Question: Consider the following European options with different strikes that expire in 6 month. Assume that the current stock price is 100 and zero interest rate.

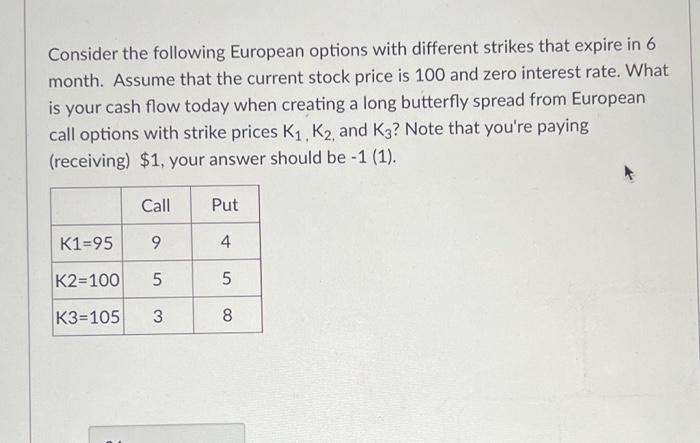

Consider the following European options with different strikes that expire in 6 month. Assume that the current stock price is 100 and zero interest rate. What is your cash flow today when creating a long butterfly spread from European call options with strike prices K1,K2, and K3 ? Note that you're paying (receiving) \$1, your answer should be -1 (1)

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock