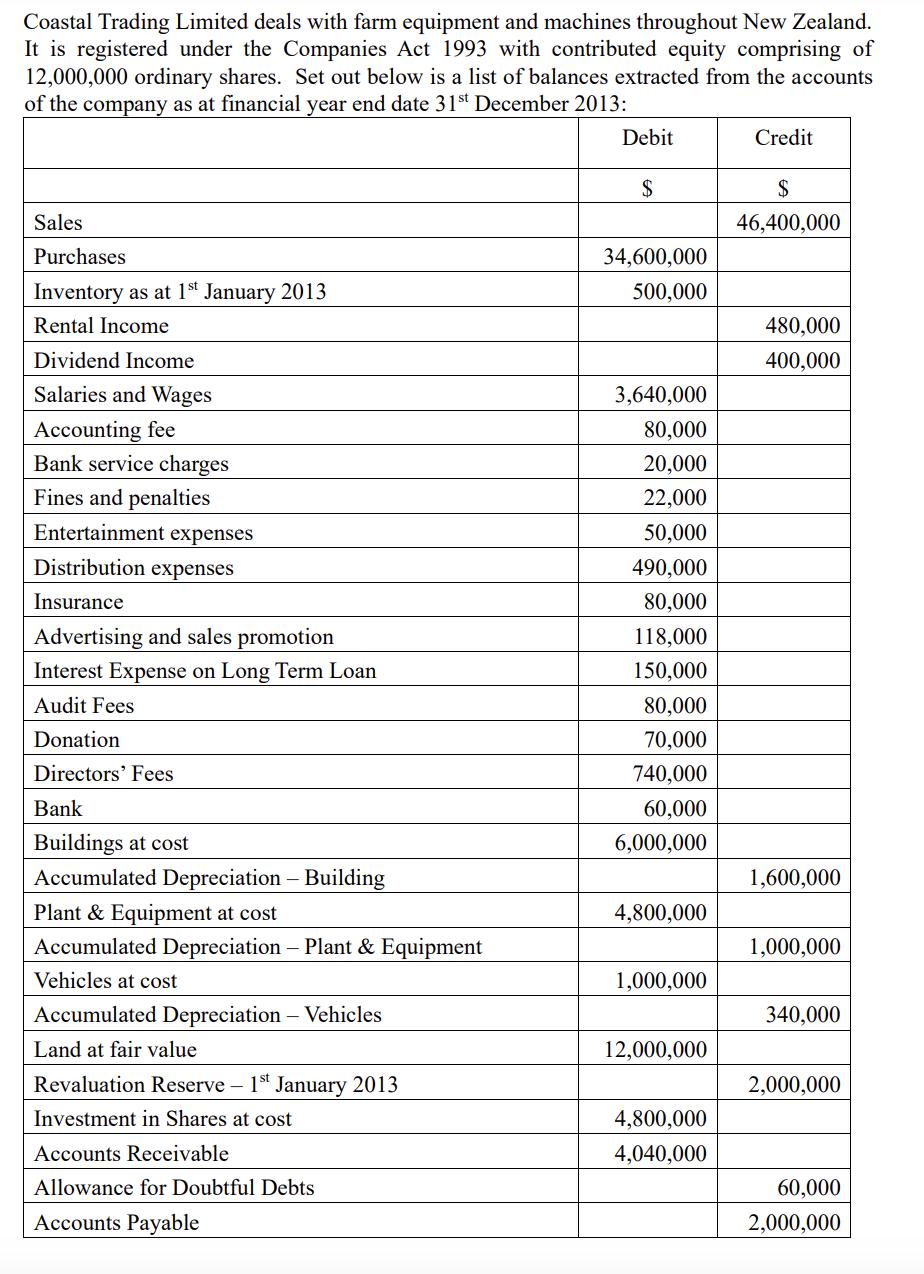

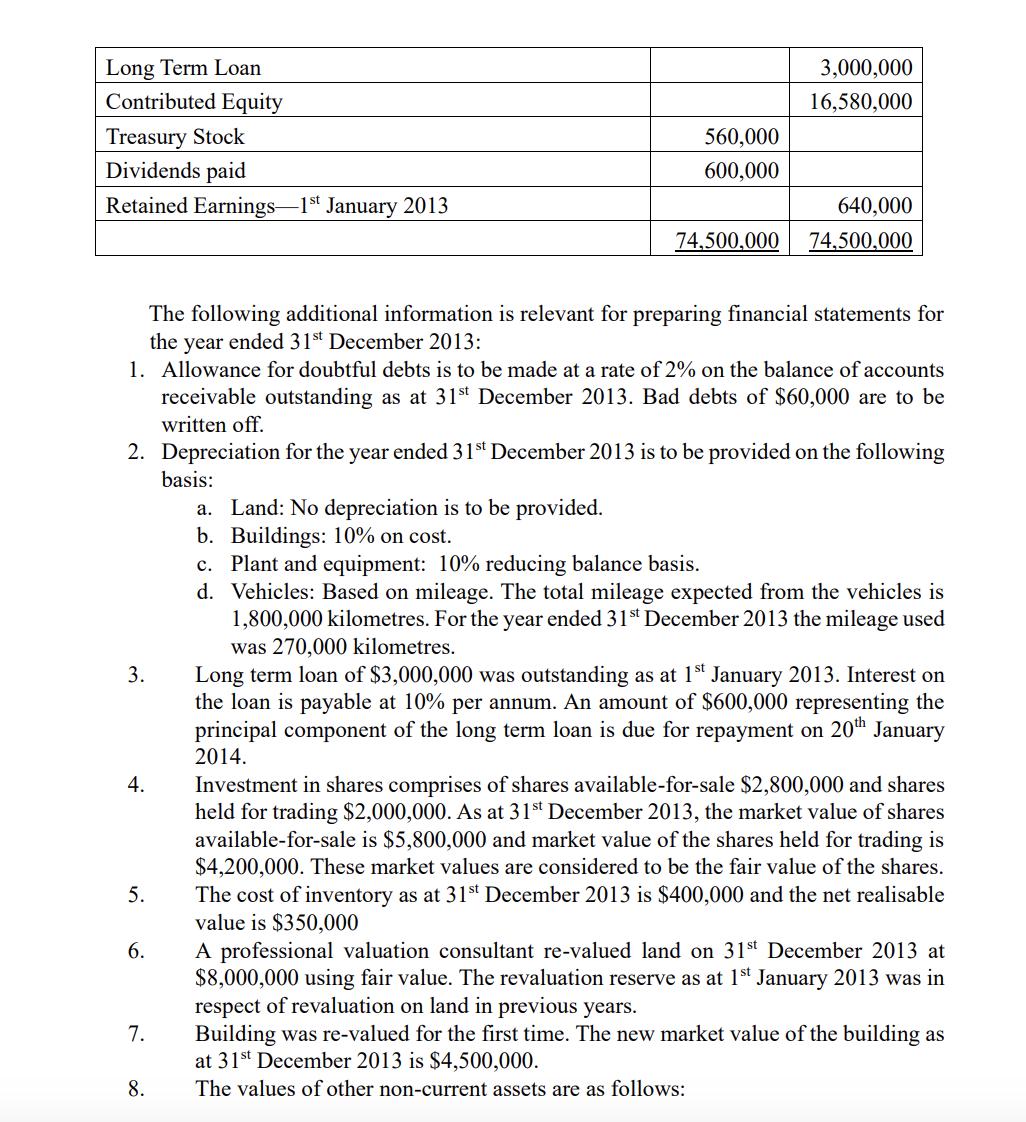

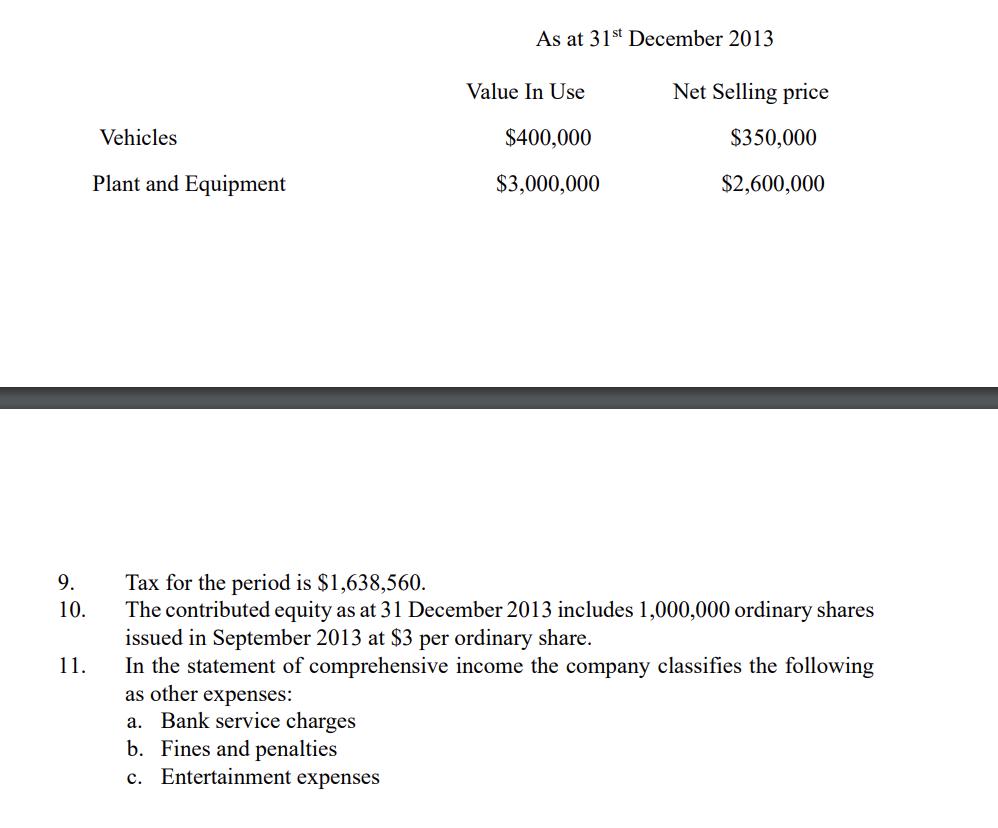

Coastal Trading Limited deals with farm equipment and machines throughout New Zealand. It is registered under...

Fantastic news! We've Found the answer you've been seeking!

Question:

Expert Answer:

Answer Answer a Date Particulars Dr Cr Bad Debts 40000 AC receivable 40000 Doubtful Debts 20000 Provision for Doubtful Debts 4040000 40000 x 260000 20... View the full answer

Related Book For

Financial Reporting Financial Statement Analysis and Valuation a strategic perspective

ISBN: 978-1337614689

9th edition

Authors: James M. Wahlen, Stephen P. Baginski, Mark Bradshaw

Posted Date: