Question: Consider the following information. For S = 100, X = 100, r = 5%, o = 30%, and T = 1 months: Call Option Put

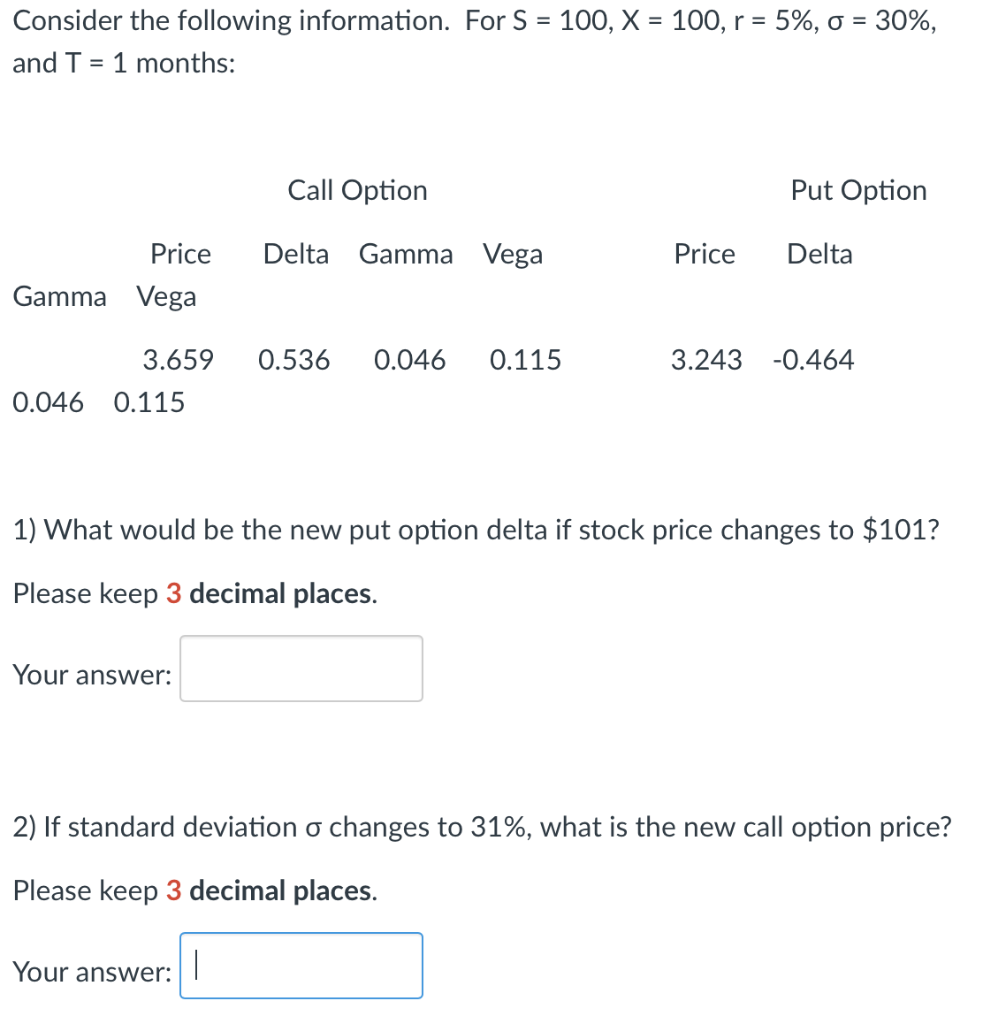

Consider the following information. For S = 100, X = 100, r = 5%, o = 30%, and T = 1 months: Call Option Put Option Delta Gamma Vega Price Delta Price Gamma Vega 0.536 0.046 0.115 3.243 -0.464 3.659 0.046 0.115 1) What would be the new put option delta if stock price changes to $101? Please keep 3 decimal places. Your answer: 2) If standard deviation o changes to 31%, what is the new call option price? Please keep 3 decimal places. Your answer: | Consider the following information. For S = 100, X = 100, r = 5%, o = 30%, and T = 1 months: Call Option Put Option Delta Gamma Vega Price Delta Price Gamma Vega 0.536 0.046 0.115 3.243 -0.464 3.659 0.046 0.115 1) What would be the new put option delta if stock price changes to $101? Please keep 3 decimal places. Your answer: 2) If standard deviation o changes to 31%, what is the new call option price? Please keep 3 decimal places. Your answer: |

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts