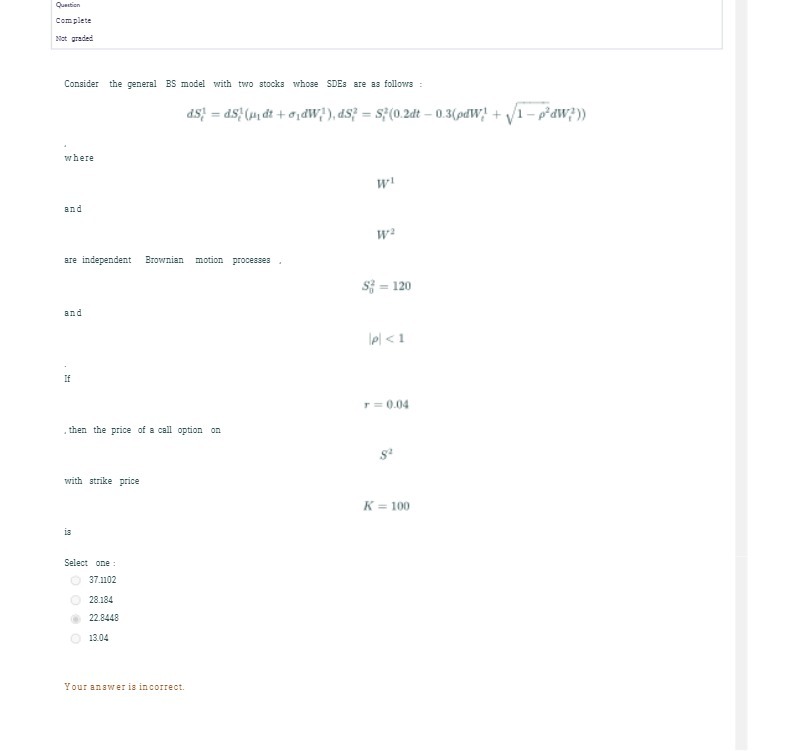

Question: Complete Not graded Consider the general BS model with two stocks whose SDEs are as follows : d5) = d5) (u di + oldW/ ),

Complete Not graded Consider the general BS model with two stocks whose SDEs are as follows : d5) = d5) (u di + oldW/ ), ds; = $;(0.2dt - 0.3(odw) + (1 - paw?)) where and are independent Brownian motion processes S = 120 and Ipl

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock