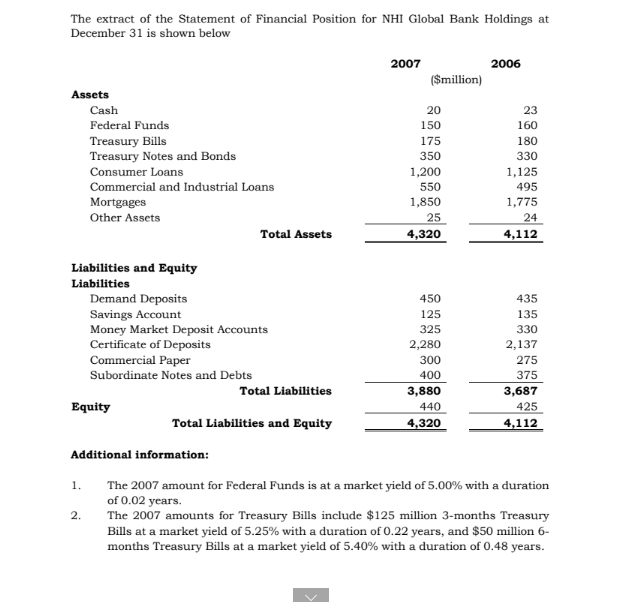

The extract of the Statement of Financial Position for NHI Global Bank Holdings at December 31...

Fantastic news! We've Found the answer you've been seeking!

Question:

Transcribed Image Text:

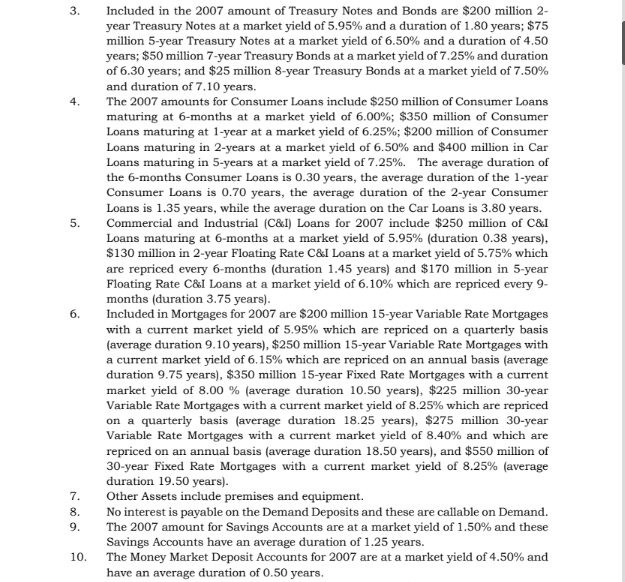

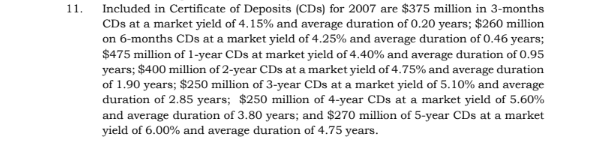

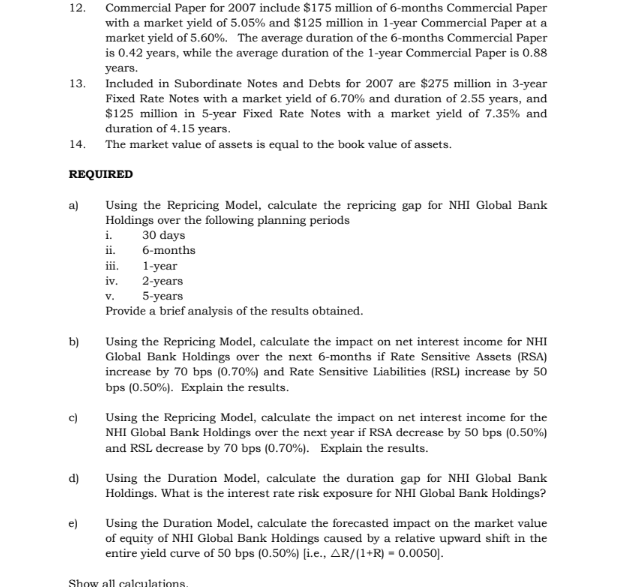

The extract of the Statement of Financial Position for NHI Global Bank Holdings at December 31 is shown below Assets Liabilities and Equity Liabilities Cash Federal Funds Treasury Bills Treasury Notes and Bonds Consumer Loans Commercial and Industrial Loans Mortgages Other Assets 1. Equity 2. Demand Deposits Savings Account Money Market Deposit Accounts Certificate of Deposits Commercial Paper Subordinate Notes and Debts Additional information: Total Assets Total Liabilities Total Liabilities and Equity 2007 ($million) 20 150 175 350 1,200 550 1,850 25 4,320 450 125 325 2,280 300 400 3,880 440 4,320 2006 23 160 180 330 1,125 495 1,775 24 4,112 435 135 330 2,137 275 375 3,687 425 4,112 The 2007 amount for Federal Funds is at a market yield of 5.00% with a duration of 0.02 years. The 2007 amounts for Treasury Bills include $125 million 3-months Treasury Bills at a market yield of 5.25% with a duration of 0.22 years, and $50 million 6- months Treasury Bills at a market yield of 5.40% with a duration of 0.48 years. 3. 4. 5. 6. 7. 8. 9. 10. Included in the 2007 amount of Treasury Notes and Bonds are $200 million 2- year Treasury Notes at a market yield of 5.95% and a duration of 1.80 years; $75 million 5-year Treasury Notes at a market yield of 6.50% and a duration of 4.50 years; $50 million 7-year Treasury Bonds at a market yield of 7.25% and duration of 6.30 years; and $25 million 8-year Treasury Bonds at a market yield of 7.50% and duration of 7.10 years. The 2007 amounts for Consumer Loans include $250 million of Consumer Loans maturing at 6-months at a market yield of 6.00% ; $350 million of Consumer Loans maturing at 1-year at a market yield of 6.25%; $200 million of Consumer Loans maturing in 2-years at a market yield of 6.50% and $400 million in Car Loans maturing in 5-years at a market yield of 7.25%. The average duration of the 6-months Consumer Loans is 0.30 years, the average duration of the 1-year Consumer Loans is 0.70 years, the average duration of the 2-year Consumer Loans is 1.35 years, while the average duration on the Car Loans is 3.80 years. Commercial and Industrial (C&I) Loans for 2007 include $250 million of C&I Loans maturing at 6-months at a market yield of 5.95% (duration 0.38 years), $130 million in 2-year Floating Rate C&I Loans at a market yield of 5.75% which are repriced every 6-months (duration 1.45 years) and $170 million in 5-year Floating Rate C&I Loans at a market yield of 6.10% which are repriced every 9- months (duration 3.75 years). Included in Mortgages for 2007 are $200 million 15-year Variable Rate Mortgages with a current market yield of 5.95% which are repriced on a quarterly basis (average duration 9.10 years), $250 million 15-year Variable Rate Mortgages with a current market yield of 6.15% which are repriced on an annual basis (average duration 9.75 years), $350 million 15-year Fixed Rate Mortgages with a current market yield of 8.00% (average duration 10.50 years), $225 million 30-year Variable Rate Mortgages with a current market yield of 8.25% which are repriced on a quarterly basis (average duration 18.25 years), $275 million 30-year Variable Rate Mortgages with a current market yield of 8.40% and which are repriced on an annual basis (average duration 18.50 years), and $550 million of 30-year Fixed Rate Mortgages with a current market yield of 8.25% (average duration 19.50 years). Other Assets include premises and equipment. No interest is payable on the Demand Deposits and these are callable on Demand. The 2007 amount for Savings Accounts are at a market yield of 1.50% and these Savings Accounts have an average duration of 1.25 years. The Money Market Deposit Accounts for 2007 are at a market yield of 4.50% and have an average duration of 0.50 years. 11. Included in Certificate of Deposits (CDs) for 2007 are $375 million in 3-months CDs at a market yield of 4.15% and average duration of 0.20 years; $260 million on 6-months CDs at a market yield of 4.25% and average duration of 0.46 years; $475 million of 1-year CDs at market yield of 4.40% and average duration of 0.95 years; $400 million of 2-year CDs at a market yield of 4.75% and average duration of 1.90 years; $250 million of 3-year CDs at a market yield of 5.10% and average duration of 2.85 years; $250 million of 4-year CDs at a market yield of 5.60% and average duration of 3.80 years; and $270 million of 5-year CDs at a market yield of 6.00% and average duration of 4.75 years. 12. 13. 14, a) REQUIRED b) c) d) Commercial Paper for 2007 include $175 million of 6-months Commercial Paper with a market yield of 5.05% and $125 million in 1-year Commercial Paper at a market yield of 5.60%. The average duration of the 6-months Commercial Paper is 0.42 years, while the average duration of the 1-year Commercial Paper is 0.88 years. e) Included in Subordinate Notes and Debts for 2007 are $275 million in 3-year Fixed Rate Notes with a market yield of 6.70% and duration of 2.55 years, and $125 million in 5-year Fixed Rate Notes with a market yield of 7.35% and duration of 4.15 years. The market value of assets is equal to the book value of assets. Using the Repricing Model, calculate the repricing gap for NHI Global Bank Holdings over the following planning periods 30 days 6-months i. ii. iii. iv. V. 1-year 2-years 5-years Provide a brief analysis of the results obtained. Using the Repricing Model, calculate the impact on net interest income for NHI Global Bank Holdings over the next 6-months if Rate Sensitive Assets (RSA) increase by 70 bps (0.70%) and Rate Sensitive Liabilities (RSL) increase by 50 bps (0.50%). Explain the results. Using the Repricing Model, calculate the impact on net interest income for the NHI Global Bank Holdings over the next year if RSA decrease by 50 bps (0.50%) and RSL decrease by 70 bps (0.70%). Explain the results. Using the Duration Model, calculate the duration gap for NHI Global Bank Holdings. What is the interest rate risk exposure for NHI Global Bank Holdings? Using the Duration Model, calculate the forecasted impact on the market value of equity of NHI Global Bank Holdings caused by a relative upward shift in the entire yield curve of 50 bps (0.50% ) [i.e., AR/ (1+R) - 0.0050]. Show all calculations. The extract of the Statement of Financial Position for NHI Global Bank Holdings at December 31 is shown below Assets Liabilities and Equity Liabilities Cash Federal Funds Treasury Bills Treasury Notes and Bonds Consumer Loans Commercial and Industrial Loans Mortgages Other Assets 1. Equity 2. Demand Deposits Savings Account Money Market Deposit Accounts Certificate of Deposits Commercial Paper Subordinate Notes and Debts Additional information: Total Assets Total Liabilities Total Liabilities and Equity 2007 ($million) 20 150 175 350 1,200 550 1,850 25 4,320 450 125 325 2,280 300 400 3,880 440 4,320 2006 23 160 180 330 1,125 495 1,775 24 4,112 435 135 330 2,137 275 375 3,687 425 4,112 The 2007 amount for Federal Funds is at a market yield of 5.00% with a duration of 0.02 years. The 2007 amounts for Treasury Bills include $125 million 3-months Treasury Bills at a market yield of 5.25% with a duration of 0.22 years, and $50 million 6- months Treasury Bills at a market yield of 5.40% with a duration of 0.48 years. 3. 4. 5. 6. 7. 8. 9. 10. Included in the 2007 amount of Treasury Notes and Bonds are $200 million 2- year Treasury Notes at a market yield of 5.95% and a duration of 1.80 years; $75 million 5-year Treasury Notes at a market yield of 6.50% and a duration of 4.50 years; $50 million 7-year Treasury Bonds at a market yield of 7.25% and duration of 6.30 years; and $25 million 8-year Treasury Bonds at a market yield of 7.50% and duration of 7.10 years. The 2007 amounts for Consumer Loans include $250 million of Consumer Loans maturing at 6-months at a market yield of 6.00% ; $350 million of Consumer Loans maturing at 1-year at a market yield of 6.25%; $200 million of Consumer Loans maturing in 2-years at a market yield of 6.50% and $400 million in Car Loans maturing in 5-years at a market yield of 7.25%. The average duration of the 6-months Consumer Loans is 0.30 years, the average duration of the 1-year Consumer Loans is 0.70 years, the average duration of the 2-year Consumer Loans is 1.35 years, while the average duration on the Car Loans is 3.80 years. Commercial and Industrial (C&I) Loans for 2007 include $250 million of C&I Loans maturing at 6-months at a market yield of 5.95% (duration 0.38 years), $130 million in 2-year Floating Rate C&I Loans at a market yield of 5.75% which are repriced every 6-months (duration 1.45 years) and $170 million in 5-year Floating Rate C&I Loans at a market yield of 6.10% which are repriced every 9- months (duration 3.75 years). Included in Mortgages for 2007 are $200 million 15-year Variable Rate Mortgages with a current market yield of 5.95% which are repriced on a quarterly basis (average duration 9.10 years), $250 million 15-year Variable Rate Mortgages with a current market yield of 6.15% which are repriced on an annual basis (average duration 9.75 years), $350 million 15-year Fixed Rate Mortgages with a current market yield of 8.00% (average duration 10.50 years), $225 million 30-year Variable Rate Mortgages with a current market yield of 8.25% which are repriced on a quarterly basis (average duration 18.25 years), $275 million 30-year Variable Rate Mortgages with a current market yield of 8.40% and which are repriced on an annual basis (average duration 18.50 years), and $550 million of 30-year Fixed Rate Mortgages with a current market yield of 8.25% (average duration 19.50 years). Other Assets include premises and equipment. No interest is payable on the Demand Deposits and these are callable on Demand. The 2007 amount for Savings Accounts are at a market yield of 1.50% and these Savings Accounts have an average duration of 1.25 years. The Money Market Deposit Accounts for 2007 are at a market yield of 4.50% and have an average duration of 0.50 years. 11. Included in Certificate of Deposits (CDs) for 2007 are $375 million in 3-months CDs at a market yield of 4.15% and average duration of 0.20 years; $260 million on 6-months CDs at a market yield of 4.25% and average duration of 0.46 years; $475 million of 1-year CDs at market yield of 4.40% and average duration of 0.95 years; $400 million of 2-year CDs at a market yield of 4.75% and average duration of 1.90 years; $250 million of 3-year CDs at a market yield of 5.10% and average duration of 2.85 years; $250 million of 4-year CDs at a market yield of 5.60% and average duration of 3.80 years; and $270 million of 5-year CDs at a market yield of 6.00% and average duration of 4.75 years. 12. 13. 14, a) REQUIRED b) c) d) Commercial Paper for 2007 include $175 million of 6-months Commercial Paper with a market yield of 5.05% and $125 million in 1-year Commercial Paper at a market yield of 5.60%. The average duration of the 6-months Commercial Paper is 0.42 years, while the average duration of the 1-year Commercial Paper is 0.88 years. e) Included in Subordinate Notes and Debts for 2007 are $275 million in 3-year Fixed Rate Notes with a market yield of 6.70% and duration of 2.55 years, and $125 million in 5-year Fixed Rate Notes with a market yield of 7.35% and duration of 4.15 years. The market value of assets is equal to the book value of assets. Using the Repricing Model, calculate the repricing gap for NHI Global Bank Holdings over the following planning periods 30 days 6-months i. ii. iii. iv. V. 1-year 2-years 5-years Provide a brief analysis of the results obtained. Using the Repricing Model, calculate the impact on net interest income for NHI Global Bank Holdings over the next 6-months if Rate Sensitive Assets (RSA) increase by 70 bps (0.70%) and Rate Sensitive Liabilities (RSL) increase by 50 bps (0.50%). Explain the results. Using the Repricing Model, calculate the impact on net interest income for the NHI Global Bank Holdings over the next year if RSA decrease by 50 bps (0.50%) and RSL decrease by 70 bps (0.70%). Explain the results. Using the Duration Model, calculate the duration gap for NHI Global Bank Holdings. What is the interest rate risk exposure for NHI Global Bank Holdings? Using the Duration Model, calculate the forecasted impact on the market value of equity of NHI Global Bank Holdings caused by a relative upward shift in the entire yield curve of 50 bps (0.50% ) [i.e., AR/ (1+R) - 0.0050]. Show all calculations. The extract of the Statement of Financial Position for NHI Global Bank Holdings at December 31 is shown below Assets Liabilities and Equity Liabilities Cash Federal Funds Treasury Bills Treasury Notes and Bonds Consumer Loans Commercial and Industrial Loans Mortgages Other Assets 1. Equity 2. Demand Deposits Savings Account Money Market Deposit Accounts Certificate of Deposits Commercial Paper Subordinate Notes and Debts Additional information: Total Assets Total Liabilities Total Liabilities and Equity 2007 ($million) 20 150 175 350 1,200 550 1,850 25 4,320 450 125 325 2,280 300 400 3,880 440 4,320 2006 23 160 180 330 1,125 495 1,775 24 4,112 435 135 330 2,137 275 375 3,687 425 4,112 The 2007 amount for Federal Funds is at a market yield of 5.00% with a duration of 0.02 years. The 2007 amounts for Treasury Bills include $125 million 3-months Treasury Bills at a market yield of 5.25% with a duration of 0.22 years, and $50 million 6- months Treasury Bills at a market yield of 5.40% with a duration of 0.48 years. 3. 4. 5. 6. 7. 8. 9. 10. Included in the 2007 amount of Treasury Notes and Bonds are $200 million 2- year Treasury Notes at a market yield of 5.95% and a duration of 1.80 years; $75 million 5-year Treasury Notes at a market yield of 6.50% and a duration of 4.50 years; $50 million 7-year Treasury Bonds at a market yield of 7.25% and duration of 6.30 years; and $25 million 8-year Treasury Bonds at a market yield of 7.50% and duration of 7.10 years. The 2007 amounts for Consumer Loans include $250 million of Consumer Loans maturing at 6-months at a market yield of 6.00% ; $350 million of Consumer Loans maturing at 1-year at a market yield of 6.25%; $200 million of Consumer Loans maturing in 2-years at a market yield of 6.50% and $400 million in Car Loans maturing in 5-years at a market yield of 7.25%. The average duration of the 6-months Consumer Loans is 0.30 years, the average duration of the 1-year Consumer Loans is 0.70 years, the average duration of the 2-year Consumer Loans is 1.35 years, while the average duration on the Car Loans is 3.80 years. Commercial and Industrial (C&I) Loans for 2007 include $250 million of C&I Loans maturing at 6-months at a market yield of 5.95% (duration 0.38 years), $130 million in 2-year Floating Rate C&I Loans at a market yield of 5.75% which are repriced every 6-months (duration 1.45 years) and $170 million in 5-year Floating Rate C&I Loans at a market yield of 6.10% which are repriced every 9- months (duration 3.75 years). Included in Mortgages for 2007 are $200 million 15-year Variable Rate Mortgages with a current market yield of 5.95% which are repriced on a quarterly basis (average duration 9.10 years), $250 million 15-year Variable Rate Mortgages with a current market yield of 6.15% which are repriced on an annual basis (average duration 9.75 years), $350 million 15-year Fixed Rate Mortgages with a current market yield of 8.00% (average duration 10.50 years), $225 million 30-year Variable Rate Mortgages with a current market yield of 8.25% which are repriced on a quarterly basis (average duration 18.25 years), $275 million 30-year Variable Rate Mortgages with a current market yield of 8.40% and which are repriced on an annual basis (average duration 18.50 years), and $550 million of 30-year Fixed Rate Mortgages with a current market yield of 8.25% (average duration 19.50 years). Other Assets include premises and equipment. No interest is payable on the Demand Deposits and these are callable on Demand. The 2007 amount for Savings Accounts are at a market yield of 1.50% and these Savings Accounts have an average duration of 1.25 years. The Money Market Deposit Accounts for 2007 are at a market yield of 4.50% and have an average duration of 0.50 years. 11. Included in Certificate of Deposits (CDs) for 2007 are $375 million in 3-months CDs at a market yield of 4.15% and average duration of 0.20 years; $260 million on 6-months CDs at a market yield of 4.25% and average duration of 0.46 years; $475 million of 1-year CDs at market yield of 4.40% and average duration of 0.95 years; $400 million of 2-year CDs at a market yield of 4.75% and average duration of 1.90 years; $250 million of 3-year CDs at a market yield of 5.10% and average duration of 2.85 years; $250 million of 4-year CDs at a market yield of 5.60% and average duration of 3.80 years; and $270 million of 5-year CDs at a market yield of 6.00% and average duration of 4.75 years. 12. 13. 14, a) REQUIRED b) c) d) Commercial Paper for 2007 include $175 million of 6-months Commercial Paper with a market yield of 5.05% and $125 million in 1-year Commercial Paper at a market yield of 5.60%. The average duration of the 6-months Commercial Paper is 0.42 years, while the average duration of the 1-year Commercial Paper is 0.88 years. e) Included in Subordinate Notes and Debts for 2007 are $275 million in 3-year Fixed Rate Notes with a market yield of 6.70% and duration of 2.55 years, and $125 million in 5-year Fixed Rate Notes with a market yield of 7.35% and duration of 4.15 years. The market value of assets is equal to the book value of assets. Using the Repricing Model, calculate the repricing gap for NHI Global Bank Holdings over the following planning periods 30 days 6-months i. ii. iii. iv. V. 1-year 2-years 5-years Provide a brief analysis of the results obtained. Using the Repricing Model, calculate the impact on net interest income for NHI Global Bank Holdings over the next 6-months if Rate Sensitive Assets (RSA) increase by 70 bps (0.70%) and Rate Sensitive Liabilities (RSL) increase by 50 bps (0.50%). Explain the results. Using the Repricing Model, calculate the impact on net interest income for the NHI Global Bank Holdings over the next year if RSA decrease by 50 bps (0.50%) and RSL decrease by 70 bps (0.70%). Explain the results. Using the Duration Model, calculate the duration gap for NHI Global Bank Holdings. What is the interest rate risk exposure for NHI Global Bank Holdings? Using the Duration Model, calculate the forecasted impact on the market value of equity of NHI Global Bank Holdings caused by a relative upward shift in the entire yield curve of 50 bps (0.50% ) [i.e., AR/ (1+R) - 0.0050]. Show all calculations. The extract of the Statement of Financial Position for NHI Global Bank Holdings at December 31 is shown below Assets Liabilities and Equity Liabilities Cash Federal Funds Treasury Bills Treasury Notes and Bonds Consumer Loans Commercial and Industrial Loans Mortgages Other Assets 1. Equity 2. Demand Deposits Savings Account Money Market Deposit Accounts Certificate of Deposits Commercial Paper Subordinate Notes and Debts Additional information: Total Assets Total Liabilities Total Liabilities and Equity 2007 ($million) 20 150 175 350 1,200 550 1,850 25 4,320 450 125 325 2,280 300 400 3,880 440 4,320 2006 23 160 180 330 1,125 495 1,775 24 4,112 435 135 330 2,137 275 375 3,687 425 4,112 The 2007 amount for Federal Funds is at a market yield of 5.00% with a duration of 0.02 years. The 2007 amounts for Treasury Bills include $125 million 3-months Treasury Bills at a market yield of 5.25% with a duration of 0.22 years, and $50 million 6- months Treasury Bills at a market yield of 5.40% with a duration of 0.48 years. 3. 4. 5. 6. 7. 8. 9. 10. Included in the 2007 amount of Treasury Notes and Bonds are $200 million 2- year Treasury Notes at a market yield of 5.95% and a duration of 1.80 years; $75 million 5-year Treasury Notes at a market yield of 6.50% and a duration of 4.50 years; $50 million 7-year Treasury Bonds at a market yield of 7.25% and duration of 6.30 years; and $25 million 8-year Treasury Bonds at a market yield of 7.50% and duration of 7.10 years. The 2007 amounts for Consumer Loans include $250 million of Consumer Loans maturing at 6-months at a market yield of 6.00% ; $350 million of Consumer Loans maturing at 1-year at a market yield of 6.25%; $200 million of Consumer Loans maturing in 2-years at a market yield of 6.50% and $400 million in Car Loans maturing in 5-years at a market yield of 7.25%. The average duration of the 6-months Consumer Loans is 0.30 years, the average duration of the 1-year Consumer Loans is 0.70 years, the average duration of the 2-year Consumer Loans is 1.35 years, while the average duration on the Car Loans is 3.80 years. Commercial and Industrial (C&I) Loans for 2007 include $250 million of C&I Loans maturing at 6-months at a market yield of 5.95% (duration 0.38 years), $130 million in 2-year Floating Rate C&I Loans at a market yield of 5.75% which are repriced every 6-months (duration 1.45 years) and $170 million in 5-year Floating Rate C&I Loans at a market yield of 6.10% which are repriced every 9- months (duration 3.75 years). Included in Mortgages for 2007 are $200 million 15-year Variable Rate Mortgages with a current market yield of 5.95% which are repriced on a quarterly basis (average duration 9.10 years), $250 million 15-year Variable Rate Mortgages with a current market yield of 6.15% which are repriced on an annual basis (average duration 9.75 years), $350 million 15-year Fixed Rate Mortgages with a current market yield of 8.00% (average duration 10.50 years), $225 million 30-year Variable Rate Mortgages with a current market yield of 8.25% which are repriced on a quarterly basis (average duration 18.25 years), $275 million 30-year Variable Rate Mortgages with a current market yield of 8.40% and which are repriced on an annual basis (average duration 18.50 years), and $550 million of 30-year Fixed Rate Mortgages with a current market yield of 8.25% (average duration 19.50 years). Other Assets include premises and equipment. No interest is payable on the Demand Deposits and these are callable on Demand. The 2007 amount for Savings Accounts are at a market yield of 1.50% and these Savings Accounts have an average duration of 1.25 years. The Money Market Deposit Accounts for 2007 are at a market yield of 4.50% and have an average duration of 0.50 years. 11. Included in Certificate of Deposits (CDs) for 2007 are $375 million in 3-months CDs at a market yield of 4.15% and average duration of 0.20 years; $260 million on 6-months CDs at a market yield of 4.25% and average duration of 0.46 years; $475 million of 1-year CDs at market yield of 4.40% and average duration of 0.95 years; $400 million of 2-year CDs at a market yield of 4.75% and average duration of 1.90 years; $250 million of 3-year CDs at a market yield of 5.10% and average duration of 2.85 years; $250 million of 4-year CDs at a market yield of 5.60% and average duration of 3.80 years; and $270 million of 5-year CDs at a market yield of 6.00% and average duration of 4.75 years. 12. 13. 14, a) REQUIRED b) c) d) Commercial Paper for 2007 include $175 million of 6-months Commercial Paper with a market yield of 5.05% and $125 million in 1-year Commercial Paper at a market yield of 5.60%. The average duration of the 6-months Commercial Paper is 0.42 years, while the average duration of the 1-year Commercial Paper is 0.88 years. e) Included in Subordinate Notes and Debts for 2007 are $275 million in 3-year Fixed Rate Notes with a market yield of 6.70% and duration of 2.55 years, and $125 million in 5-year Fixed Rate Notes with a market yield of 7.35% and duration of 4.15 years. The market value of assets is equal to the book value of assets. Using the Repricing Model, calculate the repricing gap for NHI Global Bank Holdings over the following planning periods 30 days 6-months i. ii. iii. iv. V. 1-year 2-years 5-years Provide a brief analysis of the results obtained. Using the Repricing Model, calculate the impact on net interest income for NHI Global Bank Holdings over the next 6-months if Rate Sensitive Assets (RSA) increase by 70 bps (0.70%) and Rate Sensitive Liabilities (RSL) increase by 50 bps (0.50%). Explain the results. Using the Repricing Model, calculate the impact on net interest income for the NHI Global Bank Holdings over the next year if RSA decrease by 50 bps (0.50%) and RSL decrease by 70 bps (0.70%). Explain the results. Using the Duration Model, calculate the duration gap for NHI Global Bank Holdings. What is the interest rate risk exposure for NHI Global Bank Holdings? Using the Duration Model, calculate the forecasted impact on the market value of equity of NHI Global Bank Holdings caused by a relative upward shift in the entire yield curve of 50 bps (0.50% ) [i.e., AR/ (1+R) - 0.0050]. Show all calculations.

Expert Answer:

Answer rating: 100% (QA)

The repricing gap for NHI Global Bank Holdings over the following planning periods would be 30 days 002 million 6 months 009 million 1 year 021 millio... View the full answer

Related Book For

Posted Date:

Students also viewed these accounting questions

-

The equity section of Ahab SA at December 31 is as follows. AHAB SA Statement of Financial Position (partial) Equity Share capital-preference, cumulative, 10,000 shares authorized, 5,000 shares...

-

The December 31, 2015, statement of financial position for the Blood Donors of America Foundation is presented below. Statement of Financial Position December 31, 2015 Assets Cash...

-

The comparative statement of financial position for Baird Corporation shows the following noncash current asset and liability accounts at March 31: _____________________________________ 2015...

-

You are considering an investment that will be valued at $1,000 one year from now. Your next best alternative investment opportunity would yield an annual rate of return of 8%, In other words, if you...

-

The Swift Company is planning to finance an expansion. The principal executives of the company agree that an industrial company such as theirs should finance growth by issuing common stock rather...

-

A home in a remote location without access to municipal power is expensive to heat during the winter using a gas generator. The home owner is considering whether to set the thermostat to 66 deg F...

-

a. Describe the circumstances where discovery sampling may be useful in auditing. b. What factors are necessary to determine sample size in discovery sampling?

-

At the end of the year, Bertha Enterprises estimates the uncollectible accounts expense to be 0.7 percent of net sales of $15,150,000. The current credit balance of Allowance for Uncollectible...

-

Identify the best definition for network event log analysis The process of properly gathering, safeguarding, and synthesizing network event logs to identify root cause of a system problem The process...

-

What is the relationship between the variable LastByteRcvd in Section 3.5.5 and the variable y in Section 3.5.4?

-

How much would you be prepared to pay for a $ 1 , 0 0 0 face value bond with a 1 0 % coupon, annual payments, and 5 years to maturity if the market interest rate is 1 2 % ? Show in Excel how the...

-

Identify the categories of individuals who can adopt children.

-

Identify the nature and purpose of permanency planning.

-

Describe the nature and purpose of putative father registries.

-

Describe the nature and purpose of a home study.

-

Describe the tort of interference with parental relationships.

-

Draw the products of the reaction of the substituted cyclopntene SHOWI below with HBr under kinetic (cold temperatures) and thermodynamic (warm temperatures). + HBr kinetic conditions thermodynamic...

-

For each equation, (a) Write it in slope-intercept form (b) Give the slope of the line (c) Give the y-intercept (d) Graph the line. 7x - 3y = 3

-

On January 1, 2017, Plutonium Corporation acquired 80% of the outstanding stock of Sulfurst Inc. for $268,000 cash. The following balance sheet shows Sulfurst Inc.'s book values immediately prior to...

-

Day and Night formed an accounting partnership in 2014. Capital transactions for Day and Night during 2014 are as follows: Partnership net income for the year ended December 31, 2014; is $68,400...

-

On January 2, 2014, Press Company purchased on the open market 90% of the outstanding common stock of Sensor Company for $800,000 cash. Balance sheets for Press Company and Sensor Company on January...

-

Find the number of recycle loops, the optimal number of tear streams, and the corresponding calculation sequence for the process flowsheet in Figure 7.38. Figure 7.38:- Figure 7.38 Process flowsheet....

-

Convert the process flowsheet in Figure 7.22 into a flowsheet for mass-balance simulation Task-1. List the model equations, the variables to be specified, and the variables to be calculated. Figure...

-

Given the feed streams and the parameters of the process units as shown in Figure 7.39, complete the simulation flowsheet for ASPEN PLUS and show the calculation sequence (i.e., complete the...

Study smarter with the SolutionInn App