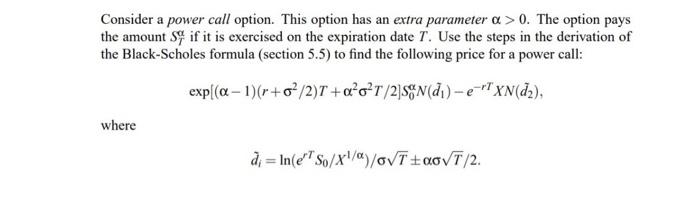

Question: Consider a power call option. This option has an extra parameter a > 0. The option pays the amount Sif it is exercised on the

Consider a power call option. This option has an extra parameter a > 0. The option pays the amount Sif it is exercised on the expiration date T. Use the steps in the derivation of the Black-Scholes formula (section 5.5) to find the following price for a power call: expl(a-1)(r+o/2)T + ooT/2] (d)-e-TXN(2), where d = Inte" $/X1/)/V TEOOT/2

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock