Question: Consider a four-year zero-coupon bond. Use a binomial tree for this calculation. The probability that the rate moves higher is 70%; it moves lower is

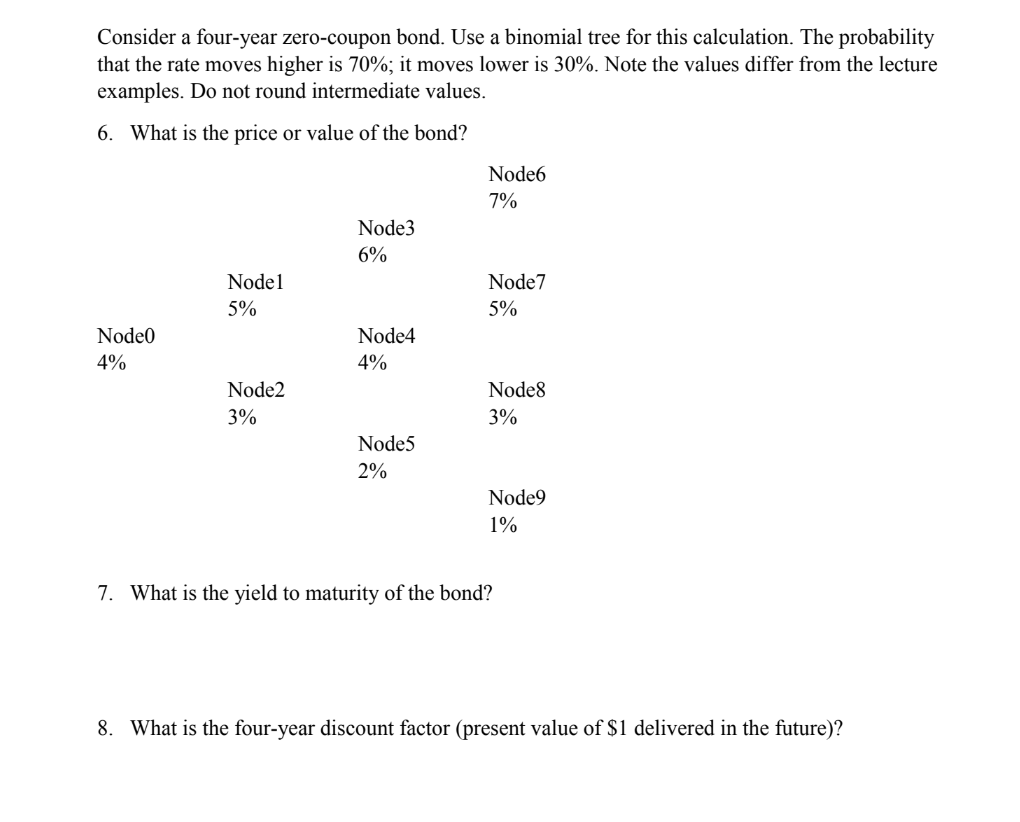

Consider a four-year zero-coupon bond. Use a binomial tree for this calculation. The probability that the rate moves higher is 70%; it moves lower is 30%. Note the values differ from the lecture examples. Do not round intermediate values. 6. What is the price or value of the bond? Node6 7% Node3 6% Node 7 Nodel 5% 5% Nodeo 4% Node4 4% Node 8 Node2 3% 3% Node5 2% Node 9 1% 7. What is the yield to maturity of the bond? 8. What is the four-year discount factor (present value of $1 delivered in the future)? Consider a four-year zero-coupon bond. Use a binomial tree for this calculation. The probability that the rate moves higher is 70%; it moves lower is 30%. Note the values differ from the lecture examples. Do not round intermediate values. 6. What is the price or value of the bond? Node6 7% Node3 6% Node 7 Nodel 5% 5% Nodeo 4% Node4 4% Node 8 Node2 3% 3% Node5 2% Node 9 1% 7. What is the yield to maturity of the bond? 8. What is the four-year discount factor (present value of $1 delivered in the future)

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts