Question: Consider a simple econometric model (mean or intercept model) for one variable as yi ui , where E(yi), is an unknown parameter, yi is ith

Consider a simple econometric model (mean or intercept model) for one variable as yi ui , where E(yi), is an unknown parameter, yi is ith sample observation on an economic

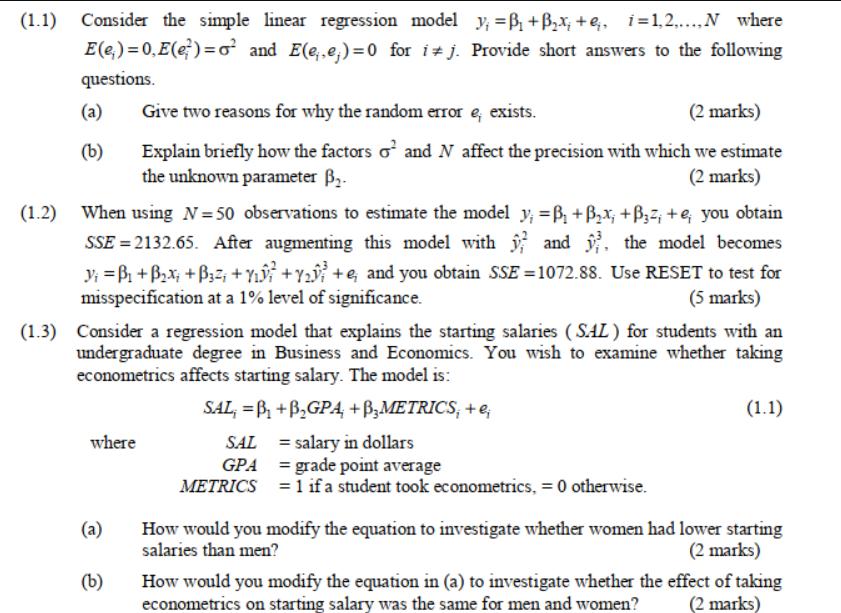

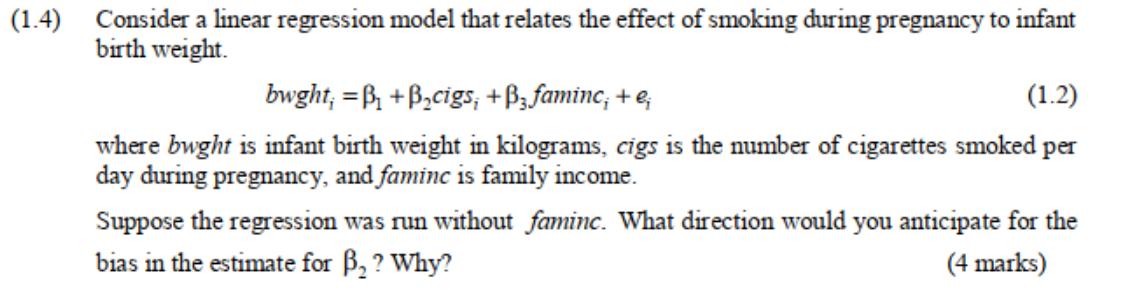

(1.1) Consider the simple linear regression model y, =B + Bx+, i=1,2,..., N where E(e) = 0, E(e)=o and E(e,e;)=0 for ij. Provide short answers to the following questions. (a) (b) (1.2) When using N=50 observations to estimate the model y =B + Bx; +B3z, +e; you obtain SSE=2132.65. After augmenting this model with the model becomes and V =B + Bx +B3 +Y++e, and you obtain SSE=1072.88. Use RESET to test for misspecification at a 1% level of significance. (5 marks) Give two reasons for why the random error e, exists. (2 marks) Explain briefly how the factors o' and N affect the precision with which we estimate the unknown parameter . (2 marks) (1.3) Consider a regression model that explains the starting salaries (SAL) for students with an undergraduate degree in Business and Economics. You wish to examine whether taking econometrics affects starting salary. The model is: SAL, =B + BGPA; +METRICS; +e; = salary in dollars = grade point average = 1 if a student took econometrics, = 0 otherwise. where (a) (b) SAL GPA METRICS (1.1) How would you modify the equation to investigate whether women had lower starting salaries than men? (2 marks) How would you modify the equation in (a) to investigate whether the effect of taking econometrics on starting salary was the same for men and women? (2 marks)

Step by Step Solution

3.45 Rating (152 Votes )

There are 3 Steps involved in it

a Two reasons for why the random error e exists in the simple linear regression model are 1 Inherent variability The relationship between the dependent variable y and the independent variable x is not ... View full answer

Get step-by-step solutions from verified subject matter experts