Question: . Consider the data given below. The one-year rates can be viewed as spot interest rates, and the two-year rates are yields to maturity in

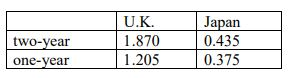

. Consider the data given below. The one-year rates can be viewed as spot interest rates, and the two-year rates are yields to maturity in annualized percent

.

The spot exchange rate is 130.15/.

What should be the two-year forward rate to prevent arbitrage?

two-year one-year U.K. 1.870 1.205 Japan 0.435 0.375

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock