Question: Compute, AB , the correlation between frontier portfolios A and B. Calculate the expected return on the global minimum variance portfolio. Calculate the maximum possible

- Compute, AB, the correlation between frontier portfolios A and B.

- Calculate the expected return on the global minimum variance portfolio.

- Calculate the maximum possible Sharpe Ratio from these frontier portfolios, when the risk free rate is 2% per annum.

- Explain, illustrating with graphs, the difference between the portfolio frontier when there is a risk free asset available for investment as compared to the portfolio frontier when there is not.

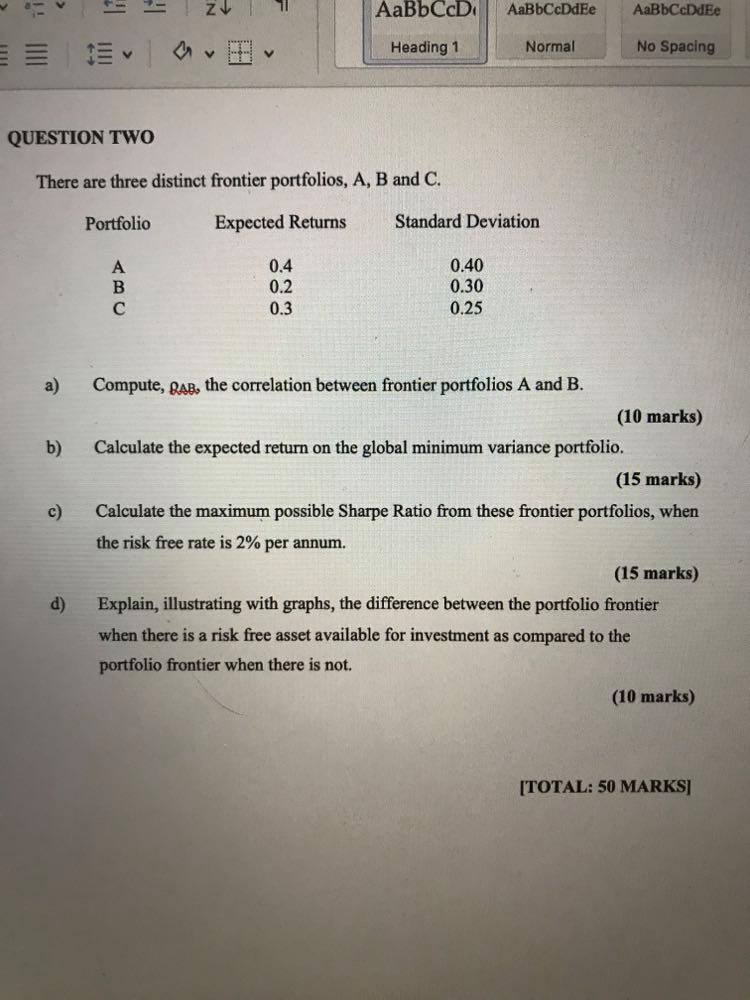

AaBbCcD AaBbCcDdEe AaBbCcDdEe Heading 1 Normal No Spacing V V V QUESTION TWO There are three distinct frontier portfolios, A, B and C. Portfolio Expected Returns Standard Deviation A B 0.4 0.2 0.3 0.40 0.30 0.25 a) b) C) Compute, RAB, the correlation between frontier portfolios A and B. (10 marks) Calculate the expected return on the global minimum variance portfolio. (15 marks) Calculate the maximum possible Sharpe Ratio from these frontier portfolios, when the risk free rate is 2% per annum. (15 marks) Explain, illustrating with graphs, the difference between the portfolio frontier when there is a risk free asset available for investment as compared to the portfolio frontier when there is not. (10 marks) d) [TOTAL: 50 MARKS] AaBbCcD AaBbCcDdEe AaBbCcDdEe Heading 1 Normal No Spacing V V V QUESTION TWO There are three distinct frontier portfolios, A, B and C. Portfolio Expected Returns Standard Deviation A B 0.4 0.2 0.3 0.40 0.30 0.25 a) b) C) Compute, RAB, the correlation between frontier portfolios A and B. (10 marks) Calculate the expected return on the global minimum variance portfolio. (15 marks) Calculate the maximum possible Sharpe Ratio from these frontier portfolios, when the risk free rate is 2% per annum. (15 marks) Explain, illustrating with graphs, the difference between the portfolio frontier when there is a risk free asset available for investment as compared to the portfolio frontier when there is not. (10 marks) d) [TOTAL: 50 MARKS]

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts