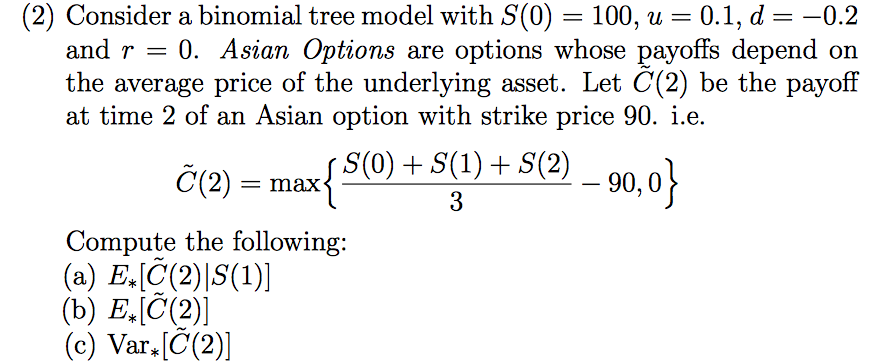

Question: Consider a binomial tree model with S(0) = 100, u = 0.1, d = -0.2 and r = 0. Asian Options are options whose payoffs

Consider a binomial tree model with S(0) = 100, u = 0.1, d = -0.2 and r = 0. Asian Options are options whose payoffs depend on the average price of the underlying asset. Let C(2) be the payoff at time 2 of an Asian option with strike price 90. i.e.^~C(2) = max{S(0) + S(1) + S(2)/3 - 90, 0} Compute the following: E_*[^~C(2)|S(1)] E_*[^~C(2)] Var_*[^~C(2)] Consider a binomial tree model with S(0) = 100, u = 0.1, d = -0.2 and r = 0. Asian Options are options whose payoffs depend on the average price of the underlying asset. Let C(2) be the payoff at time 2 of an Asian option with strike price 90. i.e.^~C(2) = max{S(0) + S(1) + S(2)/3 - 90, 0} Compute the following: E_*[^~C(2)|S(1)] E_*[^~C(2)] Var_*[^~C(2)]

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts