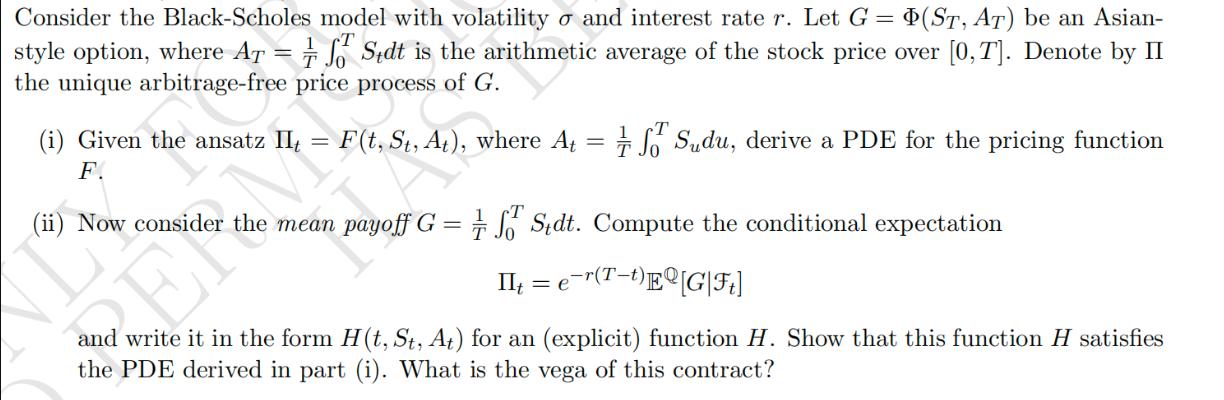

Consider the Black-Scholes model with volatility and interest rate r. Let G = (ST, AT) be...

Fantastic news! We've Found the answer you've been seeking!

Question:

Expert Answer:

Related Book For

Posted Date: