Question: Consider a GARCH model with parameter estimates given by: Parameter Estimate 0.91 0.04 0.07 Is the estimated model stationary? What is the long-run variance

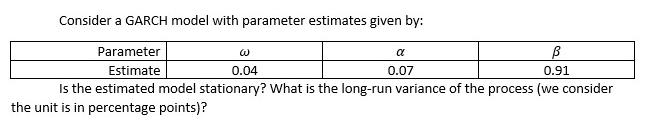

Consider a GARCH model with parameter estimates given by: Parameter Estimate 0.91 0.04 0.07 Is the estimated model stationary? What is the long-run variance of the process (we consider the unit is in percentage points)?

Step by Step Solution

★★★★★

3.39 Rating (149 Votes )

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

To determine if the estimated GARCH model is stationary and find the longrun var... View full answer

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock