenue or expense) and a balance sheet account (asset or liability), so omitting an adjusting entry or making an error in the amount of the adjusting entry makes the income statement, the statement of owner's equity, and the balance sheet incorrect. Some helpful hints to keep in mind as you write adjusting entries: Helpful Hints As previously noted, each adjusting entry affects an income statement account and a balance sheet account. No adjusting entry affects the Cash account. Chapter 3 (Accounting Cycle Steps 5, 6,&7) ACCOUNTING CYCLE STEPS: Adjust the appropriate accounts of BRAP based on the following information. This step involves journalizing the adjusting entries in the general journal and posting them to the general ledger, using the cross-reference procedure described in accounting cycle step h unote Add these transactions to the general journal and general ledger that you began in the Chapter 2 section of this packet.) September 30 One month of the general iability insurance coverage that began on September 1 has now September 30 | Accrue interest on the $7,000, 6% loan issued on August 1 even though payment on the principal and interest will not l the note matures in two years. (Round to the nearest dollar, if necessary)S2 September 30 Matt determined that $182 of the supplies purchased on September 7 remained unused September 30 You consult with a fellow student who has already completed ACTG 2110, a calculate depreciation as follows: Equipment- $32; Sign-$13, and Activity Courses $94. (Note: use separate Accumulated Depreciation accounts for each asset, but report the total amount of Depreciation Expense in a single account.) Accrue wages of $120. The employees earned these wages in September, but will not be paid September 30 until October While there are no source documents to prompt us to record adjusting entries, adjusting entries are an important element of matching revenues and expenses to provide GAAP-compliant financial statements. Each adjusting entry affects an income statement account (revenue or expense) and a balance sheet account (asset or liability), so omitting an adjusting entry or making an error in the amount of the adjusting entry makes the income statement, the statement of owner's equity, and the balance sheet incorrect. Some helpful hints to keep in mind as you write adjusting entries: Helpful Hints As previously noted, each adjusting entry affects an income statement account and a balance sheet account. No adjusting entry affects the Cash account

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts