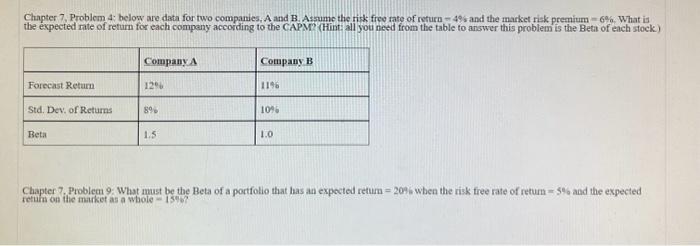

Question: Chapter 7, Problem 4: below are data for two companies, A and B. Assume the risk frev rate of return =4% and the market risk

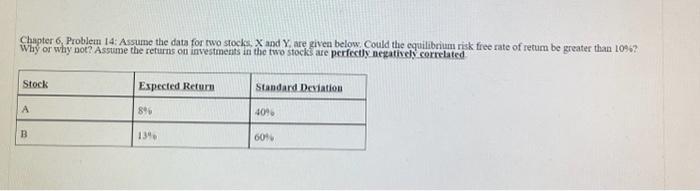

Chapter 7, Problem 4: below are data for two companies, A and B. Assume the risk frev rate of return =4% and the market risk premium =6%. What is the expected nate of return for each company according to the CAPM? (Hint: all you need from the table to answer this problem is the Beta of each stock) Chapter 7, Problecn 9: What must be the Beta of a portfolio that has an expocted return =20 is when the risk free rate of return =5% and the expected Chapter probiecn 9, What must be the retuhn on ifie makket as a whole = Iswo? Chapter 6. Problem 14: Assume the data for two stocks, X and Y, are given below. Could the cquilibrium risk free rate of retum be greater than 1096 ? Why or why pot? Assume the returns on investments in the two stocks are perfectly netatively correlated

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts