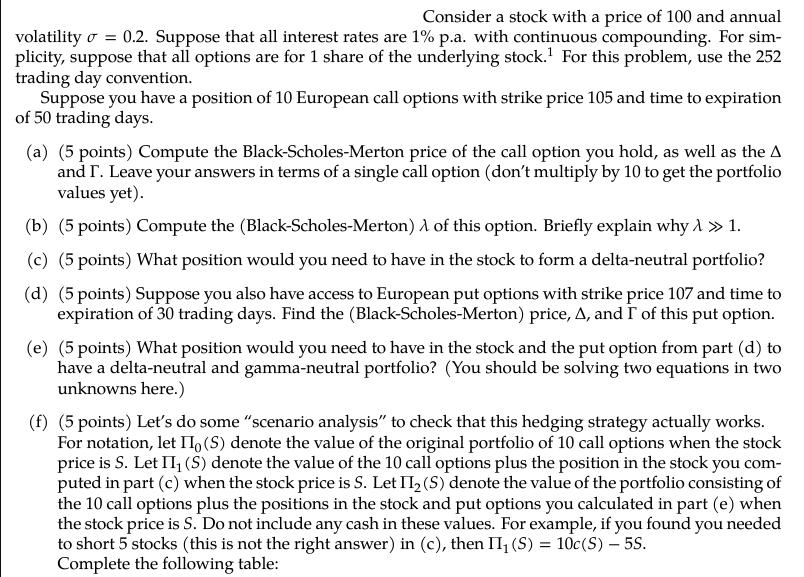

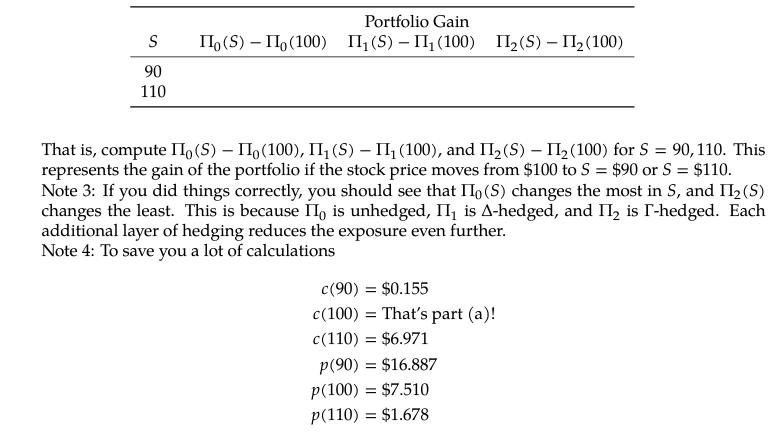

Consider a stock with a price of 100 and annual volatility = 0.2. Suppose that all...

Fantastic news! We've Found the answer you've been seeking!

Question:

Expert Answer:

Solution a The BlackScholesMerton price of the call option with strike price 105 and time to expiration of 50 trading days is C S Nd1 K erT Nd2 where S 100 K 105 r 001 T 50252 and Nd1 and Nd2 are the ... View the full answer

Related Book For

Financial Reporting and Analysis

ISBN: 978-1259722653

7th edition

Authors: Lawrence Revsine, Daniel Collins, Bruce Johnson, Fred Mittelstaedt, Leonard Soffer

Posted Date: