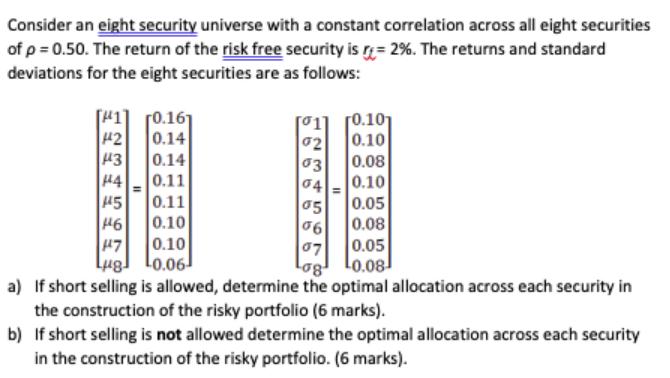

Question: Consider an eight security universe with a constant correlation across all eight securities of p = 0.50. The return of the risk free security

Consider an eight security universe with a constant correlation across all eight securities of p = 0.50. The return of the risk free security is r= 2%. The returns and standard deviations for the eight securities are as follows: [0.161 0.14 0.14 H4 0.11 445 H6 47 0.10 Lug. 0.06 442 443 = 0.11 0.10 02 03 0.08 04 0.10 [0.10 0.10 = 05 06 0.05 0.08 07 0.05 Log 0.08 a) If short selling is allowed, determine the optimal allocation across each security in the construction of the risky portfolio (6 marks). b) If short selling is not allowed determine the optimal allocation across each security in the construction of the risky portfolio. (6 marks).

Step by Step Solution

3.43 Rating (162 Votes )

There are 3 Steps involved in it

a If short selling is allowed the optimal allocation across each security in the construction of the ... View full answer

Get step-by-step solutions from verified subject matter experts