Computer Service Corporation The Setting: Meeting Notice Subject: Allocation of parts overhead to products Purpose: To...

Fantastic news! We've Found the answer you've been seeking!

Question:

Transcribed Image Text:

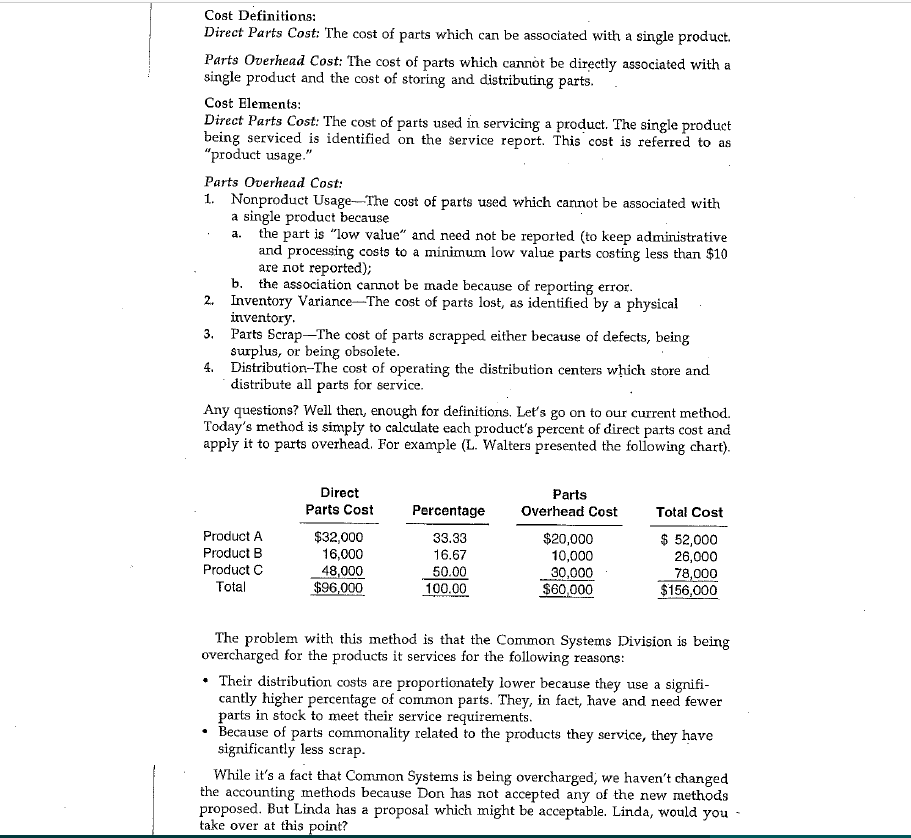

Computer Service Corporation The Setting: Meeting Notice Subject: Allocation of parts overhead to products Purpose: To decide on an equitable method Location: Executive Conference Room Time: 1:00 p.m. Thursday Attendees John Stevens, President, Computer Service Corporation Don Vawter, President, Complex Systems Division Linda Westbrook, President, Common Systems Division Larry Walters, Corporate Director of Accounting Transcript: The meeting to decide on an equitable method of allocating parts overhead was held on schedule. The following is a transcript of the discussion. John Stevens: Good afternoon. For some time now, you have been studying various methods of allocating parts overhead to the products we service. As I understand it, no agreement has been reached on a single method that is accept- able to all. I'm pleased with the effort you have been making, but also feel it is important we come to an agreement and I feel that we can reach agreement before we adjourn today. To reach agreement, each of you will have to put aside, to some extent, your division's particular interest and focus on a financial approach that is in the best interest of the total corporation. I am convinced that our final agreement will turn on a way of allocating this important element of service cost to products based on an association that best recognizes cause and effect. To price our services properly, we must eliminate the product inequities inherent in our current method which, as you know, allocates parts overhead to each product serviced based on the proportionate share of the cost of direct parts used. There are, of course, difficulties in associating indirect costs to product in a practical and cost efficient manner. These points, I am sure, will come out as each of you has an opportunity to state your position on the current and proposed methods. Larry, would you start us off by reviewing our current method in detail and remind- ing us why it was put in place when it doesn't seem to work well for anyone today. Larry Walters: Thanks a whole lot for the terrific lead in, John. Or should I say set up! Fact is, there was no disagreement with the current method when it was adopted ten years ago. Of course, we had fewer than 25 products then, and they were all large, complex systems. It wasn't until our product line began to grow and the products became substantially different in complexity that the inequities developed. Before I go any further in reviewing today's method, however, let me run through the definitions and elements of direct parts cost and parts overhead, just to make sure we're all starting from the same point. Cost Definitions: Direct Parts Cost: The cost of parts which can be associated with a single product. Parts Overhead Cost: The cost of parts which cannot be directly associated with a single product and the cost of storing and distributing parts. Cost Elements: Direct Parts Cost: The cost of parts used in servicing a product. The single product being serviced is identified on the service report. This cost is referred to as "product usage." Parts Overhead Cost: 1. Nonproduct Usage-The cost of parts used which cannot be associated with a single product because the part is "low value" and need not be reported (to keep administrative and processing costs to a minimum low value parts costing less than $10 are not reported); b. the association cannot be made because of reporting error. 2. Inventory Variance-The cost of parts lost, as identified by a physical inventory. 3. Parts Scrap--The cost of parts scrapped either because of defects, being surplus, or being obsolete. 4. Distribution-The cost of operating the distribution centers which store and distribute all parts for service. a. Any questions? Well then, enough for definitions. Leť's go on to our current method. Today's method is simply to calculate each product's percent of direct parts cost and apply it to parts overhead. For example (L. Walters presented the following chart). Direct Parts Overhead Cost Parts Cost Percentage Total Cost Product A $32,000 16,000 48,000 $96,000 $ 52,000 26,000 78,000 $156,000 33.33 $20,000 10,000 30,000 $60,000 Product B 16.67 50.00 100.00 Product C Total The problem with this method is that the Common Systems Division is being overcharged for the products it services for the following reasons: • Their distribution costs are proportionately lower because they use a signifi- cantly higher percentage of common parts. They, in fact, have and need fewer parts in stock to meet their service requirements. • Because of parts commonality related to the products they service, they have significantly less scrap. While it's a fact that Common Systems is being overcharged, we haven't changed the accounting methods because Don has not accepted any of the new methods proposed. But Linda has a proposal which might be acceptable. Linda, would you - take over at this point? Linda Westbrook: Thanks, Larry. John, I agree with Larry's presentation of my division's problem. We considered various ways to improve the allocation of costs and settled on this approach as the most practical. • Allocate non-product usage to products based on product usage or direct parts cost. Allocate the other elements of parts overhead cost to product based on the parts inventory by product. A parts inventory by product would be established by associating each part num- ber with a product. For unique parts, this is simple. All of the inventory for these parts would be associated with the unique product. For common parts, an alloca- tion would be made to each product based on usage. This approach could be implemented in a few months. The only thing we are lacking is agreement to implement. Don, are you willing to go along with what I've described? Or do you have objections to my proposal? Don Vawter: John, if you were to decide based on these two presentations, Com- plex System's financial measurements would be adversely affected. I don't disagree with anything that Larry or Linda said. My problem is that they have left out a couple of important facts. First, they failed to mention that those low value parts, which do not require reporting, are mostly used by Common Systems. To allocate them based on usage would unfairly charge my division. Second, they propose to allocate the other elements of parts overhead based on inventory "value." Inventory value will allocate too much cost to Complex Systems because we have the most expensive parts but, at the same time, we occupy a much smaller share of inventory space and have a significantly lower number of units in inventory. To sum up, I agree that ouır present method leaves a lot to be desired, but I request that we don't change uniess we can satisfy all of our concerns. Required: 1. What are the objectives of allocating costs to product? Given the above scenario, what other basis might be used to allocate cost to product? 3. Identify which elements of cost would be included within each product alloca- tion method. 2. Computer Service Corporation The Setting: Meeting Notice Subject: Allocation of parts overhead to products Purpose: To decide on an equitable method Location: Executive Conference Room Time: 1:00 p.m. Thursday Attendees John Stevens, President, Computer Service Corporation Don Vawter, President, Complex Systems Division Linda Westbrook, President, Common Systems Division Larry Walters, Corporate Director of Accounting Transcript: The meeting to decide on an equitable method of allocating parts overhead was held on schedule. The following is a transcript of the discussion. John Stevens: Good afternoon. For some time now, you have been studying various methods of allocating parts overhead to the products we service. As I understand it, no agreement has been reached on a single method that is accept- able to all. I'm pleased with the effort you have been making, but also feel it is important we come to an agreement and I feel that we can reach agreement before we adjourn today. To reach agreement, each of you will have to put aside, to some extent, your division's particular interest and focus on a financial approach that is in the best interest of the total corporation. I am convinced that our final agreement will turn on a way of allocating this important element of service cost to products based on an association that best recognizes cause and effect. To price our services properly, we must eliminate the product inequities inherent in our current method which, as you know, allocates parts overhead to each product serviced based on the proportionate share of the cost of direct parts used. There are, of course, difficulties in associating indirect costs to product in a practical and cost efficient manner. These points, I am sure, will come out as each of you has an opportunity to state your position on the current and proposed methods. Larry, would you start us off by reviewing our current method in detail and remind- ing us why it was put in place when it doesn't seem to work well for anyone today. Larry Walters: Thanks a whole lot for the terrific lead in, John. Or should I say set up! Fact is, there was no disagreement with the current method when it was adopted ten years ago. Of course, we had fewer than 25 products then, and they were all large, complex systems. It wasn't until our product line began to grow and the products became substantially different in complexity that the inequities developed. Before I go any further in reviewing today's method, however, let me run through the definitions and elements of direct parts cost and parts overhead, just to make sure we're all starting from the same point. Cost Definitions: Direct Parts Cost: The cost of parts which can be associated with a single product. Parts Overhead Cost: The cost of parts which cannot be directly associated with a single product and the cost of storing and distributing parts. Cost Elements: Direct Parts Cost: The cost of parts used in servicing a product. The single product being serviced is identified on the service report. This cost is referred to as "product usage." Parts Overhead Cost: 1. Nonproduct Usage-The cost of parts used which cannot be associated with a single product because the part is "low value" and need not be reported (to keep administrative and processing costs to a minimum low value parts costing less than $10 are not reported); b. the association cannot be made because of reporting error. 2. Inventory Variance-The cost of parts lost, as identified by a physical inventory. 3. Parts Scrap--The cost of parts scrapped either because of defects, being surplus, or being obsolete. 4. Distribution-The cost of operating the distribution centers which store and distribute all parts for service. a. Any questions? Well then, enough for definitions. Leť's go on to our current method. Today's method is simply to calculate each product's percent of direct parts cost and apply it to parts overhead. For example (L. Walters presented the following chart). Direct Parts Overhead Cost Parts Cost Percentage Total Cost Product A $32,000 16,000 48,000 $96,000 $ 52,000 26,000 78,000 $156,000 33.33 $20,000 10,000 30,000 $60,000 Product B 16.67 50.00 100.00 Product C Total The problem with this method is that the Common Systems Division is being overcharged for the products it services for the following reasons: • Their distribution costs are proportionately lower because they use a signifi- cantly higher percentage of common parts. They, in fact, have and need fewer parts in stock to meet their service requirements. • Because of parts commonality related to the products they service, they have significantly less scrap. While it's a fact that Common Systems is being overcharged, we haven't changed the accounting methods because Don has not accepted any of the new methods proposed. But Linda has a proposal which might be acceptable. Linda, would you - take over at this point? Linda Westbrook: Thanks, Larry. John, I agree with Larry's presentation of my division's problem. We considered various ways to improve the allocation of costs and settled on this approach as the most practical. • Allocate non-product usage to products based on product usage or direct parts cost. Allocate the other elements of parts overhead cost to product based on the parts inventory by product. A parts inventory by product would be established by associating each part num- ber with a product. For unique parts, this is simple. All of the inventory for these parts would be associated with the unique product. For common parts, an alloca- tion would be made to each product based on usage. This approach could be implemented in a few months. The only thing we are lacking is agreement to implement. Don, are you willing to go along with what I've described? Or do you have objections to my proposal? Don Vawter: John, if you were to decide based on these two presentations, Com- plex System's financial measurements would be adversely affected. I don't disagree with anything that Larry or Linda said. My problem is that they have left out a couple of important facts. First, they failed to mention that those low value parts, which do not require reporting, are mostly used by Common Systems. To allocate them based on usage would unfairly charge my division. Second, they propose to allocate the other elements of parts overhead based on inventory "value." Inventory value will allocate too much cost to Complex Systems because we have the most expensive parts but, at the same time, we occupy a much smaller share of inventory space and have a significantly lower number of units in inventory. To sum up, I agree that ouır present method leaves a lot to be desired, but I request that we don't change uniess we can satisfy all of our concerns. Required: 1. What are the objectives of allocating costs to product? Given the above scenario, what other basis might be used to allocate cost to product? 3. Identify which elements of cost would be included within each product alloca- tion method. 2.

Expert Answer:

Answer rating: 100% (QA)

OBJECTIVES OF ALLOCATING COSTS 1 For decision making 2 To reduce cost... View the full answer

Related Book For

Accounting For Managers Interpreting Accounting Information for Decision Making

ISBN: 978-1119979678

4th edition

Authors: Paul M. Collier

Posted Date:

Students also viewed these accounting questions

-

You have been studying accounting for nearly a semester now and have become convinced of the value of determining a companys net income on an accrual basis. Why do you think the accounting profession...

-

Walters Corporation was formed during 2013 by John Walters. John is the president and sole stockholder. At December 31, 2014, John prepared an income statement for Walters Corporation. John is not an...

-

John Needles has been hired as a systems consultant for Arco Manufacturing. The companys president, Barbara Arco, has told John that the company has been having numerous problems with late deliveries...

-

Social welfare is maximized when O Total social benefits have been maximized O total social costs have been minimized O total social costs equal total social benefits O marginal social costs equal...

-

Four years ago, Ideal Solutions issued convertible preferred stock with a par value of $50 and a stated dividend of 8 percent. Each share of preferred stock can be converted to four shares of common...

-

Find support reactions at A and D and then calculate the axial force N, shear force V, and bending moment M at mid-span of AB. Let L = 14 ft, q 0 =12 lb/ft, P = 50 lb, and M 0 = 300 lb-ft. A Mo y L X...

-

The Doak Company uses prenumbered vouchers. During a given test period, voucher numbers 1000 to 8000 were used. Required: a. Select the first five vouchers to be included in a random sample in each...

-

Stanislaw Timber Company owns 9,000 acres of timberland purchased in 2003 at a cost of $1,400 per acre. At the time of purchase, the land without the timber was valued at $400 per acre. In 2004,...

-

You work for a penetration testing consulting company. Your manager is concerned about the vulnerability of the company's database server that contains the finance and accounting systems. He wants...

-

Apply Thevenin's theorem to find Vo in the circuit of Fig. 4.105? 42 3-9 16 1682

-

The following are the accounts of BMH Limited for the period ending 31 December, 2023. Plant property and equipment (at cost) Accumulated depredation-property (at 1 January 2023) $'000 $'000 129,000...

-

Identify the basic steps in the adoption process.

-

Define and distinguish between an open and a closed adoption.

-

Identify at least five common characteristics of abusers.

-

Define and give an example of an equitable adoption.

-

Identify the four most common forms of neglect.

-

F (C9H8O2) 10 1H more 8 1H 1H 1H Solution Process: 6 PPM. 4 2H 2H 2 (Cs Har) Analysis compound F: Structure of F (paste in chemdraw): Proton NMR: report in this format shift (splitting, integration);...

-

You are standing on the top of a building and throw a ball vertically upward. After 2 seconds, the ball passes you on the way down, and 2 seconds after that, it hits the ground below. a. What is the...

-

a. Produce a i. Profit budget for each of the five years, showing both gross profit and operating profit; ii. Cash flow for each of the five years, and iii. Apply a discounted cash flow technique and...

-

The preferred use of the limited labour hours is: d) prioritise selling to business because the contribution per labour hour is higher

-

Carry out a customer profitability analysis and make recommendations in relation to any future strategies DeepNDark should take in relation to its Top 5 customers.

-

(a) Complete a steady-state simulation of the vinyl-chloride process in Figure 2.6. First, create a simulation flowsheet. Assume that: Cooling water is heated from 30 to \(50^{\circ} \mathrm{C}\)...

-

For the monochlorobenzene separation process in Figure 7.14, the results of an ASPEN PLUS simulation are provided in the multimedia modules under ASPEN \( ightarrow\) Principles of Flowsheet...

-

Complete a simulation of the entire process for the hydrodealkylation of toluene in Figure 6.14. Initially, let the purge/recycle ratio be 0.25 ; then, vary this ratio and determine its effect on the...

Study smarter with the SolutionInn App