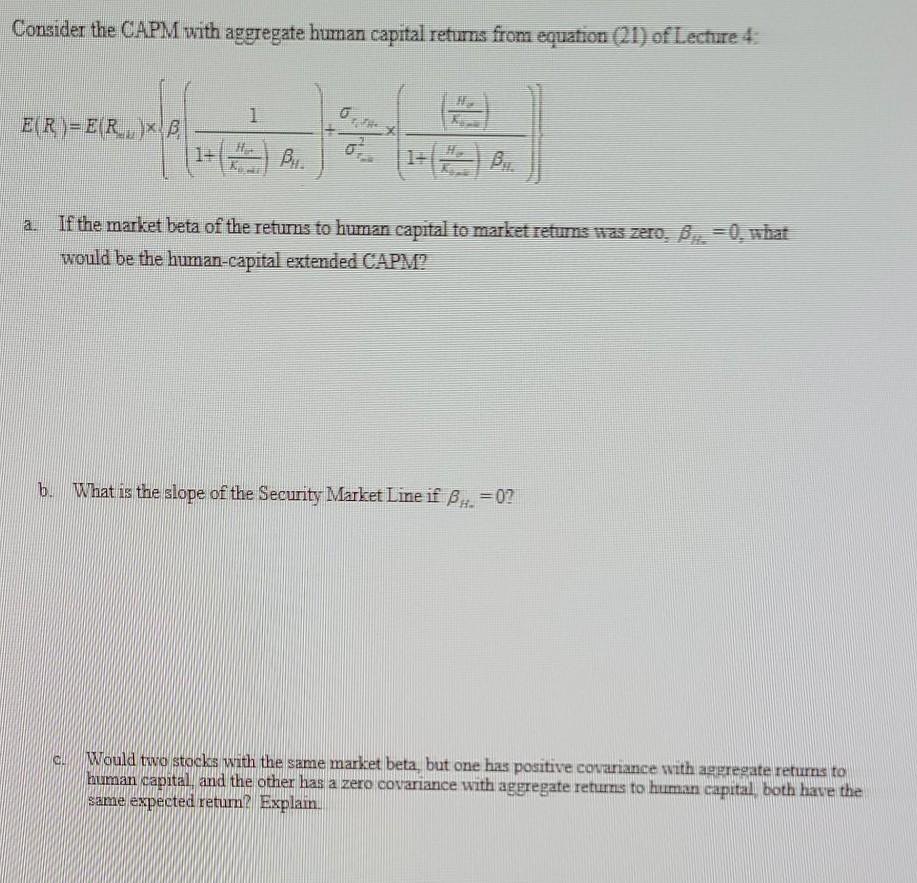

Question: Consider the CAPM with aggregate human capital returns from equation (21) of Lecture 4 1 E(R)=E(R.)x B + 1 a. If the market beta of

Consider the CAPM with aggregate human capital returns from equation (21) of Lecture 4 1 E(R)=E(R.)x B + 1 a. If the market beta of the returns to human capital to market returns was zero. By = 0what would be the human-capital extended CAPM? What is the slope of the Security Market Line if Bu=02 Would two stocks with the same market beta, but one has positive covariance with aggregate returns to human capital, and the other has a zero covariance with aggregate returns to human capital, both have the same expected retum? Explain. Consider the CAPM with aggregate human capital returns from equation (21) of Lecture 4 1 E(R)=E(R.)x B + 1 a. If the market beta of the returns to human capital to market returns was zero. By = 0what would be the human-capital extended CAPM? What is the slope of the Security Market Line if Bu=02 Would two stocks with the same market beta, but one has positive covariance with aggregate returns to human capital, and the other has a zero covariance with aggregate returns to human capital, both have the same expected retum? Explain

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts