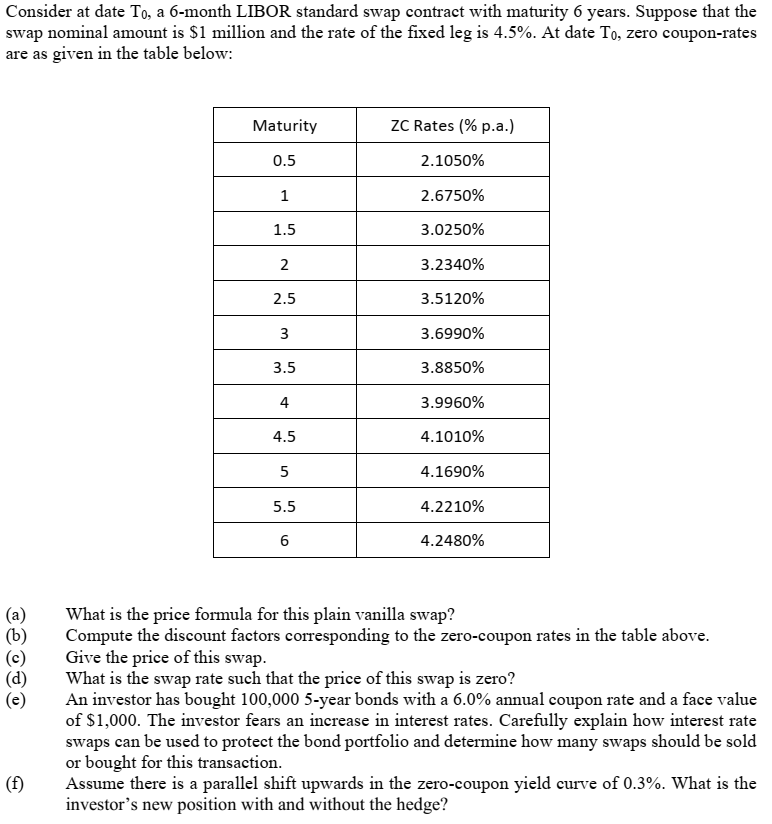

Question: Consider at date Tu, a 6-month LIBC'R. standard swap contract with maturity 6 years. Suppose that the swap nominal amount is $1 million and the

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts