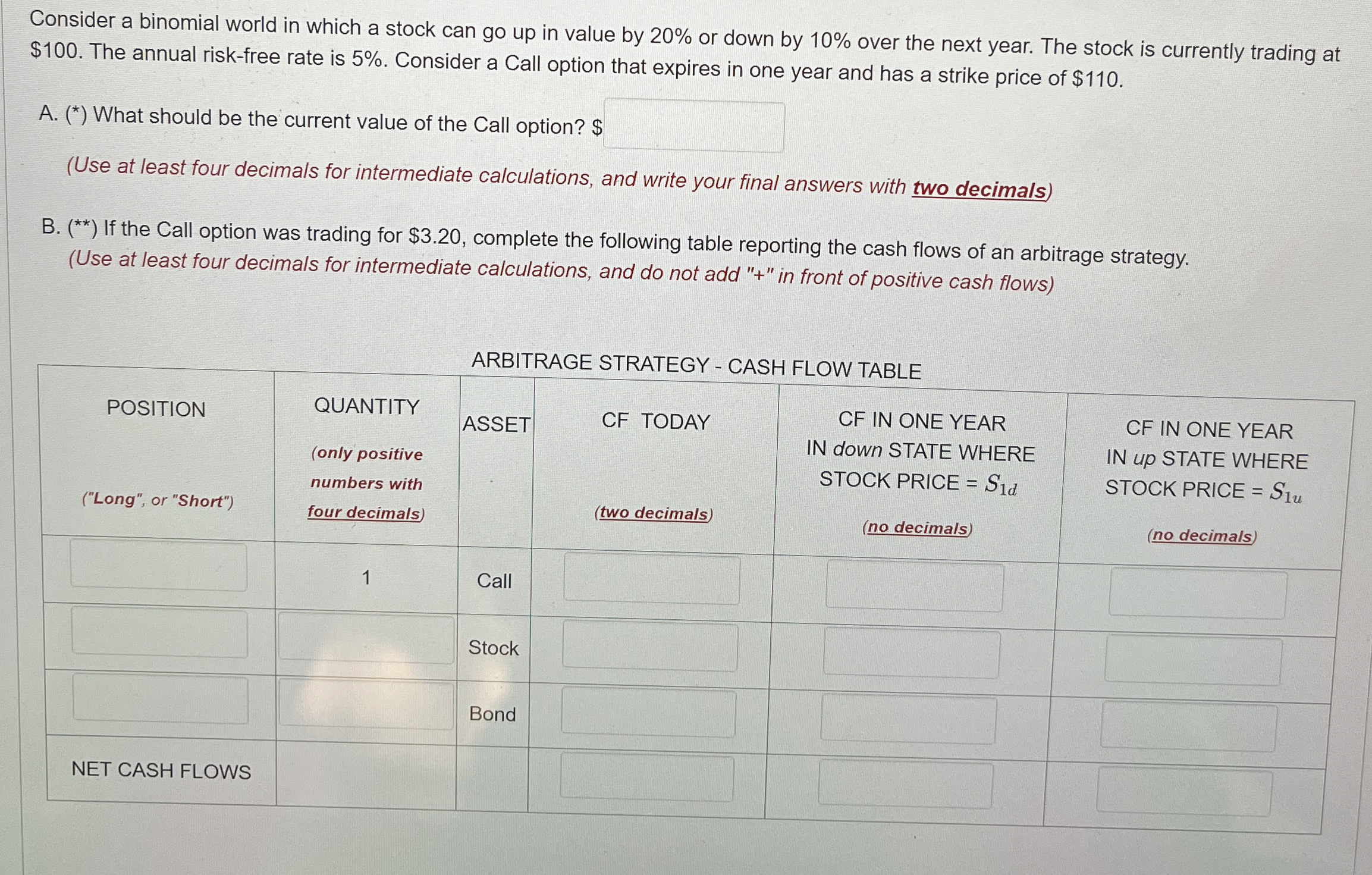

Question: Consider a binomial world in which a stock can go up in value by 2 0 % or down by 1 0 % over the

Consider a binomial world in which a stock can go up in value by or down by over the next year. The stock is currently trading at

$ The annual riskfree rate is Consider a Call option that expires in one year and has a strike price of $

A What should be the current value of the Call option? $

Use at least four decimals for intermediate calculations, and write your final answers with two decimals

B If the Call option was trading for $ complete the following table reporting the cash flows of an arbitrage strategy.

Use at least four decimals for intermediate calculations, and do not add in front of positive cash flows

ARBITRAGE STRATEGY CASH FLOW TABLE

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock