Question: Consider a market model with two securities S1 and S2 and three scenarios, 61, 62 and 63 such that P(01) = P(@3) = P(@2)/2 =

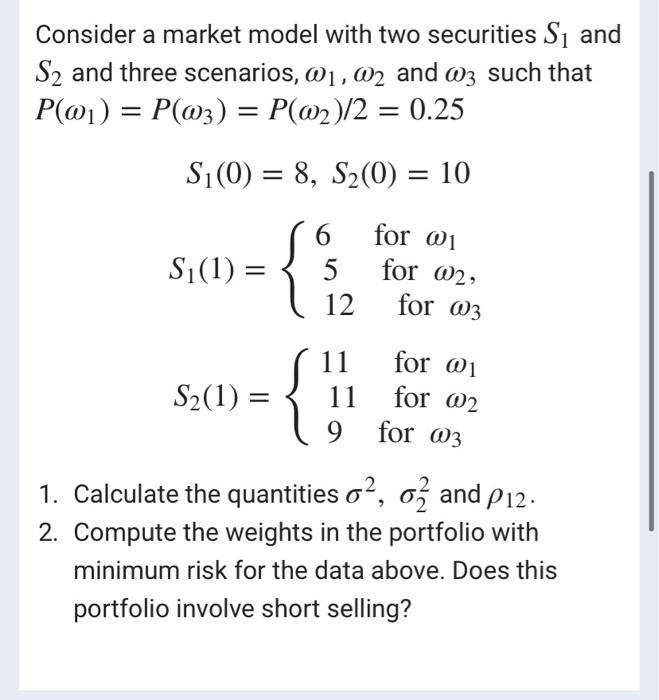

Consider a market model with two securities S1 and S2 and three scenarios, 61, 62 and 63 such that P(01) = P(@3) = P(@2)/2 = 0.25 Si(0) = 8, S2(0) = 10 Si(1) = 6 5 12 for 01 for 02, for 03 S2(1) = { 11 11 9 for 01 for 02 for 03 1. Calculate the quantities o?, oz and P12. 2. Compute the weights in the portfolio with minimum risk for the data above. Does this portfolio involve short selling? Consider a market model with two securities S1 and S2 and three scenarios, 61, 62 and 63 such that P(01) = P(@3) = P(@2)/2 = 0.25 Si(0) = 8, S2(0) = 10 Si(1) = 6 5 12 for 01 for 02, for 03 S2(1) = { 11 11 9 for 01 for 02 for 03 1. Calculate the quantities o?, oz and P12. 2. Compute the weights in the portfolio with minimum risk for the data above. Does this portfolio involve short selling

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts